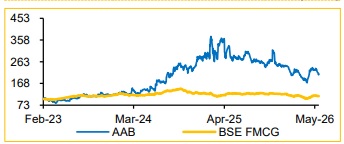

Buy AAB Ltd for the Target Rs.1,070 by Choice Institutional Equities

Kerala Market Gains Traction, IMFL Proprietary Volume Grows by 39% YoY

Incremental market share gains (+1.5% in FY26) have boosted growth for proprietary brands across categories such as whiskey and brandy. AAB reported a growth of 33% in IMFL Proprietary segment for FY26. However, overall topline declined by ~5% because of transition of contracted manufacturing from full accounting to revenue-only accounting. Further, oversupply of ethanol led to lower offtake, causing a decline in ethanol volume by ~17% for FY26. Key monitorables include ramp-up in premium product launches, scaling up of proprietary brands across new markets, recovery in ethanol demand driven by policy support and margin sustenance.

View and Valuation

We reduce our FY27E revenue estimate by ~5% to factor in continued weakness in the ethanol business amid industry-wide oversupply and lower blending allocation. However, we remain constructive on AAB, supported by a strong traction in proprietary IMFL brands, RTD and single malt launches. We continue to factor in ~36% growth in the IMFL proprietary portfolio and marginally increase our EBITDA margin estimate driven by better product mix and operating efficiency. We expect a Revenue / EBITDA / PAT CAGR of 9.8% / 14.9% / 16.1% over FY26–FY29E, respectively. Thus, we maintain our ‘BUY’ rating with a revised target price of INR 1,070 (vs. 1,110) using the DCF methodology. Our TP implies a PE of 18.5x on FY28E EPS.

Q4FY26: Margin Expands, in line with CIE estimate

* AAB reported a revenue of INR 2.4 Bn, declining by 1.6% YoY / 8.4% QoQ

* The decline was caused by volume contraction in the IMFL Licensed (IMFLL) and Ethanol segment (combined ~23% of net revenue), declining by 49.7% and 33.3%, respectively

* EBIDTA margin expanded by 226 bps YoY; EBITDA stood at INR 402.9 Mn (+13.6% YoY) ? Higher taxes and interest cost led to a growth of 5.3% YoY in PAT. PAT margin saw a growth of 65 bps YoY, reaching 9.9% (vs CIE Est. of 9.7%)

‘KULTUR’ Ready-To-Drink and Single Malt Whiskey to Propel Growth

AAB continues to strengthen its premiumisation strategy through focus on proprietary IMFL brands, supported by a strong traction in the Central Province portfolio, premium offering, such as Hillfort and Nicobar. RTD has been softlaunched in MP; the drink is expected to be available across other markets in 1–2 months, pending label registrations. Further, commissioning of the 6,000 KLPD malt facility and planned launch of its own single malt over the next 18 months is expect to support both, premium brand expansion and backward integration. Capacity enhancement in ENA and acquisition of SDF Industries will strengthen bottling capability and expansion into new states, such as Odisha, Andhra Pradesh and Karnataka. This will support profitable growth in the medium term.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

2.jpg)

.jpg)