Buy Laxmi Dental Ltd for the Target Rs 290 by Motilal Oswal Financial Services Ltd

Beat on revenue & margins; lab offerings drive revival Scanner pull-through & iScope launch to boost FY26-28 earnings growth

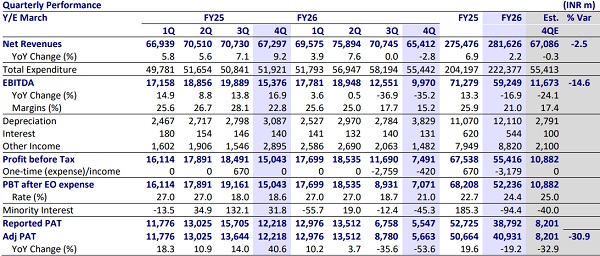

* Laxmi Dental (LAXMIDEN) delivered a better-than-expected financial performance with a 4%, 13%, and 6% beat on revenue, EBITDA, and PAT for 4QFY26, respectively. LAXMIDEN not only exhibited a YoY revival in sales growth but also showcased improved profitability.

* LAXMIDEN improved its growth in laboratory offerings across the domestic as well as the export segment. Compared to the stable sales run rate for the past two quarters in the domestic segment, it delivered 13% YoY growth in laboratory offerings (domestic) in 4QFY26. Even the international laboratory offering segment retained its growth momentum in 4QFY26/FY26.

* Scanner sales not only boosted its 4Q P&L but also provided commitment from the dentist community for subsequent sales of LAXMIDEN products & services.

* The aligner solution segment’s performance was weak as the company continued to find a balance between growth and profitability.

* LAXMIDEN has introduced ‘I Scope 360’ to connect dentists and patients conveniently in online mode and enable continuous tracking from home.

* We reduce our estimates by 6%/4% for FY27/FY28, factoring in

1) reduced off-take of aligner solutions

2) marketing and promotional expenses for innovative products

3) a gradual uptick in the paediatric business. We value LAXMIDEN at 30x 12M forward earnings to arrive at our TP of INR290.

* Despite global policy-related headwinds and rising competition, LAXMIDEN has improved its financial performance in 4QFY26 and ended FY26 with 16% YoY growth in revenue and 21% YoY growth in earnings. With increased scanner sales and the introduction of innovative solutions across focus markets, we expect earnings to alm

Superior revenue growth/better operating leverage fuel EBITDA growth

* Revenue for 4QFY26 grew 21.9% YoY to INR740m (our est: INR712m).

* EBITDA margin came in at 18.3% (our est: 17%), up 230bp YoY.

* EBITDA grew 41.8% YoY to INR135m (our est: INR119m).

* Adj. PAT grew 150.2% YoY at INR101m (our est: INR96m).

* Revenue/EBITDA/PAT grew 16%/4%/21% YoY in FY26

Reiterate BUY

* We reduce our estimates by 6%/4% for FY27/FY28, factoring in

1) reduced offtake of aligner solutions,

2) marketing and promotional expenses for innovative products, and 3) a gradual uptick in the paediatric business. We value LAXMIDEN at 30x 12M forward earnings to arrive at our TP of INR290.

* Despite global policy-related headwinds and rising competition, LAXMIDEN has improved its financial performance in 4QFY26 and ended FY26 with 16% YoY growth in revenue and 21% YoY growth in earnings. With increased scanner sales and the introduction of innovative solutions across focus markets, we expect earnings to almost double over FY26-28. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412