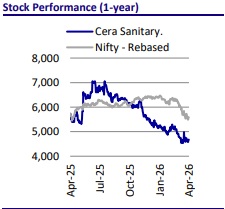

Buy Cera Sanitaryware Ltd for the Target Rs.5,990 by Motilal Oswal Financial Services Ltd

Healthy demand momentum continues in 4QFY26

Cera Sanitaryware (CRS) continued to witness healthy demand momentum in 4QFY26 after clocking a healthy 11% revenue growth in 3Q, following a <5% growth since 2HFY24. In our recent interaction, management remained optimistic about reporting double-digit growth in FY27, with a gradual expansion in margins as one-off cost factors disappear in the coming period. Further, the company’s production remains unaffected, supported by sufficient gas supply from Gail (100%) and Sabarmati (80%). We keep our earnings estimate intact and expect an 11%/23%/20% CAGR in revenue/EBITDA/PAT over FY26E-28, with EBITDA margin recovering toward 16%. A high cash surplus (~INR10b likely in FY28) will help CRS to weather the storm in case of tough times. After a ~15% correction in scrip from its Feb’26 high, CRS’s scrip appears attractive at ~19x FY28E P/E (vs. 33x 10-year average). We, thus, upgrade our rating on CRS to BUY with a revised TP of INR5,990, based on 25x FY28E P/E.

Key highlights from our interaction with the management

* Demand momentum remained healthy, and a double-digit revenue growth is likely in 4QFY26, in line with management guidance.

* Management also expects double-digit revenue growth in FY27.

* Margins have seen contraction in the last few quarters due to factors such as: 1) a rise in trade discount due to a greater mix of project sales; 2) a rise in brass prices; 3) higher publicity costs associated with phasing out certain SKUs; and 4) new brand launch-related expenses.

* Management expects a gradual recovery in margins (13-14% in 4QFY26 and 15%+ from 2HFY27 onwards) as some one-off costs disappear.

* The company’s production has remained unaffected, supported by sufficient gas supply from Gail (100%) and Sabarmati (80%), compared to a more than 50% cut in gas supply for Morbi-based players, which has led to the shutdown of most plants in the region.

* CRS has taken two price hikes in Mar'26 of 4% in Sanitaryware and 11% in Faucetware, following raw material cost inflation, to protect margins.

* Faucetware plant utilization is near optimal level, while Sanitaryware plant is operating at ~80%. Faucetware capacity can be scaled up from 0.4m units to 0.6m units in 4-6 months at existing location, as needed.

* The company has acquired a land parcel near Kadi, Gujarat, for a Sanitaryware greenfield facility. It will decide on the timeline to set up capacity in the next few months.

* The Polipluz brand is focused on driving volumes through store expansion.

* The Senator brand aims to elevate CRS’ positioning in the premium segment, rather than solely driving volume.

* The company is in the process of appointing brand ambassadors soon.

India’s top sanitary and bathware brand

Founded in 1980, CRS is India’s third-largest sanitaryware player and a leading faucet brand in the bathware industry with ~8% combined organized market share. It has an annual capacity of 2.5m pieces of sanitaryware and 4m pieces of faucetware, largely comprising products in the mid-premium range. Its manufacturing plants are based in Kadi (Gujarat), the ceramic hub of India. Building on its earlier asset-light model, the company has ramped up capex over the last 2 - 3 years to develop in - house capacity for midpremium range products, while continuing to outsource mass-mid-range product requirements. CRS’s three brands (Senator, CERA Luxe, and CERA) cater to its products at different price points. The company has a highly penetrated distribution network with 6,600+ dealer partners, 25,500+ retailers, 1,850 brand stores, and 13 company-owned experience centers. Rising aspirations and the affordability of consumers are driving premiumization in tier 2/3 towns (over 70% revenue exposure), despite the company increasing its presence in the niche premium category. CRS has adopted a risk-averse business model thus far, with retail sales contributing ~80% to total revenue. However, looking at the robust prospects, it now intends to increase its focus on institutional sales as well, with a dedicated sales team in place.

Wide product offerings; premiumization-driven growth

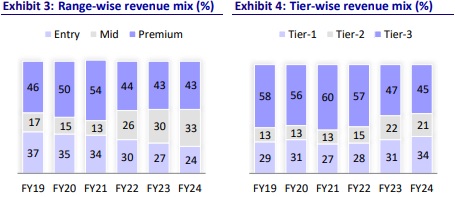

CRS has vast product offerings throughout the value chain (mass to luxury), which are sold through its three brands (Senator, CERA Luxe, and CERA), pan-India, through a multilayer marketing infrastructure as well as through continued brand efforts. Starting with sanitaryware over four decades ago, CRS now has a wide product basket (added faucets in FY11 and tiles in FY13). Regular introduction of new SKUs, refreshing running SKUs, and entry into new product lines have helped the company expand its portfolio. While gaining strength in the mass-mid segment through its CERA and the newly launched Polipluz brands, the company has also been focusing on the premium segment through its Senator and CERA Luxe brands. The premiumization trend in tier 2/3 towns (CRS’ focus) has also led the company to address the changing requirements of these markets. The mid and premium segments combined generated over 75% of total revenue in FY25. Following a 6% revenue CAGR over FY19 - 25, we estimate a 9% revenue CAGR over FY25-28. CRS is tracking industry growth in the sanitaryware and faucetware categories, as it will continue to expand its channel and product basket with heightened branding efforts.

Diversification in faucetware working well

CRS enjoys a wide product basket in the bathware category. The company added faucets in FY11 and tiles in FY13. In FY25, non-sanitaryware products accounted for 51% share of the total revenue, a substantial diversification from a single product line. Notably, all these diversifications were achieved without CRS leveraging its balance sheet. Over these years, faucetware has scaled up rapidly (15% revenue CAGR over FY19 -25; ~INR7.5b revenue in FY25, 39% mix in total), delivering the best margins within the pack. Traction in tiles (~INR1.9b revenue in FY25, 10% mix), though, has been slow due to low brand salience and intense competition; CRS's focus remains on the high-end GVT segment to profitably grow the division. Wellness is a niche segment (comprising bathroom cubicles/partitions/shower panels) and may face limitations in scaling. Faucetware capacity was expanded from 0.3m pieces per month in FY23 to 0.4m pieces in FY25. Sanitaryware capex will be executed in due course. Additional capacities at new locations would also mitigate the risk of production disruption at a single location.

Healthy cash flow due to a strict credit policy

CRS’s strong cash flows (OCF/EBITDA ~75%, FCF/PAT ~109% average over FY19-25) have been driven by its strict credit policy, healthy margins, and asset - light business model. However, these metrics weakened in FY25 due to an increase in the working capital cycle. Management expects them to normalize in FY26. Leveraging an asset-light model, the company has rapidly widened its product offerings. It has also paid regular dividends over the last 30+ years (30%+ payout ratio in the last three years). We expect CRS to generate ~INR6b of FCF over FY25 - 28. We also project the company to generate over INR10b cash in FY28 (~INR6b in FY25).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)