Buy EPL Ltd for the Target Rs.270 by Motilal Oswal Financial Services Ltd

Building a scaled consumer packaging leader for emerging markets

EPL and Indovida (a leading global rigid PET packaging company and subsidiary of Indorama Ventures Ltd) have signed definitive agreements to merge, creating a ~USD1b revenue entity with a combined valuation of ~USD2b. The transaction will form one of the largest consumer packaging platforms in emerging markets, combining complementary capabilities to expand global reach, accelerate growth, and enhance margins and returns.

* Indovida is a leading global rigid PET packaging platform, with 19 facilities across nine countries (primarily in Southeast Asia and Africa), deriving ~90% of revenue from emerging markets; it operates mainly in preforms (~75% of revenue) and is supported by strong customer relationships, driven by high service quality, experienced management, reliable raw material access, and a diversified geographic footprint.

* For this merger, EPL is valued at ~USD1.2b (at INR339/share, i.e., ~70% premium to the 26th Mar’26 close), while Indovida India is valued at ~USD700m, at a ~35% discount to EPL’s multiple.

* The implied EV/EBITDA multiples are 12.5x for EPL and 8.1x for Indovida India, with EPL commanding a premium due to its strategic pivot toward the beauty & cosmetics segment and expansion into high-growth markets such as Brazil and Thailand.

* Post-merger, Indorama Ventures will become the co-promoter with a 51.8% stake (three board seats), while Blackstone will hold 16.6% (one board seat) in the combined entity.

* The merger is expected to result in sizable synergies of USD35-50m annually, driven by mutually leveraging each other’s moats, such as leading market positions in the key emerging markets, portfolio diversification, supply chain, and other costs synergies.

* This merger transforms EPL into a diversified multi-format packaging leader, expanding TAM from USD2.4b to USD29b, strengthening global presence and customer relationships while positioning the company for sustained growth across products, geographies, and emerging markets.

* EPL is trading at ~10.3x FY28E EPS of INR19.9 and ~5x FY28E EV/EBITDA. We value the stock at 14x FY28E EPS to arrive at a TP of INR270. We reiterate our BUY rating on the stock.

Indovida: A leading rigid PET player

* Indovida, wholly-owned by Indorama Ventures (99.99% stake), is a leading global rigid PET packaging platform that manufactures preforms, bottles, and closures for the food & beverage, healthcare, and broader consumer segments.

* The company operates 19 manufacturing facilities across nine countries, primarily in Southeast Asia and Africa, with ~90% of its revenue derived from emerging markets.

* Preforms contribute ~75% of the revenue, while the remainder comes from bottles and closures (equal split). Its strong customer franchise is driven by highservice quality, experienced management, reliable access to raw materials, and a well-diversified geographic footprint.

* The customer base includes leading global FMCG players such as Coca-Cola, PepsiCo, Nestlé, Unilever, P&G, L’Oréal, Danone, and ThaiBev. The company holds the #1 position in rigid packaging across the Philippines, Vietnam, and Nigeria, and ranks among the top two players in several other key markets, including Egypt, Thailand, Tanzania (recently entered), and Ghana.

* The company reported a revenue of INR38b in CY25 (~83% of EPL’s CY25 revenue), with healthy EBITDA margins of 21.3% and strong RoCE of 23.7%.

* 100% owned by Indorama Ventures, Indovida benefits from supply chain resilience, strong sustainability capabilities, and a growing footprint across emerging markets.

* Indovida is a net cash company, providing significant balance sheet flexibility to pursue future inorganic growth opportunities.

* Indovida currently has no presence in India; the merger provides a strategic entry into the market through EPL’s established platform.

Shareholding and transaction valuation

* The pre-merger shareholding of EPL includes ~26% of Epsilon Pte. (affiliate of Blackstone), 24.4% of Indorama Netherlands BV (‘Indorama BV’), and balance held by other shareholders.

* The swap ratio determined for the transaction is 286 fully paid-up equity shares (FV INR2) of EPL for every 10,000 fully paid-up equity shares (FV INR10) in Indovida India.

* Accordingly, upon the merger becoming effective, the share of Indorama BV would rise to 51.8%, while the revised shareholding of Epsilon and other shareholders would stand at ~16.6% and 31.6%, respectively.

* For the purpose of effecting this merger, EPL is valued at ~USD1.2b, with a per share price of INR339 (~70% higher than the closing price as of 26 Mar’26), resulting in a transaction value of ~INR62.6b for the shares issued to Indovida India. Indovida India is valued at ~USD700m (~35% discount to the multiple ascribed to EPL).

* The valuation is based on EV/EBITDA multiple of 12.5x and 8.1x for EPL and Indovida India, respectively, based on CY25 financials. EPL was valued comparatively at a higher multiple due to its pivot in the Beauty & Cosmetic category, along with its entry into emerging markets like Brazil and Thailand.

