Buy Interglobe Aviation Ltd for the Target Rs.5,500 by Motilal Oswal Financial Services Ltd

Disruption extended through 4Q; fundamentals remain strong

An escalation in geopolitical conflicts has triggered material airspace disruption across critical international corridors, creating a multi-layered impact on IndiGo’s network, revenue, and cost structures, with meaningful implications for the nearterm earnings trajectory and margin resilience.

* An escalation in the US-Iran conflict and the Pakistan airspace closure have rendered key Middle Eastern corridors inaccessible, disrupting IndiGo’s Gulf network and parts of Europe, as all westbound routes traverse this region, constraining operations across critical international markets.

* This impact is amplified by the Middle East’s dual role as a large origindestination market and a transit hub for Europe-bound traffic, with the UAE alone contributing ~30% of India’s international flows, directly affecting both core revenue and network connectivity. Airspace restrictions have forced cancellations and rerouting, limiting IndiGo’s ability to monetize demand despite underlying strength in passenger traffic.

* Consequently, revenue impact is two-fold: immediate loss from flight cancellations across Gulf routes contributing ~18-20% of total revenue, and a lagged effect from weaker forward bookings as demand remains suppressed due to uncertainty and limited alternatives.

* Simultaneously, the spike in Brent crude prices to ~USD113/bbl (from USD60- 65/bbl) in Mar’26 has pushed ATF costs higher to ~INR115/liter in 4QFY26, implying an incremental cost impact of ~INR16b (i.e., ~22%/43% of FY25/FY26E PAT would be eroded), with fuel forming ~30-35% of costs, thereby exacerbating margin pressure. As per our calculation, every USD1/bbl increase in crude prices reduces profitability by ~INR3.6b. In extreme scenarios, airlines typically implement fuel surcharges to offset rising fuel costs. IndiGo has introduced surcharges of INR425-INR2,300 across routes, partially mitigating the impact, with an estimated offset of ~INR1b for every USD1/bbl increase in crude prices.

* In addition, the rerouting of European flights via Africa adds 3-4 hours per sector, increasing fuel burn, crew costs, and operational complexity, while straining FDTL limits, reducing flexibility and further elevating per-flight costs.

* Finally, INR depreciation compounds cost pressures given IndiGo’s USD-linked cost base, with each INR1 depreciation to USD adding ~INR9b to costs, while reduced international operations weaken natural hedging, creating a sustained earnings headwind beyond the disruption period.

* Factoring these headwinds of higher fuel costs, INR depreciation and lower international operations leading to adverse operating leverage, we have reduced our FY26 and FY27E EBITDAR estimates by 7% each, and PAT estimate for FY26/FY27/FY28 by 31%/15%/10%.

* We reiterate BUY with a reduced TP of INR5,500, valuing it at 9x FY28E EBITDA (implied P/E on FY28E is 25x).

Airspace restriction in key international route due to conflict

* Just as IndiGo was exiting the FDTL disruption and managing a more stable 4QFY26 schedule, a far more externally-driven shock emerged.

* The escalation of the US-Iran conflict from late Feb’26, compounded by the continued Pakistan airspace closure for Indian carriers, has effectively neutralized IndiGo's entire Middle East and large portions of its European network for the time being. This resulted in the progressive closure and restriction of the Middle East airspace across a corridor that handles ~25% of global international air traffic by passenger volume.

* For Indian carriers, this corridor is uniquely consequential. All of IndiGo's westbound international flights to UAE, Saudi Arabia, Bahrain, Kuwait, Oman, Qatar, and onward to Europe and North Africa pass through or near the affected airspace.

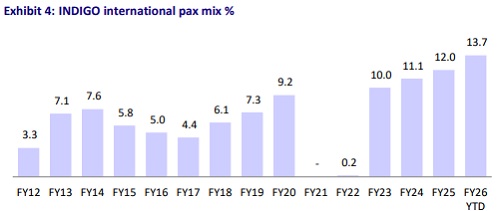

* The Middle East is not simply a transit zone for Indian carriers; it is simultaneously a large origin-destination market and a critical intermediate routing layer for European services. The UAE alone accounts for ~30% each of India's total outbound and inbound international passenger traffic since most routes are largely two-way origin-destination (O-D) flows (workers, diaspora visits, tourism, business).

* The dual function means that the airspace closure affects IndiGo in two distinct ways: it directly eliminates Gulf origin-destination revenue, and it forces longerroute rerouting for European services that cannot use the standard Iran-overfly routing.

* This is not a demand-side shock; load factors on affected routes were healthy before the closure. It is a pure supply-side constraint, driven by airspace access.

* The revenue impact of the Middle East disruption is felt in two dimensions.

* The first is direct: The cancellation of flights on Gulf routes eliminated revenue from those sectors outright. The cancellations concentrated on the highestfrequency sectors: Dubai, Abu Dhabi, Sharjah, Riyadh, Jeddah, Dammam, Muscat, Doha, Bahrain, and Kuwait, collectively IndiGo's most commercially important international route group. IndiGo's international revenue accounts for 23% of total revenue, with Gulf routes generating an estimated INR145- 160b of annual revenue in FY25 (i.e., ~18-20% of total revenue). A complete suspension of these routes for the disruption period, combined with the booking uncertainty effect that suppresses advance sales even on routes that continue to operate, creates a revenue shortfall concentrated in 4QFY26.

* The second dimension is more insidious: Airspace disruptions are causing forward-booking softness, as travelers delay bookings when routes are uncertain and alternatives are limited. This particularly affects India-Gulf migrant and diaspora traffic, which cannot easily shift to other airlines since major carriers like Emirates, flydubai, and Air Arabia are all operating restricted schedules due to the same regional airspace issues. With over 23,000 flight cancellations, demand is suppressed rather than diverted. Once operations normalize, revenue typically rebounds quickly, but advance bookings usually take 4-6 weeks to return to normal levels.

