Buy Cholamandalam Inv & Fin Ltd for the Target Rs.1,870 by Motilal Oswal Financial Services Ltd

* Cholamandalam Investment and Finance (CIFC) appears to be emerging from a cyclical slowdown, with a recovery in growth momentum and early signs of asset quality improvement. The company is expected to report strong, broad-based disbursement growth across its key product segments, supported by robust demand across CVs, PVs, and two-wheelers in both new and used categories. The GST rate reduction aided affordability by lowering vehicle prices, thereby strengthening demand conditions and improving conversion rates across segments.

* Over the past 12-18 months, CIFC faced sustained asset quality pressures, with GNPA deteriorating sequentially, driven by elevated delinquencies in the vehicle finance portfolio and higher slippages in the CSEL segment; however, early signs of improvement are now visible, aided by improving collection efficiencies in VF and moderation in credit costs, led by the exit from the partnership-sourced CSEL business.

* We expect asset quality to improve further in 4Q and in FY27, supported partly by favorable seasonality and strengthening borrower cash flows, aided by a healthy monsoon, a robust kharif harvest, and improving vehicle capacity utilization. This should translate into a gradual moderation in credit costs over the coming quarters. We model credit costs (as a % of avg. AUM) of 1.65%/1.5% in FY27/FY28E (vs. ~1.75% in FY26E).

* CIFC’s NIM has begun to expand over the past couple of quarters, with the company guiding a further 5-10bp dip in cost of funds, which is likely to flow through to the NIM, implying ~10bp of incremental margin expansion in 4Q. We expect margins to improve in 4QFY26, driven by lower funding costs, and thereafter remain broadly stable over the medium term. Its NIM is estimated at ~7% for both FY27/FY28E.

* The company’s newer business verticals, including CD and gold loans, are scaling up well, with the gold loans network expanding to 118 branches and AUM reaching ~INR10b as of Dec’25. Additionally, the CSEL segment is witnessing a gradual recovery following a phase of stress and portfolio recalibration, with monthly disbursements reaching ~INR10b in Dec’25.

* While a temporary ceasefire between the US/Israel and Iran has been announced, the situation remains fluid and fragile, with risks of re-escalation persisting. Accordingly, we expect continued volatility in stock performance, with news flow around the evolving geopolitical situation likely to act as a key near-term trigger. This will impact both growth outlook and asset quality trajectory for the company.

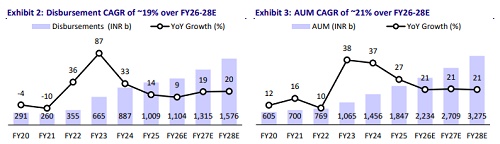

* CIFC continues to demonstrate resilience through its diversified business model, prudent risk management, and focus on sustainable growth, even as it navigates a dynamic operating environment. We expect ~21% AUM CAGR and ~26% PAT CAGR over FY26-28, alongside a projected RoA/RoE of 2.7%/20.0% in FY28. We reiterate our BUY rating on the stock with a TP of INR1,870 (based on 3.6x Mar’28E BVPS).

AUM growth accelerates; strong momentum in VF disbursements

* Over the past 3-4 quarters, the company’s disbursement trajectory remained largely flat, impacted by subdued demand in vehicle finance and asset quality-related headwinds across select segments. However, disbursement momentum has picked up from 3QFY26 onwards, supported by GST rate cuts. We expect this improvement to be sustained in 4QFY26 and FY27.

* CIFC is increasingly focusing on scaling its consumer durable (CD), gold loan, and in-house digital lending businesses, with management guiding for a visible improvement in AUM and disbursement growth from these segments by 4QFY26. We believe the ramp-up of these businesses will support overall growth momentum while also aiding margin expansion, given their relatively higher-yield profile.

* Additionally, the retail mortgage portfolio, including LAP, home loans, and SBPL, has also delivered strong disbursement growth, supported by sustained housing demand and healthy SME credit traction. Hence, we expect an AUM growth of ~21% in the coming quarter and model an AUM CAGR of ~21% over FY26-28.

