Debt Monthly Observer by Pankaj Pathak, Quantum Mutual Fund

Follow us Now on Telegram ! Get daily 10 - 12 important updates on Business, Finance and Investment. Join our Telegram Channel

https://t.me/InvestmentGuruIndiacom

Download Telegram App before Joining the Channel

Below are Views On Debt Monthly Observer by Pankaj Pathak, Fund Manager-Fixed Income, Quantum Mutual Fund

Over the last decade, central banks have become a major participant in financial markets. They have been buying enormous amounts of government and private bonds and in some cases even equities to keep financial markets going. With the onset of COVID pandemic, their asset purchases increased many fold.

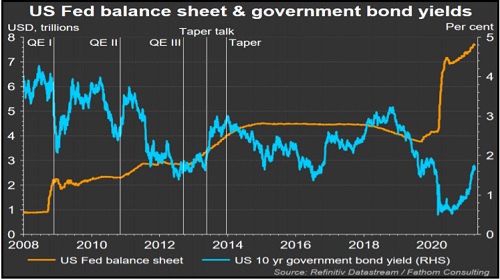

The US Federal Reserve added more assets to its balance sheet in few months after Covid than what they added in the 4 years following the great financial crisis of 2008. Other major central banks have also followed a similar trend. Global central bankers have added more than USD 10 trillion to their balance sheets.

Chart – I : US Fed Bond Purchases jumped after Covid-19

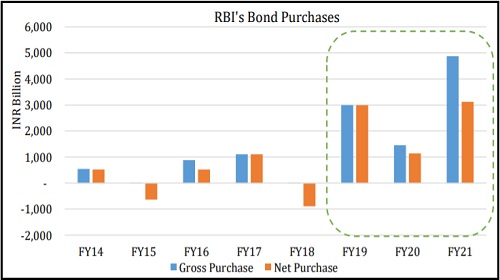

India was no different. The Reserve Bank of India (RBI) has been one of the largest buyers of government bonds in the last three years. In FY 19, it was to support the slowing economy. In 2021 it was to fight the pandemic. The RBI bought record Rs. 3.1 trillion worth of government bonds in the last financial year. They also conducted operation twists – selling short term bonds and simultaneously buying longer term bonds, to keep long term bond yields low.

Chart – II: RBI in action in bond market

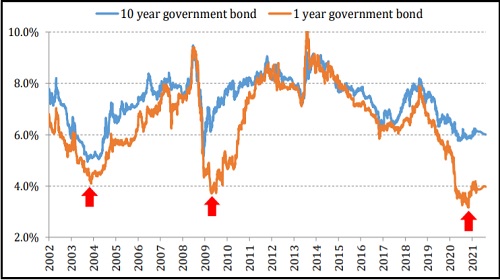

RBI’s actions dominated the market behavior in a significant way. Bond yields remained anchored throughout the year despite over 80% increase in government’s borrowing program. The 10 year government bond yield remained below 6% for most part of the last year

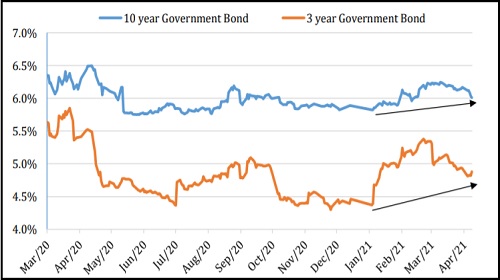

All this changed in the last 3 months. Central banks’ bond buying started to lose its efficacy. The 10 year benchmark government bond yield moved up from 5.87% on December 31, 2020 to 6.17% on March 31, 2021. Selling was more pronounced in other maturity segments both at long and the short end of the maturity curve, where yields went up by 30-50 basis points in the same period. The selling persisted notwithstanding the fact that the RBI purchased about Rs. 1.3 trillion of longer-dated government bonds through OMOs (including purchase leg of operation twists) between January and March 2021.

Chart – III : Bond yields moving higher

Source – Bloomberg, Quantum Research

Past performance may or may not sustained in future

Longer term bond funds performance suffered due to sharp rise in bond yields in the last quarter.

Table 1: Best of Bond markets behind us?

