Buy Coforge Ltd for the Target Rs.1,880 by Motilal Oswal Financial Services Ltd

Pricing in the extreme?

Despite near-term risks, valuations look attractive after recent correction

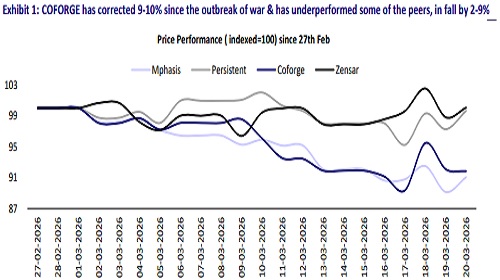

* Since the US–Iran conflict broke out, Coforge Ltd (COFORGE) has witnessed a decline of 9-10% (45% from its peak) and underperformed some of its mid-cap peers by 2-9% (refer to Exhibit 1); Coforge seems to have two disadvantages vs peers: (1) relatively higher exposure to the travel vertical vs peers, & (2) Middle East exposure.

* Even so, we believe the stock is currently pricing in an extreme bear-case scenario. As shown in Exhibit 3, the stock trades at 20x FY28E P/E, assuming a bear case of 10% organic constant currency growth rate in FY27/FY28E.

* At current levels, valuations appear attractive (19x/15x FY27/28E P/E), even on our pared estimates.

* COFORGE is now trading at large-cap multiples, and barring any extreme change in direction, we still expect it to remain one of the fastest-growing IT services companies, with scope for margin recovery in the near term.

* We believe COFORGE’s strong executable order book and resilient client spending across verticals bode well for its organic business. Cross-sell opportunities in Cigniti remain highly synergistic for the company, and COFORGE’s sales engine still remains the best in class.

* Factoring in travel-vertical risks, we pare our estimates by 4-6%. Additionally, considering AI-related uncertainties in IT services, we lower our target multiple to 26x (from 32x), valuing the stock at INR1,880, implying a 73% upside.

Meaningful travel exposure remains sensitive amid war

* Travel and transportation is a key vertical for COFORGE, contributing ~22- 23% of revenue as of 3QFY26. The company serves airlines, airports, OTAs, and hospitality clients.

* Travel has been by far COFORGE’s fastest-growing vertical over the past three quarters, driven by the Sabre deal ramp-up.

* The Sabre deal is now fully ramped up, and the ongoing war could potentially slow growth in this vertical.

MEA exposure weighs on uncertainty

* We assess that COFORGE has high exposure to the Middle East, with our estimates suggesting ~5% of revenues linked to the region.

* We do not believe this is material in the long term, but it may weigh on near-term revenue growth.

* If the war persists, we will monitor potential risks to deal closures in the MENA region for COFORGE.

* Our bear-case scenario assumes FY27–28E organic growth could moderate to ~10%, while post-Encora acquisition, we expect EPS dilution of 7-9% across FY27-28 in this scenario.

Margin levers to provide room for expansion

* The company is now past its wage hike cycle, with levers such as lower ESOP costs and D&A expenses providing room for margin expansion going forward.

* We estimate EBIT margins to hover around 14%/14.3% in FY27/FY28, higher than the 13-13.5% range observed over the past couple of years.

Valuations and view

* We believe COFORGE’s strong executable order book and resilient client spending across verticals bode well for its organic business. Cross-sell opportunities in Cigniti remain highly synergistic for the company.

* We believe the stock is currently pricing in an extreme bear-case scenario. At current levels, valuations appear attractive (19x/15x FY27/28E P/E). Factoring in risks related to the travel vertical, we pare our estimates by 4-6%. Additionally, considering AI-related uncertainties in IT services, we lower our target multiple to 26x (from 32x), valuing the stock at INR1,880, implying a 73% upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041