Buy Max Financial Services Ltd for the Target Rs.2,050 by PL Capital

Growth to sustain; margin outlook positive

Quick Pointers:

* 30% APE growth in Q3 led by protection and PAR; expect momentum to sustain

* Q3 VNB margin resilient at 24.1%; drag from GST exemption to be offset by favorable product mix

Q3FY26 APE grew 30% YoY driven by robust growth in protection and PAR segments and company expects the momentum to continue. We build in APE growth of 18%/17% in FY26/FY27E driven by a strong uptick in retail protection post GST exemption, new launches in PAR/NPAR/annuity, and recovery in credit life volumes. Q3 VNB margin was resilient at 24.1%, and the company expects the drag from GST exemption to be offset by a favorable product mix. We revise our margin estimates upward to 24.4%/ 24.7% for FY26/ FY27E, factoring in strong performance in 9M and gradual margin recovery. We value MAXF using the appraisal value framework with TP of Rs2,050 (2.2x FY27E P/EV vs. 2.1 earlier). Strong outlook on growth and margin trajectory are the positives. Reiterate ‘BUY’

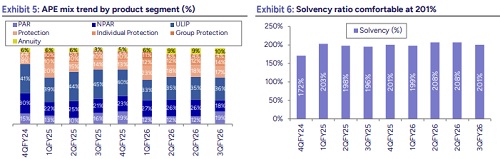

* Growth momentum to sustain: Q3 APE saw strong growth of 30% YoY to Rs27.3bn, led by protection (+59% YoY) and PAR (+54% YoY) segments. ULIP/NPAR grew 6%/ 12% YoY as the company focused on new launches – STAR ULIP and Smart VIBE. Group credit life grew by 45% in Q3FY26 with a pick-up in MFI and HL disbursals across partners. Annuity grew 3x YoY (on a small base) driven by the launch of newer limited pay variants. PAR/ NPAR/ ULIP/ Protection/ Annuity comprise 19%/ 18%/ 36%/ 17%/ 10% of Q3 APE. 9MFY26 APE grew 21% YoY, and the company is confident of sustaining momentum in Q4FY26/FY27. We build in 18%/17% APE growth in FY26/FY27E driven by a strong uptick in retail protection, new launches in PAR/NPAR/ annuity, and steady demand across ULIP and credit life

* FY26 VNB margin to range at 24-25%: Q3 VNB grew 35% YoY to Rs6.6bn. Despite the drag from GST exemption, Q3 VNB margin stood resilient at 24.1% led by a favorable product mix. The company reiterated a gross impact of 300- 350bps on FY26E VNB margin due to non-availability of Input Tax Credit (ITC). However, it is undertaking various measures such as distributor renegotiations, and cost optimization/ efficiency initiatives to mitigate the impact. Moreover, strong growth in retail protection and high-sum-assured ULIP is likely to absorb the impact. 9MFY26 VNB margin stood at 23.6%, and the company reiterated a guidance of 24-25%, considering the drag from GST exemption. We revise our FY26/ FY27E VNB margin estimate upward to 24.4%/ 24.7% as the share of protection increases.

* EV grows 16.5% YoY with operating RoEV of 16.9%: 9MFY26 total cost ratio stood elevated at 15.8% (vs. 14.9% in 9MFY25) due to the impact of the new labor codes (Rs600mn) and ITC disallowance (Rs2.95bn). Embedded value grew 16.5% YoY to Rs281.1bn and operating RoEV stood at 16.9%. 13M persistency dropped to 85% for 8MFY26 (vs. 87% for 8MFY25) due to poor performance of certain cohorts (0-surrender policies). However, the management highlighted taking corrective action in the segment with a reduction in the proportion of these policies in the overall book. AUM grew 12.2% YoY to Rs1,926.7bn. Solvency continued to be comfortable at 201% aided by debt raise of Rs8bn during Q2FY26.

* Both banca and proprietary contributing to growth: Proprietary and partnership channels contributed almost equally (49.5% and 50.5%, respectively) to Q3 APE. Growth was led by the proprietary channel (54% YoY) across agency, direct and e-commerce. Axis Max Life continues to maintain leadership position in online protection and savings business (rank #1). Agency remains a core focus area for the company, and it is activating more agents to drive growth. While the company has seen positive growth momentum in Axis Bank, it highlighted a pick-up in new banca partners (counter share at ~25%) and remains focused on consolidating its presence in the channel. It has added 51 new partners in 9MFY26, which now contribute to ~5% of APE.

Above views are of the author and not of the website kindly read disclaimer