Buy Park Medi World Ltd for the Target Rs.350 by Choice Institutional Equities

NDR Takeaways: A Compounding Story

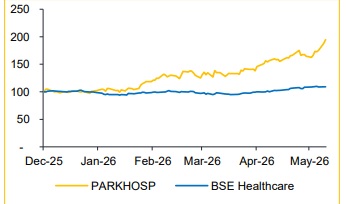

We hosted a Non-deal Roadshow with the Park Medi World Ltd. management in Mumbai on May 26, 2026, with Institutional Investors, where discussions primarily focussed on the recent acquisition of its Uttarakhand facility, its financial and operational performance and expansion plans. The management expects PARKHOSP’s growth to be driven by aggressive capacity expansion with efficient capital deployment, a richer case mix, optimised ALOS, improved payor mix and revised CGHS rate benefits

Valuation: We value the company at 18x EV/EBITDA on FY28E and hence maintain our ‘BUY’ rating with a revised target price of INR 350 (from INR 320).

1. What are the key details and strategic rationale behind the recent Uttarakhand acquisition? Answer: The acquisition of Medicity Hospital, Rudrapur, provides Park Medi World with a strategic entry into Uttarakhand through the largest NABHaccredited multi-super-specialty hospital in the area. It was an all-cash consideration of INR 1,770 Mn, funded through internal accruals. The acquisition increases the company’s network to 17 hospitals across six states and expands the total bed capacity to ~4,290. The deal aligns with the company’s strategy of expanding into high-potential but underserved markets through value-accretive inorganic growth.

2. What is the financial ramp-up trajectory for the acquired asset in Uttarakhand? Answer: Operations are expected to commence by the end of August 2026, with all of the 330 beds being made available from the outset. In Year 1, the company targets revenues of INR 1,000 Mn, EBITDA of INR 200 Mn (~20% margin) and PAT of INR 120 Mn (~12% margin), with occupancy maintained at 60–65%. By Year 2, revenues are expected to scale up to INR 1,400 Mn (40% YoY growth), with EBITDA improving to INR 35 Mn (~25% margin) and PAT of INR 21 Mn (~15% margin), supported by occupancy rising to 70–75%. Key operating levers include increasing ARPOB to INR 18,000–20,000, scaling up the super-specialty revenue mix, from the existing 60–65% to 70–75% and deploying top-end equipment to support higher-acuity procedures.

3. How does Park Medi World deliver high-quality care at affordable price points? Answer: We attribute our affordable healthcare model to a combination of operational efficiency, asset optimisation and scale benefits. The company owns 100% of its assets, ensuring 100% revenue accrual and no leakage. Unlike premium chains which allocate significant area to large suites, PARKHOSP's bed configuration — 40% general ward, 30% ICU/critical care, 20–22% twin-sharing and the remainder single sharing maximises revenue-generating beds. The company also benefits from economies of scale in procurement, consumables and equipment sourcing across its network. Combined with industry-low capex of ~INR 34 lakh per bed, this enables PARKHOSP to offer affordable tertiary and quaternary care while maintaining a healthy margin.

4. What are the key benefits of the cluster-based expansion model? Answer: The management believes the cluster-based approach is the key competitive advantage, as hospitals within close geographic proximity are able to share doctors, clinical expertise, equipment and operational resources efficiently. The strategy enhances utilisation levels, improves talent recruitment and retention, strengthens brand recall and drives synergies across the network.

5. What is the roadmap for ARPOB growth and what are the key upside levers? Answer: The management aspires to deliver nearly 10% ARPOB growth, driven by a combination of pricing inflation, increasing share of advanced and robotic procedures, improving specialty mix and higher occupancy. Upcoming expansion is also focussed on specialised care — for instance, Ambala is expected to add 200 beds focussed on oncology, while Mohali will see 150 beds dedicated to advanced super-specialty care.

6. What gives investors confidence in PARKHOSP's ability to sustain aggressive expansion with financial discipline? Answer: The management’s confidence is supported by strong promoter commitment, a healthy financial position, proven execution capability and access to capital. The company turned debt-free in February 2026 and continues to generate healthy operating cash flows, providing financial flexibility for expansion.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131