Buy AU Small Finance Bank Ltd for the Target Rs. 1,275 by Motilal Oswal Financial Services Ltd

Business momentum robust; well poised for RoA expansion

NIM expands 24bp QoQ

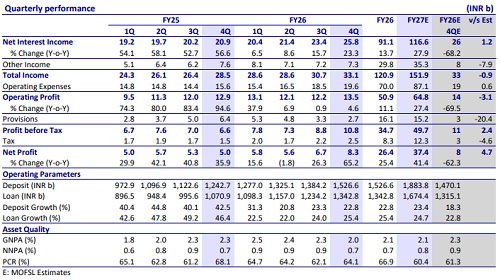

* AU Small Finance Bank (AUBANK) delivered a healthy performance in 4QFY26, characterized by a healthy uptick in NIM, as well as lower-thanexpected provisions. Business growth was robust at 24% YoY/9.6% QoQ.

* AUBANK’s 4QFY26 PAT stood at INR8.3b, up 65% YoY (5% beat), led by healthy NII and a sharp decline in provisions.

* NII came in at INR25.8b, up 23% YoY (in line). NIMs expanded 24p QoQ to 5.96%. The bank sustained industry-leading growth at 25% YoY/9% QoQ.

* Asset quality improved, with slippages declining 17% QoQ. GNPA/NNPA ratios declined to 2.03%/0.74% (down 27bp/14bp QoQ). PCR improved to 64% from 62% in 3QFY26.

* Credit costs declined to 0.6% (0.96% for FY26). Provisions were lower at INR2.7b (20% below our est., down 19% QoQ).

* We fine-tune our earnings and estimate a PAT CAGR of 35% over FY27- 28E. AUBANK remains our top pick among mid-size private banks. Reiterate BUY with a TP of INR1,275 (premised on 3.4x Sep’27E BV).

Robust growth outlook; FY27E credit costs guided at 0.9%

* AUBANK’s 4QFY26 PAT grew by 65% YoY/25% QoQ (5% beat), aided by lower-than-expected provisions and healthy NII growth.

* NII grew 23.3% YoY/10.3% QoQ to INR25.8b (in line), as NIM expanded 24bp QoQ to 5.96%. This growth was led by CoF reduction, lower day count, and lower interest reversals.

* Provisions were lower at INR2.7b (20% lower than MOFSLe), while the quarterly credit cost ratio dipped to 15bp from 19bp in 3Q. PCR improved to 64.1% from 62.1% in 3QFY26.

* Other income was lower at INR7.3b (8% lower vs. MOFSLe; up 1% QoQ), as the bank reported a minor treasury loss in 4Q. Opex grew 26% YoY/6% QoQ to INR19.6b (in line). The C/I ratio thus dipped to 59.2% (down 114bp QoQ).

* Advances grew 25.4% YoY/ 8.8% QoQ, led by commercial banking (29% YoY/ 11.6% QoQ), and Retail secured (up 21% YoY/ 5.7% QoQ). The unsecured business grew 7% QoQ, fueled by MFI.

* Bank guides for 2.2-2.5x nominal GDP growth, translating to 22-25% growth in FY27E, aided by favorable macro and strong execution.

* Deposit growth was strong at 22.8% YoY/10.3% QoQ, while the CASA book grew 19.6% YoY/8.6% QoQ. As a result, the CASA ratio stood at 28%. The CD ratio declined to 88% from 89.2% in 3Q.

* Slippages declined 17% QoQ to INR6.6b in 4Q, aided by improved asset quality across segments. GNPA/NNPA ratios declined to 2.03%/0.74%. The bank reported a lower credit cost of 15p (FY26 credit cost at 96bp) and has stated FY27E full-year guidance at 0.9%

Highlights from the management commentary

* AUBANK’s 4Q is typically a seasonal quarter and better for credit costs. The bank targets credit costs of ~90bp for FY27E.

* The 1.8% RoA reported in 4QFY26 is partly seasonal. The bank aims to sustain ~1.8% RoA in FY27E. The key levers include improvement in the opex-to-assets ratio and moderation in credit costs, which are expected to be lower on a fullyear basis.

* CoF has likely bottomed out, with repricing offset by recent increases in deposit rates. ? Overall, the bank continues to target sustainable growth of ~2.0-2.5x India’s GDP growth.

Valuation and view

* AUBANK delivered a strong quarter, supported by robust growth, 24bp QoQ NIM expansion, and a sharp decline in credit costs. Margin expansion was driven by lower cost of funds, an improved asset mix, favorable day-count impact, lower interest reversals, and partial benefit from tax reversals. Growth continues to remain among the best in the industry, supported by a highyielding asset mix and strong momentum. We remain constructive on the bank’s underlying growth trajectory. Operating expenses are expected to moderate, leading to a decline in the C/I ratio towards ~56-57% over FY27-28E.

* Asset quality trends remain encouraging, with stress levels easing and a recovery visible in the unsecured portfolio. With NIM expansion, normalization in credit costs, and sustained business growth, we expect AUBANK to deliver best-in-class earnings growth in the medium term. We broadly retain our earnings estimates and expect a PAT CAGR of 35% over FY27-28. AUBANK remains our top pick among mid-size private banks. Reiterate BUY with a TP of INR1,275 (based on 3.4x Sep’27E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412