Auto & Auto Ancillaries Sector Update : Delhi EV Policy 2.0 – A major step to accelerate electrification by Emkay Global Financial Services Ltd

The Delhi cabinet yesterday approved the Delhi EV Policy 2.0 (link), to promote adoption of clean mobility through targeted incentives, infrastructure development, and strong regulatory measures. The policy focuses on complete transition to EVs in E-3Ws and E-2Ws from Jan-27/Apr-28 with a staggered transition across other categories. Akin to the earlier subsidies, the government has offered a purchase incentive for E-2Ws (ex-factory cost

Only E-3Ws/E-2W registrations permitted from Jan-27/Apr-28 in NCT of Delhi

Only E-3Ws (L5 category) will be permitted for new registrations from Jan-27, and only E-2Ws from Apr-28 in the NCT of Delhi. School bus fleets (whether leased or hired) are required to achieve 30% EV penetration by FY30 in the NCT of Delhi. All government fleet vehicles (buses and N1 trucks) in the NCT of Delhi that are hired or leased must be EVs from the date the policy is notified, except for emergency/specifically exempted vehicles. Fleet operators will not be allowed to add any new petrol/diesel vehicles including LCVs, LGVs (>= 3.5tn) and 2Ws to their existing fleets from Jan-26 onward; fleet operators would be allowed to add BS-VI-compliant 2Ws to their fleets until the end of Dec-26

Staggered purchase incentive structure akin to earlier policies

The policy lays out a phased, 3Y purchase incentive structure across vehicle categories. E-2Ws (ex-factory cost

Road tax and registrations fees to be waived to further incentivize EV purchases

All electric passenger vehicles (E-PVs) with an ex-showroom price up to Rs3mn will receive a 100% exemption from road tax and registration fees until FY30. However, EPVs with an ex-showroom price exceeding Rs3mn will not be eligible for any exemption. Strong hybrid EVs to receive a 50% exemption from road tax/registration fees until FY30.

Our View: Positive for pure play EV OEMs – Ather/Ola; Negative for incumbents

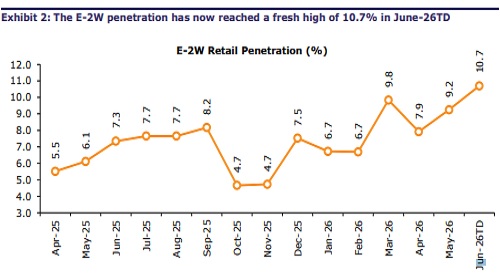

i) Industry: We believe that this development could accelerate electrification as a theme (EV share at a fresh high across 2Ws, 3Ws and PVs in Jun26TD) and also further influence customer behavior which is already witnessing a pull toward EVs. This would further accelerate scooterization (scooters form 40% of domestic 2Ws). In E-3Ws, while this could open opportunities for newer players, the market has already started consolidating in favor of larger/incumbent OEMs (BJAUT, M&M, and TVS form >75% of the E-3W market as of Q1FY27TD/FY26). We believe the EV policy could have a cascading effect into other states as well.

ii) OEMs: Ather could be one of the biggest beneficiary of this given a higher focus on expanding into non-South states supported by its upcoming EL platform (targets the Rs0.1-0.13mn price segment, the belly of the market which is ~50% of the industry volumes). Within the 2W incumbents, we believe that EIM (Royal Enfield) and HMCL are likely to be the worst affected, given a largely domestic franchise (domestic volumes: 89/94% of FY26 volumes respectively) and higher exposure to motorcycles. TVS/BJAUT, in contrast, are relatively insulated due to the significant export exposure (exports formed ~30/44% of FY26 volumes respectively) and growing E-2W franchises. While 3Ws also pose a risk, both BJAUT/TVSL are rapidly gaining market share in E-3Ws as well. Within E-PVs, M&M and TMPV are relatively better placed.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...