Buy National Aluminium Company Ltd For the Target Rs. 220 by the Axis Securites

Recommendation Rationale

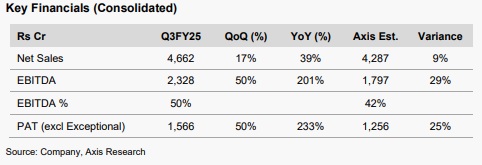

Overall beat: NALCO’s consolidated EBITDA grew by 200%/50% YoY/QoQ to Rs 2,328 Cr, a 30% beat vs. our and consensus, led by strong performance at both the Alumina and Aluminium divisions. EBIT at both divisions increased sharply, led by higher Alumina and Aluminium prices in Q3FY25.

Alumina refinery expansion: The 5th stream Alumina refinery of 1 mtpa is 70% complete and is expected to be commissioned by the end of FY26 from earlier guidance of Sep’25 (Q2FY26). The Pottangi Bauxite Mine (111 MT reserves) of 3.5 mtpa capacity will secure the bauxite supply for the alumina refinery expansion is also expected to start by the end of FY26. Utkal coal blocks D & E of 2 mtpa each will be operated as a single block for cost optimisation. Of the 7 MTPA coal needed for CPP, 3MTPA was produced in FY25, and it will increase this to 4 MTPA in FY26, replacing all the e-auction volumes required earlier. The majority of the benefit from captive coal is now already in the power costs

Aluminium smelter expansion of 0.5 mtpa capacity with a Capex of Rs 17,000 Cr is likely to be installed by FY30, along with a 1,200 MW CPP with a Capex of Rs 13,000 Cr in a JV with NTPC. Capex will kickstart with ~10-15% of initial spend in FY27, and spending will rise to 25% in subsequent years. It will float a tender for the project within the next 6 months and award the project within the next 7-8 months.

Sector Outlook: Neutral

Company Outlook & Guidance: A spike in Alumina prices led to strong Alumina realisation at $641/t in Q3FY25. In Q4FY25, it is likely to stay strong at $600/t, while Alumina sales volumes will rise to 4 LcT vs. 3.75 LcT in Q3FY25. As a result, Q4FY25 will be another good quarter. Spot Alumina prices have now corrected from the peak of $800/t to $530/t and could cool down further towards $450-$500/t. The lower Alumina prices will flow from Q1FY26 onwards. Earnings growth could moderate in FY26. We cut our Alumina and Aluminium price assumptions for FY26/27, resulting in EBITDA cuts of 4%/3% for FY26/27. However, we build 5 LcT additional Alumina volumes in FY27 from the 5th Stream of Alumina refinery, which partly offsets the decline in EBITDA from the downward price revision of Alumina and Aluminium. We model slightly lower sales volume against the management guidance of 7-8 Lc tonnes to factor in ramp-up delays. Delays in refinery expansion, along with a fall in Alumina's price, are key Risks.

Current Valuation: 6.0x EV/EBITDA on Dec’26E EBITDA (from 7.0x Sep’26E EBITDA)

Current TP: Rs 220/share (Earlier TP: Rs 250/share)

Recommendation: We maintain our BUY rating.

Financial Performance: NALCO’s Revenue/EBITDA/PAT beat our and consensus estimates because of strong performance by both the Alumina and Aluminium divisions. Consolidated revenue at Rs 4,662 Cr (up 39%/17% YoY/QoQ) stood ahead of consensus estimate by ~6%. EBITDA at Rs 2,328 Cr (up 201%/50% YoY/QoQ) beat the consensus estimates by 30%, led by a higher topline, while RM and employee costs remained under control. PAT stood at Rs 1,566 Cr (up 233%/50% YoY/QoQ), a 32% miss vs the consensus estimate, led by an EBITDA miss. The company has declared 2nd interim dividend of Rs 4/share for FY25. (Rs 4/share 1st interim in QFY25)

Outlook Nalco’s timely expansion and ramp-up of the 5th stream Alumina refinery with a 1 MTPA capacity by FY26 will be crucial. The Capex for it has already undergone a cost overrun. The company has plans of Rs 30,000 Cr Capex for the 0.5 MTPA smelter and 1,200 MW CPP. The Capex will increase materially from FY28, and execution will be the key. It has guided a capital structure of a 70:30 leverage ratio for the expansion.

Valuation & Recommendation We value the company at 6.0x Dec’26E EBITDA (from 7.0x and Sep’26E) and 0.5x book value of CWIP (unchanged). The TP at Rs 220/share (From 250/share) implies an upside of 20% from the CMP. We maintain our BUY rating on the stock.

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633