ATF: The cost amplifier that compounds both disruptions

* The Middle East escalation has introduced a concurrent fuel cost shock that is independent of but simultaneous with the rerouting cost increase.

* Brent crude, which had been trading in the USD60-65/bbl range through 2HFY26, spiked toward USD113/bbl in early Mar’26 as market participants incorporated supply disruption risk from Iranian production infrastructure, Gulf terminal vulnerability, and Strait of Hormuz transit risk. ? Aviation turbine fuel (ATF) prices in India, set fortnightly by Indian Oil Corporation (IOCL) based on import parity calculations that incorporate international jet fuel benchmarks (primarily the Singapore jet kerosene marker), track crude with approximately a two-to-three-week lag, meaning the full impact of the March crude spike will be embedded in 4QFY26 ATF actuals with a minimal delay.

* The impact on IndiGo is magnified by its cost structure. ATF represents ~30-35% of IndiGo's total operating costs in a normalized environment. At the FY25 scale of operations, the company consumed roughly ~3b liters of ATF annually, a base that grows by ~10-11% per year as ASKs expand.

* Our prior FY26E ATF assumption of ~INR91/liter reflected a modest decline from FY25 levels of INR94.7/litre on the basis of earlier crude price softness. The Mar’26 spike forces a revision to ~INR115/litre for 4QFY26E. The difference between INR94/litre (our 4QFY26 ATF assumption) and INR115/litre across ~0.8b liters of quarterly consumption implies roughly ~INR16b of additional annual fuel costs in 4QFY26 alone (i.e., ~22%/43% of FY25/FY26E PAT would be eroded).

* Further, every USD1/barrel increase in crude prices will directly impact the company’s profitability by ~INR3.6b (i.e. 3-4% of FY28E PAT). This can be partly offset by implementing a fuel surcharge, which INDIGO recently announced, ranging INR425 (domestic) to as high as INR2,300 (international) across domestic and international destinations. This will partly offset the fuel price impact by INR1b per dollar change in crude price.

* If higher crude prices continue for an extended period, then the cost implications will be much higher in FY27.

* Further, the Ministry of Civil Aviation had imposed domestic airfare caps during the FDTL-led disruption of Dec’25 to protect consumer interests. These caps have been lifted recently, which is a modest positive for airlines as it restores pricing flexibility at a time when rising crude prices are squeezing margins.

* That said, the ministry has made clear that any excessive or unjustified fare increases will remain under close regulatory scrutiny, effectively capping the practical upside from this pricing headroom.

* The quantum of pass-through to ticket prices will become clearer from 1st Apr’26, when ATF prices are due for their next fortnightly revision by IOCL — the first reset that will fully reflect the Mar’26 crude spike in domestic jet fuel price.

Rerouting and INR depreciation add to the cost impact

* The operational complexity has also been compounded by Africa-rerouting requirements. Flight 6E033 from Delhi to Manchester returned to base after seven hours in the air when last-minute Eritrean airspace restrictions were invoked.

* European Union Aviation Safety Agency (EASA) directives and ME corridor closure together require IndiGo to reroute westbound services through subSaharan Africa, adding 3-4 hours of block time per flight. Each additional flight hour on a B787 or A320 in long-haul configuration translates to ~6-8% additional fuel burn, plus crew hour extensions that consume FDTL headroom that was still being rebuilt. IndiGo's own spokesperson confirmed that flights may take longer routes or experience diversions as the ME situation evolves.

* Moreover, the INR/USD exchange rate creates an additional, structurally persistent cost layer that is often underappreciated in near-term disruption analysis. IndiGo's lease obligations, which represent the single largest item in its cost structure, are entirely denominated in USD; aircraft and engine maintenance reserve payments, spare parts sourcing, certain ground handling costs at international stations, and navigation fees payable to international air navigation service providers (ANSPs) are similarly USD-linked.

* This is also a double whammy as international travel acts as a natural hedge to the company’s forex exposure. Slowdown/hiatus in the international travel will result in a significant loss of forex, thereby increasing the cost.

* In terms of MTM exposure to USD/INR, INR1 depreciation against USD adds ~INR9b to annualized operating costs. With INR having moved from ~INR84- 85/USD in FY25 to an estimated INR88.6/USD average for FY26E and likely INR91/USD in FY27E and further to INR94/USD for FY28E given current account dynamics and global USD demand, the cumulative exchange rate headwind over FY26-FY28E is ~INR90b, and unlike fuel, this headwind does not reverse when airspace reopens.

Valuation and view

* The ongoing airspace disruption represents a meaningful near-term earnings overhang for IndiGo, driven by a combination of network dislocation, revenue loss, and elevated cost pressures. The supply-side nature of the shock limits mitigation, with cancellations and booking softness likely to weigh on 4QFY26 performance.

* While demand fundamentals remain intact and recovery should be swift once normalcy resumes, the concurrent fuel cost spike, rerouting inefficiencies, and forex headwinds could extend margin pressure beyond the disruption window, thereby impacting earnings visibility to early FY27 despite partial offsets through pricing actions.

* Over the longer term, we remain confident in the company’s growth strategy. INDIGO’s domestic network remains the backbone of its operations, supporting India’s travel and tourism evolution, while expanding international connectivity provides a natural hedge and enhances margins.

* We expect its revenue/EBITDAR/Adj. PAT to clock a CAGR of 11%/13%/6% over FY25-28. We reiterate BUY with a reduced TP of INR5,500, valuing at 9x FY28E EBITDA (implied P/E on FY28E is 25x).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041