Buy CIE Automotive India Ltd for the Target Rs.546 by Motilal Oswal Financial Services Ltd

India business likely to resume outperformance

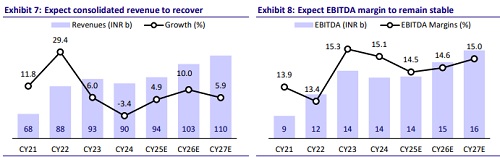

We hosted CIE India management for a non-deal roadshow, and below are the key takeaways. Over the last few quarters, CIE had witnessed slower growth in its India business; however, this trend has reversed after GST rate cuts, which have boosted demand across all segments. Moreover, it has bagged new orders from non-anchor customers, which are expected to ramp up in the coming quarters and help drive its longpromised outperformance. In Europe, despite a weak demand outlook, CIE aims to sustain its margins at the “new normal” of demand. The current geopolitical conflict has not had a material impact on the company’s business yet, though it may lead to supply disruptions if it continues for a couple more weeks. Despite increasing input costs, management is confident of maintaining margins in India business as CIE continues to work on improving efficiencies. The stock trades at 19.3x/17.7x CY26E/CY27E consolidated EPS. Reiterate BUY with a TP of INR546 (~21x CY27E consolidated EPS).

India business to remain the key growth driver

Auto demand has picked up across segments after GST rate cuts and continues to hold strong even in 1QCY26, as per management. Order schedules for 2Q also remain healthy. Further, CIE is expected to start SOP of multiple new orders (iron castings, forgings, stampings) in the coming quarters, which would further boost revenue. CIE has been seeing an uptrend in its growth trajectory over the last few quarters, and management expects this trend to continue in 1Q as well. The ongoing geopolitical conflict is likely to result in supply-side disruptions if it persists for a couple of more weeks. Further, despite rising input costs, management remains confident of maintaining its India business margins.

Europe: Management to focus on margins

The demand outlook for light vehicles in Europe continues to be weak. Further, CIE has a strong EV order book, though the underperformance of European EV OEMs amid Chinese competition has led to muted ramp-up for CIE. Given weak demand, CIE is “right-sizing” its European operations and has already restructured Metalcastello, which has now returned to ~18% margins at reduced demand, and it is now making similar efforts at Legazpi (last phase likely in CY26). Overall, CIE remains focused on sustaining its performance given reduced demand.

Valuation and view

For CIE India, its India business is likely to be a key growth driver given the pickup in demand across segments. Further, on the back of its new order wins, we expect India business to resume its outperformance to industry growth, which was lacking in the recent past. In Europe, it would continue to focus on maintaining margins despite reduced demand. At CMP, the stock trades at 19.3x/17.7x CY26E/CY27E consolidated EPS. Reiterate BUY with a TP of INR546 (~21x CY27E consolidated EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041