Buy Lemon Tree Hotels Ltd for the Target Rs. 150 by Motilal Oswal Financial Services Ltd

Fleur expansion and asset-light scale-up strengthen growth outlook

Earnings in line with estimates

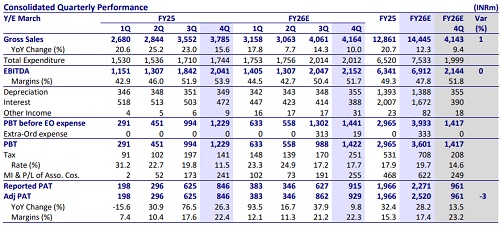

* Lemon Tree Hotels (LEMONTRE) reported healthy revenue growth of 10% YoY in 4QFY26, led by 17%/29%/6% YoY growth in FnB revenue/ Management fees/Room revenue. Average room rate (ARR) grew 6% YoY to INR7,457, with occupancy rate (OR) expanding 100bp YoY to 78.5%.

* LEMONTRE reported industry-leading EBITDA margins at 51.7% in 4QFY26, which were, however, impacted by higher investments in renovations and technology and the GST impact, leading to a 220bp YoY contraction.

* As mentioned in our recent note, going forward, we expect LEMONTRE to show healthy growth, primarily led by aggressive expansion through Fleur (pipeline of 3,375 keys), accelerating asset-light management fee income, premiumization via Aurika, and improving operating leverage as renovation cost, GST, and tech-related cost pressures normalize from FY27 onward.

* We largely maintain our FY27/FY28 EBITDA estimates and reiterate our BUY rating on the stock with our SoTP-based TP of INR150.

Stable quarterly performance supported by ARR growth

* Revenue grew ~10% YoY to INR4.2b (est. in line) in 4QFY26. OR expanded 96bp YoY to 78.5%. ARR increased 6% YoY to INR7,457. Management fees grew 29% YoY to INR206m.

* EBITDA grew 5% YoY to INR2.2b (est. in line). EBITDA margin contracted 220bp YoY to ~51.7% (est. 51.8%). Adj. PAT grew ~10% YoY to INR929m (est. in line), adjusted for exceptional items of INR19m (restructuring expenses).

* For FY26, revenue/EBITDA/adj. PAT grew 12%/9%/28% to INR14.4b/INR6.9b/INR2.5b.

* Gross debt stood at INR15b vs. INR17b as of Mar’25. Further, CFO stood at INR54.2b (largely flat vs. Mar’25).

Highlights from the management commentary

* Fleur: Backed by Warburg Pincus and a stronger balance sheet, management is evaluating multiple greenfield, brownfield, and acquisition opportunities, with ~2,500 rooms currently under discussion, primarily in the upscale and upper-upscale segments across top Indian cities. Expansion timelines vary from immediate contributions for operational acquisitions to 3-4 years for greenfield projects.

* Renovation: 400-500 rooms were under renovation in 4Q, with renovation activity typically peaking in summer and moderating during winter. Key projects such as Keys Whitefield, Lemon Tree Premier Bengaluru, Keys Hosur Road, and Red Fox Delhi (rebranded as Lemon Tree Hotel Delhi) are at various stages of completion, while Keys Pimpri Pune has already been fully renovated.

* Restructuring: After reorganization, Lemon Tree shareholders will effectively own ~58% of Fleur vs. 46% currently, while benefiting from management contracts that provide stable fee income and operational synergies between the two entities. Although Fleur will retain flexibility to partner with other brands where commercially viable, Lemon Tree is expected to remain a preferred partner given its strong operating track record. The demerger process is expected to take 12-18 months, depending on NCLT approvals.

Valuation and view

* LEMONTRE is expected to maintain a healthy growth momentum going forward, led by: 1) accelerated growth in management contracts (pipeline of ~13,300 rooms), 2) rebranding of existing hotels, 3) expansion of the Aurika portfolio, 4) strong backup from Warbug Pincus, 5) increase in yield due to the completion of renovation across brands, and 6) the addition of owned hotels through Fleur (3,375 keys).

* We expect LEMONTRE to post a CAGR of 11%/14%/22% in revenue/EBITDA/adj. PAT over FY26-28, with RoCE improving to ~18.7% by FY28 from ~13.1% in FY26. We reiterate our BUY rating on the stock with our SoTP-based TP of INR150 for FY28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412