* Post-merger, EPL would be valued at ~USD2b. The merger is cash neutral and expected to be EPS accretive from the first full year of operation.

* The merger’s approval is pending from SEBI, CCI, Stock Exchanges, NCLT, Shareholders’, Creditors, and other regulatory approvals. The transaction closure (including approval period) is expected to occur in ~12 months

Strategy, synergies, and leadership strength

* This strategic merger is expected to drive incremental value for EPL through: 1) access to global operating expertise, capital support, and sustainability capabilities; 2) enhanced stability and continuity, enabling disciplined execution of strategic and investment plans; 3) stronger alignment with global customers, regulators, and employees; and 4) reinforcement of long-term structural value creation as a future-ready global packaging platform.

* The merger is expected to unlock significant synergies (~USD35m-50m), driven by mutually leveraging leadership positions in key emerging markets, along with portfolio diversification and supply chain and cost optimization.

* The merger enables EPL to leverage Indovida’s established presence and local expertise in key emerging markets (notably Africa and Vietnam), while also providing access to new geographies, thereby accelerating market entry, reducing execution risks, and deepening customer engagement through a broader multi-format portfolio.

* The combined scale and shared infrastructure are expected to drive cost efficiencies and improve capital allocation, while increased financial flexibility supports faster expansion and potential inorganic growth opportunities.

* Further, Indovida’s positive net cash position is expected to reduce EPL’s postmerger leverage (net debt/EBITDA ~0.25x from 0.65x in CY25), enhancing financial flexibility to pursue margin-accretive inorganic opportunities.

* The merger also lays the foundation for expansion into adjacent specialty packaging segments, including specialty caps & closures and rigid containers for the beauty and cosmetics industry (each with a global market size of ~INR 800b900b), enabling deeper customer penetration and cross-selling opportunities.

* EPL is expected to benefit from procurement efficiencies, vendor consolidation, and logistics optimization, along with shared infrastructure and centralized support functions, driving structural cost savings, improved operational efficiency, and sustained margin expansion.

* Indovida’s experienced management team will strengthen EPL’s leadership, bringing proven execution capabilities and deep expertise in emerging markets.

* This merger aligns with Indorama Ventures’ strategy to deepen its presence in India and supports its IVL 2.0 focus on building market leadership through partnerships and value-accretive investments.

* Indorama’s strategic parentage is expected to enhance EPL’s access to global operating expertise, capital support, sustainability capabilities, strengthening alignment with global standards and drive further value creation.

Building a scaled, high-growth packaging leader in emerging markets

* EPL currently stands as a global leader in packaging, underpinned by a strong foundation and consistent execution. The company has delivered robust growth, with revenue/EBITDA/Adj. PAT CAGRs of 7%/13%/19% over FY22-FY25, while maintaining a significant ~60%+ revenue contribution from emerging markets.

* The merged entity will leverage EPL’s and Indovida’s strong positions in emerging markets, accounting for ~75% of the companies’ revenue, along with their complementary geographic footprints to drive enhanced growth.

* EPL and Indovida’s combination will create one of the largest consumer packaging platforms in emerging markets, with a network of 40 manufacturing facilities spanning 17 countries.

* The merged entity’s exposure to emerging markets underpins a strong growth outlook, with these markets expanding at nearly 2x the pace of developed economies.

* The laminated tube market in emerging regions is projected to expand at a ~6- 6.5% CAGR over FY24-FY30, outpacing the ~4% CAGR in developed markets. Similarly, the rigid PET market in emerging regions is expected to expand at ~5% CAGR over FY25-FY30, compared to ~2% CAGR in developed markets.

Valuation and view

* The merger is expected to transform EPL into a diversified, multi-format packaging platform (rigid and flexible packaging) with a strong presence across high-growth emerging markets (combined 75% share), supported by an increased focus on innovation for both large and emerging brands.

* EPL’s TAM will increase to USD29b (addition of Rigid PET market size of USD26.6) from USD2.4b (laminated tubes market). The combined entity’s enhanced capabilities, deep customer relationships, and expanded global footprint are likely to strengthen its positioning as a preferred partner for customers, enabling it to drive sustained growth across product categories and geographies.

* We expect EPL, on a standalone basis, to continue delivering healthy operating performance across geographies, supported by robust demand, ongoing product innovation, and an improving sustainability-led mix, with management reiterating its double-digit revenue growth guidance.

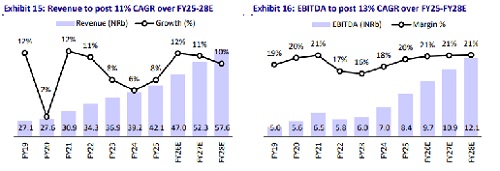

* We expect a revenue/EBITDA/PAT CAGR of 11%/13%/21% over FY25-28 and value the stock at 14x FY28E EPS to arrive at a TP of INR270. We reiterate our BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041