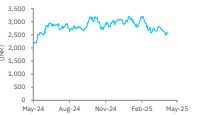

Accumulate Mahindra & Mahindra Ltd For Target Rs. 3,755 By Elara Capital

Margins impress across segments

Mahindra & Mahindra’s (MM IN) standalone EBITDA margin impressed at 14.9% (up 180bps YoY and 30bps QoQ). Automotive EBIT margin, including eSUV contract manufacturing, came in at 9.2% (ahead of our estimates of 8.9%), led by ICE EBIT margin increasing 30bps QoQ to 10%. eSUV contract manufacturing EBIT margin was 0.3%. The entire BEV operations too impressed with EBITDA margin at 1% (without PLI benefits being accounted for in Q4), while EBIT loss came in at INR 1.7bn.

Q4FY25 eSUV financials were aided by a superior mix of BEVs, with only the top end variants (pack 3) being delivered. EBIT margin for the Farm segment rose by 130bps QoQ to 19.4% in a seasonally weak quarter. The management has guided for mid-to-high teen growth in the UV portfolio in FY26 (our current estimate at 12% growth) and high single-digit growth for the tractor industry (our current estimate at 6%).

Tractor industry – Growth pegged at high single-digit for FY26: Despite a high base, MM expects the tractor industry to grow in high single-digit in FY26. On the back of resilient domestic performance, the market share stood at an all-time high of 43.3% in FY25, up 170bps YoY. While South and West continue to perform well, competitive intensity likely to rise.

Auto – Growth momentum to continue in FY26: MM expects to outperform the PV market with mid-to-high teen growth guidance for FY26, led by six-month low base for Thar Roxx, two-month low base of XUV 3XO and limited cannibalization due to the EV portfolio. Despite strong response to pack 3 BEV models, MM expects lower variants contribution to increase going forward, with at least ~25-30% of volumes from pack 1 and pack 2 variants post Q1FY26E. MM’s capacity expansion is on track, with FY25 UV exit capacity of 61.5k units expected to go up to 69k in FY26E (3k rise for XUV 3XO and Roxx) and 85k in FY27E end. In CY26, MM expects three ICE SUVs to be launched (of which two be mid cycle refreshes), and two BEVs and two LCVs to be introduced. In CY25, MM to stabilize its current portfolio.

Reiterate Buy; TP raised to INR 3,755: We are impressed by MM’s market share gains in the PV segment (FY25 Vahan retail market share up 150bps YoY to 12.3%). While growth outlook for the PV industry is muted at ~1-2%, a 15-20% growth outlook for MM’s UVs is encouraging (a similar divergence in MM’s growth versus the industry’s was seen in FY25 when MM delivered on its guidance). Continued upcycle in the Tractor industry will support valuations in the medium term. Monitor the execution of BEVs in the coming months as this is crucial for MM to meet its upcoming CAFÉ targets (of having ~20-25% of the portfolio from BEVs), as also support current valuations. We increase our FY26E-27E EBITDA estimates by 5-8%.

We reiterate Buy with higher SoTP-TP of INR 3,755 (from INR 3,654), on June 2027E as we roll forward. We value MM’s total automotive (including EVs) and farm segments at ~30x (unchanged), with a value of INR 402 ascribed to the subsidiary.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

Tag News

M&M rises on signing MoU with MoRTH