Buy Tech Mahindra Ltd for Target Rs.1,925 by Choice Institutional Equities

Focus on Scaling up Top Accounts

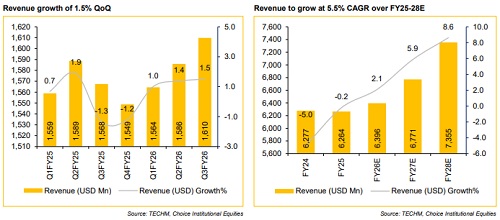

View & Valuation: TECHM is positioning itself as a future-ready partner by embedding AI across its entire service portfolio. We believe, the company is gaining market share in the Communication vertical supported by its differentiated offerings and strong vendor-consolidation opportunities. With increased clarity post the company’s outlook on industry-leading growth, as well as continuity in margin expansion led by project Fortius, gives us confidence to revise our estimate upwards. Thus, we expect Revenue/EBIT/PAT to expand at a CAGR of 8.8%/27.5%/22.1%, respectively, over FY25–FY28E. We have revised our P/E multiple to 24.0x (from 22.0x), resulting in an upward revision of our target price to INR 1,925 from INR 1,730, while maintaining our BUY rating.

Q3FY26 Revenue and EBIT in Line; PAT misses Estimate on one-offs

* Reported Revenue for Q3FY26 stood at USD 1,610 Mn up 1.5% QoQ (vs CIE est. at USD 1,608 Mn). The CC growth was 1.7% QoQ & and 1.3% YoY. In INR terms, revenue stood at INR 143.9 Bn, up 2.8% QoQ and 8.3% YoY.

* EBIT for Q3FY26 came in at INR 18.9 Bn, up 12.0% QoQ (vs CIE est. at INR 18.1 Bn). EBIT margin was up 107 bps QoQ to 13.1% (vs CIE est. at 12.2%).

* PAT for Q3FY26 came in at INR 11.2 Bn, down 6.1% QoQ on back of one-off labour code impact (vs CIE est. at INR 12.5Bn).

New Deal Wins Remain Strong; Focus on Strengthening Strategic Accounts

TECHM reported Q3FY26 revenue of USD 1,610 Mn, up 1.7% QoQ in CC. The company posted record quarterly deal bookings of USD 1,096 mn, up 34.3% QoQ and the highest LTM deal wins in five years, well above its USD 600–800 Mn target range. Deal momentum remains strong and well distributed across verticals. Vertical performance was mixed, with Communications (+2.8% QoQ), Manufacturing (+2.2%), and Technology and Healthcare (+3.0% each) showing growth, while BFSI declined 6.2% QoQ. Revenue from USD 20 Mn+ clients continues to outpace the company average, driven by a focus on scaling up strategic accounts and long-term partnerships. Management remains confident of sustaining deal momentum, emphasizing on efforts to convert large deals and expand the number of clients in the USD 20 Mn+ category.

15% EBIT Margin Target for FY27 Remains Intact

TECHM reported its ninth consecutive quarter of margin expansion, with EBIT margin rising 108 bps QoQ to 13.1% in Q3FY26. The improvement was driven by a 20–30 bps contribution from volume growth, with the balance largely led by Project Fortius initiatives, including a higher share of fixed-price projects, pricing actions, and utilisation improvement. The management remains confident of achieving its FY27 EBIT margin target of 15%, supported mainly by gross margin expansion. Employee headcount stood at 149,616 as of Q3FY26, reflecting net employee reduction of 3,098 on QoQ basis. Voluntary LTM attrition declined to 12.3% from 12.8% in Q2FY26.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

.jpg)