This sudden turn in investor sentiment was caused by confluence of factors. A loose fiscal policy till FY 2026, a share rise in crude oil prices and a global ‘reflation trend’ leading to rise in US 10 year bond yields. But the most significant aspect was the increasing bets on potential reversal in the monetary policy direction. There was fear that the RBI may start reducing its surplus liquidity (normalization). At the same time, many started expecting a rate hike sooner than earlier anticipated.

The RBI’s Assurance

The RBI, in its monetary policy on April 9, 2021, reiterated its commitment to keep liquidity condition easy and facilitate smooth functioning of financial markets. The governor said - “the Reserve Bank will continue to do whatever it takes to preserve financial stability and to insulate domestic financial markets from global spillovers and the consequent volatility”.

He re-iterated the importance of yield curve and appealed for a cooperative approach from markets for orderly evolution of yield curve. In Governor’s words – “orderly evolution of yield curve is a public good”.

In line with this endeavor, the RBI introduced a new bond buying plan referred as Secondary Market Gsec Acquisition Program (G-SAP). Under G-SAP 1.0, the RBI will purchase government bonds worth Rs. 1 trillion in Q1FY22 (April – June 2021).

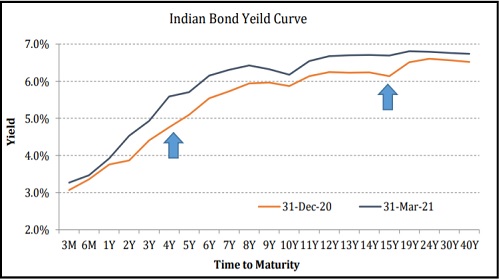

Chart – IV: Yield Curve steepened further on loose fiscal and sticky inflation

Apart from filling the demand supply gap in the government bond markets, this tool could also be used by the RBI to control the bond yield curve. Thus the bond yield curve flattened with sharp decline in long term bond yields following this announcement. The 10 year benchmark government bond yield dipped below 6.0% mark for brief period on the following day.

We do not expect any material decline in bond yields because of GSAP. In our opinion, this is just a repackaging of the conventional OMOs clubbed with an upfront commitment on quantum. Also the size of GSAP 1.0 might fail to counter the supply given the fact that the RBI purchased government bonds of around Rs. 1.5 trillion and Rs. 1.3 trillion in Q3 and Q4 of FY21. Only significant part of this announcement is that the RBI could use conventional OMOs/twists outside of G-SAP if need arise. This suggests that any sharp selloff in bond markets will be dealt with by the RBI. Thus it will put a cap on long term bond yields at least in the near term.

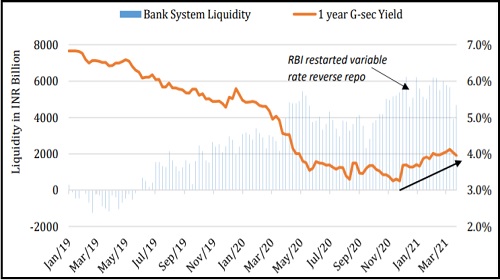

Liquidity Normalization on Track

The front end of the yield curve has been finding cues from the ongoing normalization of liquidity situation. The RBI had restarted variable rate reverse repos (VRRR) in January this year to absorb excess liquidity for slightly longer period than overnight. Until now they have been conducting VRRRs of Rs. 2 trillion for period of 14 days

The RBI has now announced to conduct VRRRs of longer maturities to absorb some more of excess liquidity. This will potentially increase the interest income on the surplus liquidity parked with the RBI by banks. Overnight and short term money market rates could go up depending on the quantum and tenor of the VRRR auctions. This could also manifest up into the front end (upto 3 year maturity) of the bond yield curve and push yields higher.

Rise in money market rates will be favorable for debt fund categories like liquid funds which rely on interest accruals from short term money market instruments.

Chart – V: Short term bond yields surged on liquidity normalization

Accommodative for now

The macro backdrop has changed significantly. One year after being battered by the lockdown, economy is recovering at a much faster pace than earlier anticipated. However, the recovery remains uneven.

