Auto Ancillaries Sector Update :EV Adoption: The resurgence by Elara Capital

The EV penetration rates in recent months have seen a resurgence. BEV penetration rates on new vehicle sales in March-May 2026 for Europe PV sales has increased to 21% (vs 18% in CY25), for China at 38% (vs 32% in CY25), India PV at 6.7% (vs 4.3% in FY26), and India 2W at 9% (vs 6.3% in FY26). The Iran war and resulting focus on oil prices and availability coupled with some of the country’s over reliance on oil imports, has resulted in this shift of consumer sentiment as also Govt’s focus again on alternate energy sources mobility (EV, hybrid, flex fuel etc). We thus believe our EV penetration forecasts for different segments in India and globally for FY30E, which were in past year undershooting our expectations, seem to be more achievable now, as we see this shift sustainable this time

History rhymes — the 1973 oil embargo as the closest structural parallel:

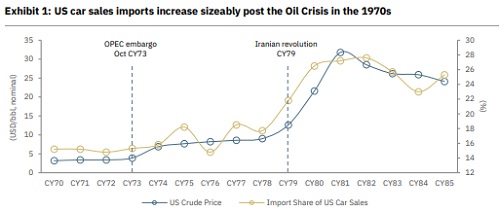

The Arab oil embargo of 1973 remains the most instructive precedent for how an energy-price shock can permanently re-order the global auto industry. During that time crude surged within months, rendering sub-15 mpg (miles per gallon) Detroit vehicles untenable; Toyota, Honda and Nissan surged from ~ 15% US import share in 1973 to ~26% by 1980 — a structural re-alignment cemented by CAFE standards introduced in 1975, which nearly doubled fleet fuel economy over the following decades. The 2025-26 Middle East crisis — Iran's blockade of the Strait of Hormuz pushing Brent higher and remaining volatile — is the most severe supply disruption since that era. The mechanism is identical to 1973; the technology that benefits this time is electric and the Chinese NEV OEMs are likely to emerge stronger, in our view. Chinese OEMs share in BEV and PHEV in Europe increased to 11.8% and 25% in YTDCY26 vs 8.7% and 8.8% in CYTD25. That said, with China’s domestic market under pressure, Chinese OEMs will further push in Europe and other regions, which is already visible in their export growth. We had highlighted reasons of Chinese NEV OEMs competitive edge in our thematic “China Energising seismic shifts”

Orderbook healthy; expect BEV penetration FY30 assumptions achievable:

OEM order books in recent calls and media reports suggest that OEMs are falling short of capacities to meet demand. Mercedes-Benz BEV order intake was up 107% year-on-year in Q1 CY26, BMW up over 60%, Indian OEMs like TMPV mentioned of increased order book to the tune of 2-2.5x. We expect BEV penetration for India PV and India 2W at 15% and 20% respectively by FY30, while for Europe, US and China EV (BEV+PHEV) is likely to be 55%, 15% and 75%, respectively.

Sona BLW, Minda corp, Uno Minda beneficiaries in Ancs; Ather, TVS Motor, M&M in OEMs:

Within the Indian Auto ancillaries space, the adoption of EV is expected to accelerate the premiumization trend.Further we prefer ancillaries, whichwould be beneficiaries of other megatrends like Lightweighting, Active safety, Connected and Electric, as highlighted in our recent thematic LACE effect. Minda Corporation remains a keyplay onpremiumization onstrong order visibility, new product expansion and strategic JV partnerships; UNO Minda's powertrainagnostic portfolio and new facility ramp-up provide a differentiated growth vector; while Sona BLW should benefit from accelerated execution of EV programs that were delayed during the earlier slowdown. SAMIL remains a SELL — ~40% Europe exposure and dependence on legacy OEMs place it most at risk from Chinese OEM share gains. In 2Ws, the EV rebound benefits Ather (NR) most, followed by TVSL (BUY) and BJAUT (Accumulate). In PVs, M&M is best placed as rising EV penetration makes CAFE compliance comfortably achievable, progressively easing the overhang on its multiple; TMPV remains a SELL as the JLR overhang continues to weigh on the consolidated multiple despite improving India EV trends.

History Repeats

1973 Oil Crisis & Rise of Japan’s Fuel-Efficient Cars:Market Re-Wired Overnight

How a supply shock rewrites the US auto industry's competitive hierarchy for a generation

The Arab Oil Embargo of 1973 was the first modern demonstration that energy shocks do not merely disrupt automobile demand temporarily — they restructure it permanently. When OPEC nations cut supply in response to US support for Israel during the Yom Kippur War, crude oil prices rose substantially (from USD 3.89/bbl to USD 6.87/bbl by 1974, and to ~USD 13.00/bbl by the second shock in 1979). The US consumer, accustomed to cheap gasoline and large-displacement Detroit vehicles delivering under 15mpg (miles per gallon), abruptly found running cost intolerable. The beneficiary were the Japanese. Toyota, Honda, and Nissan had been building compact, fuelefficient vehicles delivering 25–35mpg (miles per gallon)— but their US market share had hit a plateau, below 16% through the early 1970s. The oil shock broke the inertia. Imports share of US car sales rose from ~15% in 1973 to ~26% in 1980 and ~27% in 1981 — a structural re-alignment that took less than a decade and that Detroit has not been able to fully reverse.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...