Auto & Auto Ancillaries Sector Update :Demand returning across NA, EU; Indian players best placed by Emkay Global Financial Services Ltd

As part of our 2-day Auto Virtual Conference, India: Building for the World, we hosted the managements of prominent Indian auto ancillaries (MM Forgings, GNA Axles, Nelcast, Uniparts, Emmforce Autotech, Kirloskar Ferrous) operating in the castings and forgings space and catering to the domestic and export markets across vehicles categories (mainly CVs and agri/off-highway). KTAs: 1) After a prolonged downturn over the past 2-3Y in the CV (Class 6-8 trucks) and Agri/Off-highway space, major export markets of North America and Europe are now seeing demand recovery (aided by an ageing fleet, improving freight conditions, EPA norm change-led pre-buy in NA). 2) After 3-4Y of weakness in domestic MHCVs, signs of a multi-year upcycle are clearly visible; tractors too are performing well on supportive macros. 3) During this downturn, Indian players invested in expanding capacity, building capabilities, and strong cost optimization, thereby positioning themselves to capitalize on this demand upturn. 4) India is fast becoming the preferred global sourcing hub, owing to an inherent low cost structure (in NA, Indian players offer 20% cost benefit despite tariffs). To capture this opportunity, we favor our coverage stocks BHFC (BUY; TP: Rs2,000), Craftsman Automation (BUY; TPRs9,800), TMCV (BUY; TP Rs650), Shriram Pistons (BUY; TP Rs4,650), and JK Tyre (BUY; TP Rs650)

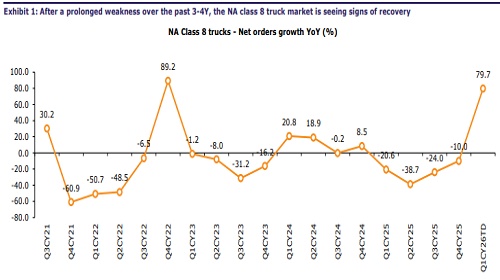

Recovery is now underway across exports markets in the CV, Off-highway space NA Class 6–8 demand is seeing the start of a replacement-led recovery after a prolonged downturn, driven by improving freight conditions, ageing installed base, and better visibility on EPA norm change (wef Jan-27)-related cost inflation (5-7% rise anticipated). Per companies’ management commentary, signs of a pre-buy are visible due to improved regulatory clarity and higher expected truck prices; demand is expected to stay strong through CY26 and into H1CY27. In EU, the heavy-truck market is showing early signs of a replacement-led recovery (25-30% growth expected in the next 2-3Y) aided by ageing fleets and under-replacement in the past few years. In the off-highway/agri space, conditions are turning favorable with decline in the NA Large AG segment narrowing (CY26: 15-20% vs 30% in CY25), EU Large AG segment seeing flat-to-modest growth

Domestic demand also remains robust, aided by recent GST cuts After 3-4Y of weakness in the domestic MHCV industry, signs of a multi-year upcycle are clearly visible. The demand momentum remains robust (aided by recent GST cuts) and the outlook for FY27 is also positive. The domestic tractor industry is faring well, aided by favorable monsoons, healthy reservoir levels, GST cut, and firm farmer sentiment.

Structural tailwinds in place for Indian manufacturers India is fast becoming a favored global sourcing hub. Per companies’ mgmt commentary, step-up in closure of EU foundries on labor shortage, rising energy cost, worsening financial stress is creating opportunity for Indian suppliers offering huge benefits on the inherent low manufacturing cost. The trend is intensifying, as EU OEMs are aggressively seeking alternative sourcing options. In NA, Indian players offer 20-30% benefit despite tariff headwinds; this helps gain share with existing clients, catering to new clients.

Players structurally well positioned to capitalize on this demand upturn While the end-market has seen prolonged weakness over the past 2-3Y, Indian ancillary players have made strategic and calibrated investments in expanding capacity, building capabilities, widening the range of their product offerings, and bringing about strong cost optimizations in operations (including via investments in renewable energy, to reduce power cost). A prime example is MM Forgings who invested Rs10bn over the last 5Y in building capacities and extensive machining capabilities.

Our view: BHFC, CAL, TMCV, SPRL, JKI best placed in this demand upturn Under our coverage, we think BHFC, CAL, TMCV, SPRL, and JKI are best placed to draw on the opportunity. BHFC’s outlook is turning positive; it will benefit from a strong India CV outlook, NA CVs bottoming out. CAL’s investments in ICE are paying off as it is seeing increased traction in PT amid supplier consolidation; it is on track to achieve USD100mnpa guidance from large engine castings. We think TMCV will lead this multiyear domestic CV upcycle (A turning CV cycle; TMCV to lead), with Iveco offering an optionality (we factor in 50% probability weighted valuation for Iveco). We like SPRL (Growth firing across verticals; valuation comfort high) owing to its dominance in core segments, transition into a multi-product player via diversification into non-ICE. JKI (Growth accelerating; margins sustained; valuation attractive) too will benefit, given the 58% contribution from TBR to India revenue.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...