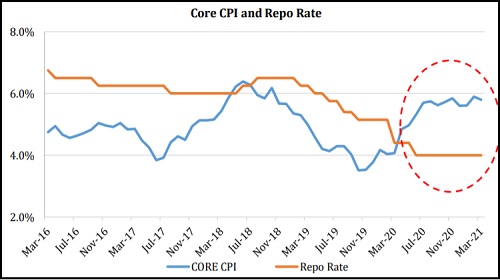

While at the same time, inflation is gathering momentum on the back of disrupted supply chains, rising commodity and fuel prices. The core inflation which excludes volatile food and fuel prices and treated as a measure for underlying inflationary pressure, has been near the RBI’s upper threshold of 6%. There is a risk of it getting generalized into inflation expectations and causing an inflation spiral. India has a troubled past with inflation. Thus it requires a careful watch and timely intervention.

This presents a critical dilemma in front of the monetary policy committee. Economic recovery is still at a nascent stage and the ongoing second wave of covid-19 has raised uncertainty. It is a difficult choice to prioritize one over the other from the growth inflation trade-off.

The monetary policy committee (MPC), in its April 2021 meeting, left the policy repo rate unchanged at 4.0% and the reverse repo rate at 3.35% and maintained its “accommodative” policy stance. Overall, the RBI maintained it priority as reviving economic growth on durable basis while they turned watchful of inflation risks on horizon.

The statement goes as - “…to continue with the accommodative stance as long as necessary to sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward”. One significant change in the policy outcome was in the nature of the forward guidance. In its monetary policy in October 2020, the RBI for the first time came up with a time based forward guidance stating they will remain accommodative…“at least during the current financial year and into the next financial year”.

It dropped this timing element from the forward guidance and made it contingent on the evolving growth and inflation trajectory. Although low interest rates are needed for the economy to revive, holding it too low for too long can have negative consequences for an emerging economy like India. Amidst resurgence of covid infections, the RBI may ignore inflationary pressures and maintain accommodative policy for some time. But, if inflationary pressures sustain, the RBI will be compelled to withdraw some of the crisis time’s measures. They have already started with the normalization of liquidity situation by the introduction of variable rate reverse repos and reversal of the cut in CRR (Cash reserve ratio- a portion of deposits that banks have to keep with the RBI as reserves).

The RBI may continue withdrawing excess liquidity though they will maintain overall liquidity in surplus. Eventually, we will see a possibility of hiking reverse repo rate towards the end of this calendar year.

Outlook – Volatility Ahead

G-SAP should bode well for long term bonds and should put a cap on yields in near term. On the other hand the excessive supply pressure will continue to push yields higher. Thus long term yields may remain range bound in near term. While short term rates are set to move higher at a pace depending on the pace of liquidity normalization.

Over medium term, inflation and potential monetary policy normalization will play more important role in shaping the interest rate trajectory. We expect market interest rates to move higher gradually over the next 1-2 years.

Portfolio Strategy and Recommendation

In the Quantum Dynamic Bond Fund (QDBF) portfolio we continue to focus on tactical trading opportunities within a narrow range. QDBF does not take any credit risks and invests only in sovereigns and top-rated PSU bonds, but it does take high-interest rate risk from time to time.

In the Quantum Liquid Fund, we continue to focus on short term treasury bills and good quality PSU debt securities. Investors should acknowledge that the best of bond market rally is now behind us. At this time it would be prudent to lower the return expectations from fixed income products– as money market yields, fixed deposits rates will remain low and potential capital gains from long bond funds will be muted.

Conservative investors should remain invested in categories like liquid fund where impact of interest rate rise would be favorable. However, while selecting a liquid fund be cautious of the credit quality and liquidity of the underlying portfolio.

At this point where fixed deposit rates have come down to historical lows, liquid funds could be better alternative in comparison to locking in long term fixed deposits. Liquid Funds invest in upto 91 day maturity debt securities which get re-priced higher when interest rates rise. Fixed deposits interest rates remain fixed for the entire tenor thus lose out during a rising interest rate cycle.

Investors with higher risk appetite and longer holding period can look at dynamic bond funds where the fund manager has flexibility to change the portfolio when market views change. These funds are best suited for long term fixed income allocation goals. However, do remember that bond funds are not fixed deposits and their returns could be highly volatile and even negative in short period of time.

Above views are of the author and not of the website kindly read disclaimer

Tag News

We anticipate immense potential benefits from the upcoming Sovereign Gold Bond Tranche in FY...