NIM tailwinds largely behind; marginal ~5-10bp upside in 4Q

* NIMs have begun to expand over the past 2-3 quarters with ~45bp of improvement already realized. The company is guiding for a further 5-10bp decline in cost of funds, which is expected to largely transmit to NIMs, implying an incremental ~10bp of margin expansion in 4QFY26.

* While benefits from lower EBLR-linked borrowings will continue to support a decline in cost of funds, the extent of further reduction is likely to be limited due to recent hardening in bond yields (up ~35bp for AA+ NBFCs) and limited incremental pass-through by banks on MCLR-linked borrowings, leading to higher incremental funding costs.

* We expect margins to improve in 4Q, driven by lower funding costs, and thereafter remain broadly stable over the medium term, with NIM estimated at ~7% for both FY27/FY28.

Tight cost control and operational efficiency driving stable opex

* CIFC has maintained strict control over its operating expenses, demonstrating a strong focus on efficiency and cost management. It continues to leverage digital initiatives and process optimizations to enhance operational efficiency, helping offset inflationary pressures and support sustainable profitability.

* Despite continued investments in branch expansions of its gold loan business and scaling up the consumer durable business (both opex-intensive), cost ratios are expected to remain broadly stable, supported by improving productivity and operating efficiencies, driving operating leverage. We expect the opex-to-average asset ratio to be sustained at ~3.1%/3.0% over FY27/FY28.

Early signs of asset quality normalization; expect moderation in credit costs

* Asset quality trends in the vehicle finance segment are exhibiting early signs of recovery, with Stage 2 assets declining from ~3.9% to ~3.6% (~30bp improvement). Further, early delinquencies and non-starters have moderated, indicating improved collection efficiency and a positive shift in portfolio behavior.

* The stress witnessed over the past two years was largely driven by external factors such as weak monsoons and subdued capacity utilization, particularly in the SCV, LCV, and tractor segments. However, we believe that, with a recovery in demand following GST rate cuts and improving utilization levels, disbursement momentum has strengthened, which is expected to support a gradual improvement in credit performance.

* In the CSEL segment, asset quality is gradually improving following a series of corrective actions. NCL trends have begun to moderate, declining from 7% in 2Q to ~6.4% in 3Q, with management guiding for a reduction to below 5% over the next financial year.

* We expect these improving trends across vehicle finance and CSEL to drive a gradual normalization in asset quality, leading to moderation in credit costs from 4QFY26 onwards and into FY27. Accordingly, we model credit costs (as a % of avg. AUM) of 1.65%/1.5% in FY27/FY28E (vs. ~1.75% in FY26E).

Valuation and view

* CIFC is gradually evolving into a more robust and resilient NBFC—one that is less cyclical, more diversified, and increasingly anchored in stable, secured retail and SME income streams. The company’s measured approach of curbing exposure to riskier product lines, while simultaneously expanding newer businesses such as CD and gold loans, underscores its commitment to preserving earnings quality and retaining balance sheet strength amid a weak macro environment.

* The company is navigating a complex operating environment by reinforcing its core businesses and implementing corrective measures in the underperforming segments. We expect near-term stock performance to remain volatile, driven by elevated geopolitical uncertainty. Any persistence or escalation of tensions between the US/Israel and Iran could act as a key downside risk, potentially impacting the macro environment and weighing on growth as well as asset quality trends.

* CIFC trades at 3.6x FY27E P/BV, a premium that we believe is well-deserved and likely to sustain. This reflects the company’s consistent focus on navigating vehicle demand cyclicality while sustaining healthy AUM growth and stable asset quality through a well-diversified product mix. We expect CIFC to deliver a PAT CAGR of ~26% over FY26-28, with an RoA/RoE of 2.6%/20% by FY28. We reiterate our BUY rating with a TP of INR1,870 (based on 3.6x Mar’28E BVPS)

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041