2025-09-15 02:07:06 pm | Source: Choice Broking Ltd

Buy Ashok Leyland Ltd For Target Rs. 155 By Choice Broking Ltd

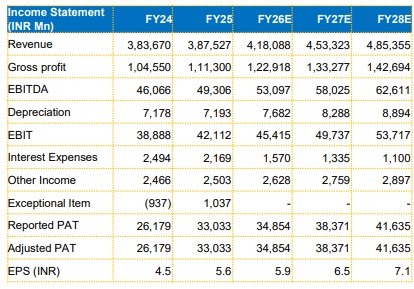

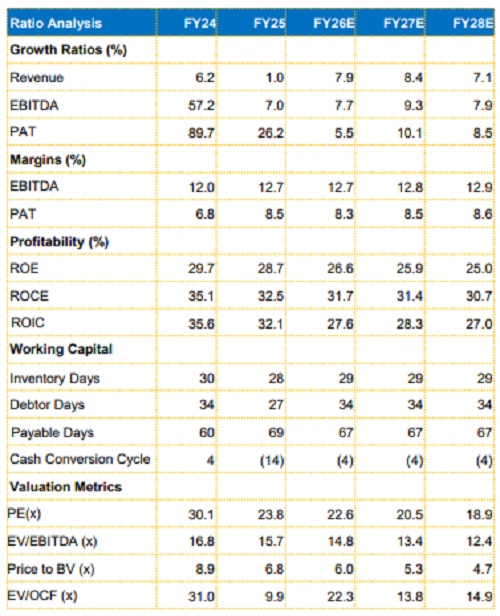

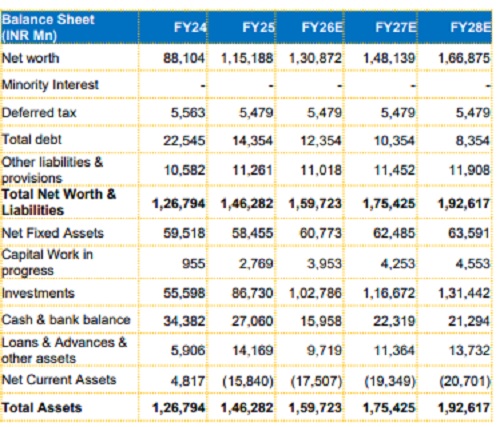

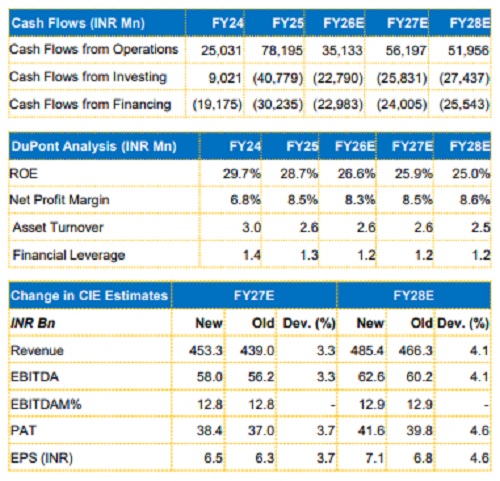

View and Valuation:

AL is well-positioned to take advantage of the GST rate cuts for the CV industry (~93–95% of total revenue) which can act as a catalyst for the pent-up replacement demand of the aging fleet. Taking this into account, we revise our FY27/FY28 EPS estimates upwards by 3.7%/4.6%. We value the core business at 20x (maintained) on the average FY27/28E EPS and arrive at a value of INR 136. We assign a value of INR 15 to HLFL and INR 4 to Switch Mobility, leading to a revised target price of INR 155. We maintain our BUY rating on the stock.

Financials:

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 00016013

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Quote on Markets by Mr Avinash Agarwal, Senior Vice ...

Uttar Pradesh continues to play a pivotal role in th...

Research report on Manthan- Oil & gas by Swarnendu B...

Market Round-up - 11th August 2026 by Motilal Oswal ...

India's Q1 FY27 GDP growth likely to near 8 pc amid ...

Buy Dalmia Bharat Ltd For Target Rs. 2,278 By Geojit...

Evening Roundup : Daily Evening Report on Bullion, B...

NASA invites ISRO to join Moon Base Programme as Ind...

Buy Suzlon Energy Ltd For Target Rs.56 By Geojit Fin...

India's merchandise exports touched record high at $...