Buy HCL Technologies Ltd for the Target Rs 1,450 by Motilal Oswal Financial Services Ltd

One eye on the future; near-term guidance maintained Investments in sovereign AI and data center stack encouraging

* HCL Technologies (HCLT) reported 1QFY27 revenue of USD3.6b, which declined 0.5% QoQ CC, above our estimate of 1.4% QoQ CC decline. EBIT margin came in at 16.9%, in line with our estimate of 16.9%. New deal TCV was USD2.4b (up 32.8% YoY) in 1QFY27. For FY27, revenue growth guidance was maintained at 1–4% YoY in CC. Services revenue growth was also maintained at 1.5% and 4.5% YoY in CC (vs. our expectations of a guidance cut at the upper end). EBIT margin guidance of 17.5–18.5% was in line.

* For 1QFY27, revenue/EBIT/adj. PAT grew 13.9%/18%/20.3% YoY in INR terms. We expect revenue/EBIT/PAT to grow 9.3%/15.7%/20% YoY in 2QFY27. Free cash flow stood at 99% of net profit for 1QFY27. We reiterate our BUY rating with a revised TP of INR1,450, based on 18x FY28E EPS (earlier 16x). We maintain HCLT as our preferred pick in the large cap space.

Our view: AI playbook starts taking shape; margins still below longterm average

* Guidance maintained despite our expectation of a 100bp cut: HCLT retained its FY27 revenue growth guidance of 1–4% YoY CC and services growth guidance of 1.5–4.5% YoY CC, implying ~1% CQGR at the midpoint.

* The company reported its highest-ever 1Q bookings, while the recently announced USD1.14b mega deal (not part of 1Q TCV) provides additional comfort around achieving the midpoint of guidance. Management clarified that the deal will have a negligible revenue contribution in FY27 as it reaches steady state only by Apr'27. We expect the ramp-up to provide a stronger exit into FY28.

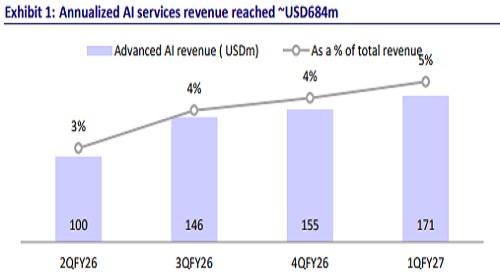

* Data center and Sarvam investments are encouraging: HCLT announced plans to invest up to INR35b to build a full-stack AI data center business, scalable to 50MW capacity. This follows its USD150m investment in Sarvam, India's sovereign LLM play. We believe HCLT is investing ahead of the market to build the next-generation AI stack.

* We believe a clearer playbook is now emerging through HCLT's fivepillar AI strategy transforming services, building differentiated IP, expanding AI-led services, strengthening AI partnerships, and scaling AI talent. This should help the company defend against, and eventually benefit from, AI disruption, and HCLT seems ahead of the curve here.

* Data center strategy is different from a traditional colocation model: Management highlighted that this is not a pure data center or capacity leasing business. The focus is on a full-stack offering that combines AIready infrastructure with software, managed services, sovereign AI capabilities, and SLMs. Investments will be phased and supported by committed client demand, partner funding, and a mix of equity and debt

* EBIT margins expanded sequentially, helped by lower restructuring costs and forex, partly offset by seasonal productivity commitments and weaker ER&D revenue. Management retained its FY27 EBIT margin guidance of 17.5%–18.5%, which already includes restructuring costs. We continue to expect margins to remain largely range-bound through FY27-28 as AI investments offset operating leverage.

* Vertical commentary remains mixed: BFSI remains the strongest vertical, supported by AI-led wallet share gains and healthy demand for data and analytics. Technology and telecom remain impacted by discretionary spending cuts at two large US telecom clients, weighing on ER&D growth. Life Sciences & Healthcare continues to face headwinds from the rollover of earlier regulatory programs and a weak US healthcare market.

Valuation and view

* We now expect HCLT to deliver a USD revenue CAGR of ~4%/INR PAT CAGR of 12.0% over FY26–28, with EBIT margins of ~17.8%. Client-specific issues in key verticals such as telecom have reduced HCLT’s growth premium in FY27E. That said, a potentially strong exit as well as continued strong deal wins could restore the gap in FY28E.

* We continue to like HCLT's all-weather portfolio. Its investments in Sarvam and the AI data center business strengthen its long-term AI positioning. We have kept our estimates unchanged and reiterate our BUY rating with a revised TP of INR1,450 based on 18x FY28E EPS (earlier 16x). We maintain HCLT as our preferred pick in the large-cap space.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412