Buy Jio Financial Services Ltd for the Target Rs. 315 by Motilal Oswal Financial Services Ltd

Credit-led scale-up continues; newer businesses ramp up

NBFC AUM up ~35% QoQ; consol. PAT declines 14% YoY

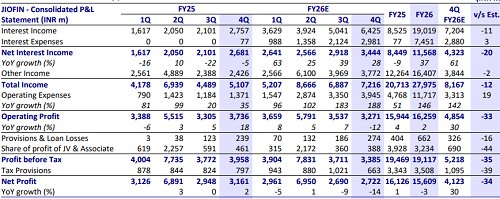

* Jio Financial Services (JIOFIN)’s 4QFY26 consolidated NII grew ~28% YoY to INR3.4b (PY: ~INR2.7b). Other income grew 55% YoY to INR3.8b. This included investment income of ~INR1.5b (PY: INR1.8b).

* Opex surged ~188% YoY to INR3.9b (PY: ~INR1.4b). Within this, employee expenses jumped ~136% YoY to INR1.3b. PPoP declined ~12% YoY to INR3.3b (PY: INR3.7b). For FY26, the PPoP grew 2% YoY to INR16.3b.

* Credit costs in 4QFY26 stood at INR274m (vs. INR239m in 4QFY25).

* The share of profit of JV & Associates dipped ~16% YoY to ~INR388m (PY: ~INR461m). Jio Payments Bank, which was earlier a JV, is now a whollyowned subsidiary of JIOFIN and is consolidated in JIOFIN’s financials.

* JIOFIN’s 4QFY26 consol. PAT declined ~14% YoY to ~INR2.7b (PY: INR3.2b). FY26 PAT declined ~3% YoY to INR15.6b.

NBFC Lending: Strong disbursement traction; AUM up 35% QoQ

* NBFC AUM grew ~35% QoQ to ~INR257b as of Mar’26 (vs. ~INR190b in Dec’25). Disbursements in 4QFY26 grew ~49% YoY and 23% QoQ to INR10.6b. NII in the NBFC business jumped ~150% YoY and stood at INR2b with PAT of INR710m, which surged ~305% YoY and 20% QoQ.

* Jio Credit’s Average CoF was broadly stable QoQ at 7% in 4QFY26 (vs. 6.99% in 3QFY26). Management shared that despite a volatile macro environment, the company was able to keep its cost of funds broadly stable.

* Portfolio mix remains balanced, with home loans at ~45%, loan against securities (LAS) at ~11%, and corporate lending at ~44%. The company plans to further diversify the asset mix by entering new segments and deepening its presence across key markets.

* CRAR stood at 25.91% with a D/E ratio of 3.05x as of Mar’26.

* We expect earnings momentum to strengthen every year, driven by a disciplined scale-up of business and a strong focus on profitability. We expect AUM CAGR of 85% and PAT CAGR of 162% over FY26-FY28E, with an RoA/RoE of 2.1%/11.7% in FY28E.

AMC: AUM at INR152b; rapid product expansion underway

* AMC AUM stood at INR152b (vs. INR150b as of Dec’25) with participation from 400+ institutional and 1.1m+ individual investors.

* JIOFIN shared that ~50% of its investors have active SIPs with the company, and over 20% of its investors are new to mutual funds.

* The product suite is expanding rapidly, with launches across short-duration, low-duration, thematic, and large-cap funds during the quarter, along with instant redemption features for liquid/overnight funds.

* Strategic intent includes building a full-stack investment platform, integrating mutual funds, ETFs, structured products, GIFT City offerings, and upcoming broking + wealth management.

Progress in other businesses

* Wealth and Broking: The wealth management business launched its website and an early access campaign, while the product roadmap and GTM strategy for broking remain under development.

* Jio Payments Bank (JPBL): Its CASA customers stood at ~3.7m (PQ: 3.2m), and it expanded the business correspondents (BC) network to ~378k (PQ: 287k). Deposits stood at INR5.44b as of Mar’26 (PQ: INR5.07b).

* Jio Payment Solutions (JPSL): Transaction processing volume has declined 8% QoQ to INR150b (PQ: INR163b). JPSL continues to focus on unit-level profitability, with net processing margin expanding to 12bp. Gross fee and commission income dipped 13% QoQ to INR840m in 4Q. The company received a payment aggregator-cross-border license from the RBI to settle global payments.

* Jio Insurance Broking: Premiums of INR2.7b were facilitated in 4QFY26.

Key highlights from the management commentary

* Management indicated that treasury performance was impacted by rising yields due to the relatively large treasury book; excluding this impact, underlying PPOP growth would have been stronger.

* Broking is not yet fully operational at scale, but it is a key upcoming pillar within the investment ecosystem. It will likely act as a high-engagement product, improving user stickiness and increasing cross-sell opportunities across lending, AMC, and derivatives of investment products.

Valuation and view

* JIOFIN reported a mixed performance, with the NBFC segment scaling well and AUM crossing INR 250bn; however, other segments witnessed slower traction, while overall profitability remained impacted by continued investments in new businesses and the impact on the treasury book amid macro volatility.

* JIOFIN offers a compelling long-term runway for growth, supported by the breadth of its financial services platform and multiple embedded value-creation levers. While current valuations reflect a part of the medium-term growth potential, we believe they do not fully capture the scale opportunity across lending, asset management, insurance, and digital financial services as these businesses transition from incubation to meaningful profitability.

* JIOFIN trades at 1x FY27E P/BV. We model a consolidated PAT CAGR of 50% over FY26-FY28 and reiterate our BUY rating on the stock with a TP of INR315 (based on Mar’28E SoTP). Our SoTP does not factor in valuation from businesses like insurance manufacturing, wealth management, broking, and marketplace, which are still in their incubation phase.

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412