Buy Hero Motocorp Ltd for the Target Rs. 6,248 by Motilal Oswal Financial Services Ltd

Steady quarter Rural recovery bodes well for HMCL

* Hero MotoCorp’s (HMCL) 4QFY26 PAT at INR14b came in line with our estimate. Margins remained stable YoY despite the ramp-up in its EV business.

* We expect HMCL to benefit from a gradual rural recovery, given the strong brand equity in the economy and executive segments. Its focus on ramping up presence in scooters (both ICE and EVs) and exports is likely to help drive volume growth. We project HMCL to deliver a CAGR of ~10%/9%/9% in revenue/EBITDA/PAT over FY26-28. At ~18.3x/16.2x FY27E/28E EPS, the stock appears attractively valued. We reiterate our BUY rating with a TP of INR6,248 (based on 18x FY28E EPS + INR89/419 for Hero FinCorp/Ather after 20% holdco discount).

Earnings in line with estimates

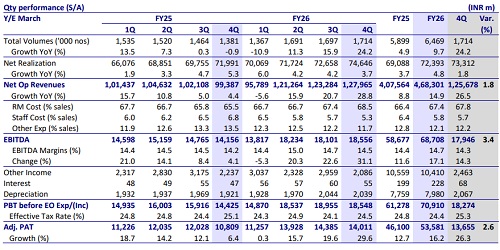

* 4Q net revenues grew 28.8% YoY (in line) to ~INR128b.

* Net realizations grew 3.7% YoY/2.7% QoQ to ~INR74.6k per unit. Volumes rose 24.2% YoY (flat QoQ) at 1.7m units.

* Gross margins contracted 300bp YoY to 31.5% (below the estimated 32.2%).

* EBITDA was up 31.1% YoY to INR18.6b, broadly in line with our estimates. EBITDA margins marginally expanded 30bp YoY to 14.5% (in line).

* PAT came in line with our estimates at INR14b, up 29.6%.

* FY26 revenue/EBITDA/PAT grew 15%/17%/16% YoY, respectively, while CFO/FCF stood at INR83b/INR74b in FY26.

* RoCE/RoE in FY26 stood at 26%/25%, respectively.

Highlights from the management commentary

* In FY26, retail performance outpaced dispatches, which helped reduce channel inventory to five weeks, within which EV inventory stood at under 10 days.

* Management expects the domestic 2W industry to grow in high single digits in FY27, with scooters outpacing the motorcycle segment by a couple of percent points. HMCL expects to outperform the industry in both segments. ? Management expects the export momentum to continue over the next couple of years as it expands its product offerings and enters new markets.

* Near-term margins are expected to remain under pressure due to commodity inflation, but HMCL plans to partially offset the impact through price hikes and cost savings

* PLI has been approved for three products, covering around 60% of the EV portfolio, and this coverage is expected to increase to 90% in FY27.

* HMCL plans INR15b capex in FY27, focused on scooters, EVs, and a second parts center. Around INR7b of capex is earmarked for the second parts center in South India.

Valuation and view

* We expect HMCL to benefit from a gradual rural recovery, given strong brand equity in the economy and executive segments. Its focus on ramping up presence in scooters (both ICE and EVs) and exports is likely to help drive volume growth. We expect HMCL to deliver a volume CAGR of ~8% over FY26-28, driven by new launches and a ramp-up in exports.

* We project a CAGR of ~10%/9%/9% in revenue/EBITDA/PAT over FY26-28. At ~18.3x/16.2x FY27E/28E EPS, the stock appears attractively valued. We reiterate our BUY rating with a TP of INR6,248 (based on 18x FY28E EPS + INR89/419 for Hero FinCorp/Ather after 20% holdco discount).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041