Buy Laxmi Dental Ltd for the Target Rs.540 by Motilal Oswal Financial Services Ltd

A brighter SMILE awaits!

A strong growth trajectory bringing joy to every smile

* Laxmi Dental (Laxmiden) is distinguished as India’s only fully integrated provider of dental solutions, led by a highly experienced management team with extensive expertise in the field.

* Over the past two decades, the company has established an extensive Business-toBusiness-to-Consumer (B2B2C) network that encompasses over 22,000 dental clinics and dentists across 320 cities, while also exporting its products to more than 90 countries. Its early investment in digital dentistry, with more than 160 intraoral scanners (IOS) deployed domestically, has reinforced its leadership in technology adoption.

* Laxmiden’s business encompasses three high-growth pillars: custom labs (crowns and bridges), aligner solutions (clear aligners, thermoforming sheets, and resins), and pediatric dental products (Bioflex zirconia crowns and SDF), all of which are experiencing strong momentum.

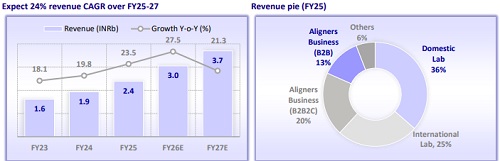

* The company’s revenue surged to INR2.4b in FY25, up from INR1.4b in FY22, with the EBITDA margin notably improving to ~17.5% from 4%. Laxmiden’s PAT increased to INR262m in FY25, recovering from a loss in FY22.

* Anchored by its digital edge, premium product focus, and extensive distribution reach, Laxmiden is well-positioned to achieve sustained growth and drive further margin expansion. Accordingly, we estimate a revenue/EBITDA/PAT CAGR of 24%/48%/62% to INR3.7b/INR900m/INR685m during FY25-27.

* Considering the supportive industry trend and Laxmiden’s potential for sustained growth, we assign a 43x 12M forward earnings multiple to arrive at our TP of INR540. It is important to note that Laxmiden has no direct competitors in the listed space. The healthcare services sector is currently trading at an average 12M forward P/E multiple of 43-45x. The company’s select focus on therapies, a customized and scalable business model, and strong growth momentum have led us to assign a similar multiple to Laxmiden. We initiate coverage on the stock with a BUY rating. Our TP implies a 26% potential upside from current levels.

Industry tailwinds and a shift towards organized labs to fuel lab growth

* Laxmiden is the second-largest player in the domestic lab segment with over 22,000 dental clinics and dentists across 320 cities. It exports to more than 90 countries and has the largest export lab business.

* The industry is experiencing strong tailwinds driven by a highly fragmented market, a shift towards premium metal-free products, growing adoption of digital dentistry, a shift towards organized labs, and an increasing trend of outsourcing by the US labs to India.

* Laxmiden is the preferred partner for Heartland, one of the US's largest Dental Service Organizations (DSOs).

* It is one of the early companies to launch branded zirconia crowns under its brand name “Illusion Zirconia”.

* Laxmiden is among the leading importers of IOS in India, adopting digital dentistry for a large part of its workflow, and has employed more than 600 IOS (iScanPro) in India.

* Laxmiden’s legacy lab business, contributing 62% of sales, clocked a 15% CAGR to reach INR1.5b over FY22-25. Its domestic lab business clocked a 13% sales CAGR to reach INR871m in FY25 from INR596m in FY22. In addition, its international labs business posted a 17% sales CAGR to reach INR607m in FY25 from INR383m in FY22.

* We expect Laxmiden’s labs business to deliver a sales CAGR of 21% over FY25-27 to reach INR2.2b.

‘Clear aligners’ poised for rapid expansion

* The global clear-aligner market is projected to clock a ~15% CAGR to reach ~USD55b by 2030 from ~USD21b in 2023.

* Rising adoption of clear aligners, greater focus on aesthetics and increasing disposable income are expected to drive strong industry demand.

* Laxmiden is the only aligner company in India that is fully vertically integrated, having end-to-end capabilities from raw material to distribution.

* In the B2B2C model, Laxmiden sells customized clear aligners through the Bizdent unit while it manufactures and supplies thermosheets and machines required to market aligners under the Vedia-B2B model.

* Laxmiden launched clear aligners under the brand ‘Illusion Aligners’, which is the first Indian brand to receive 510(k) clearance from the US FDA in CY21 to market clear aligners.

* We believe the aligner segment can deliver a 33% CAGR over FY25-27 to reach INR1.4b in revenue by FY27.

Niche pediatric dental leader primed for robust growth

* The global pediatric crown dental market is expected to post a 7.5% CAGR over CY23-30, reaching USD3.5b.

* Laxmiden is the only Indian manufacturer of Silver Diamine Fluoride (SDF), which is cleared by the USFDA to treat dental caries among children. It also has a registered design for BioflxTM (a semi-flexible, tooth-colored, pre-formed dental crown for children) in India.

* We expect the segment to achieve a revenue CAGR of 31% over FY25-27 to reach INR449m, with an anticipated PAT of INR95m in FY27.

Valuation and view: Initiate coverage with a BUY rating

* The healthcare services sector is evolving, with business models focusing on specific therapies and subsequently creating a comprehensive ecosystem. The customized service aspect not only adds value for patients but also benefits companies, establishing a strong competitive advantage for sustainable growth.

* Laxmiden has developed a comprehensive framework to bridge the gap in dentistry, effectively addressing the needs of patients across all age groups while enhancing the efficiency of dental practitioners.

* The adoption of technology has resulted in improved prospects in the international market. By utilizing celebrity brand endorsements as part of its marketing strategy, the company has also expanded its offerings in the aligner segment.We model a 24% revenue CAGR, 690bp margin expansion, and 62% PAT CAGR over FY25-27 under our base case scenario. We also assign a 43x 12M forward earnings multiple to arrive at our TP of INR540, implying a potential upside of 24%.

* The bull case scenario builds in 37% revenue CAGR with 750bp margin expansion, and 79% CAGR in PAT over FY25-27, assuming faster coverage in the domestic market, increased scope of business in international markets, and strong off-take in aligner products. This would lead to a TP of INR750, based on 50 x 12M forward earnings multiple, implying a potential upside of 75%.

* The bear case scenario assumes 10% revenue CAGR with 270bp margin expansion due to a slower ramp-up in domestic lab business, gradual progress in contracts from direct sales organization (DSO) in international markets, and lesser impact of marketing in the aligner business. These factors would result in a TP of INR360, based on the 40x 12M forward earnings multiple, implying a potential downside of 16%.

* We initiate coverage on the stock with a BUY rating.

Key risks

* Delay in receipt of approvals to launch/register products in international geographies may affect revenue prospects.

* Slower adoption of technological development at the industry level may adversely affect the positioning of Laxmiden from a competition perspective.

* A slower scale-up of dentist coverage would reduce the growth pace of its domestic lab business.

* Better dental solutions substituting crowns/bridges may affect overall demand and, consequently, the business prospects of Laxmiden.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412