Buy Apollo Tyres Ltd for the Target Rs. 551 by Motilal Oswal Financial Services Ltd

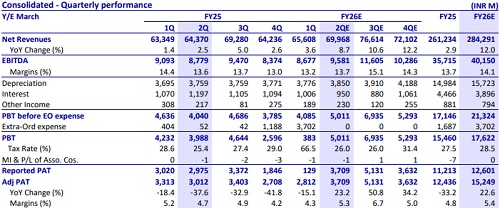

* While demand was healthy in Jul, it turned weak in Aug and then there were purchase delays in Sep in replacement given the GST deadline. OE demand was stable. We expect standalone revenue growth of 6% YoY (flat QoQ).

* Input costs are down about 2% QoQ, which is likely to aid margins. However, INR depreciation towards 2Q end may offset some of these gains.

* We expect India margins to improve 30bp QoQ (+180bp YoY over low base) due to lower input costs.

* Demand in Europe, although weak, is likely to be stable QoQ.

* We expect Europe margins to improve 70bp QoQ (-330bp YoY) to 11.5%.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Neutral Muthoot Finance Ltd for the Target Rs. 3,100 by Motilal Oswal Financial Services Ltd