No Record Found

Latest News

Quote on Bank Nifty 28th November 2025 by Vatsal Bhu...

Quote on Gold 28th November 2025 by Jateen Trivedi, ...

India sets remarkable GDP record for world: Politica...

Quote on Rupee 28th November 2025 from Jateen Trived...

India`s coffee industry to grow at 8.9 pc to reach u...

Quote on Market Wrap 28th November 2025 from Mr. Aji...

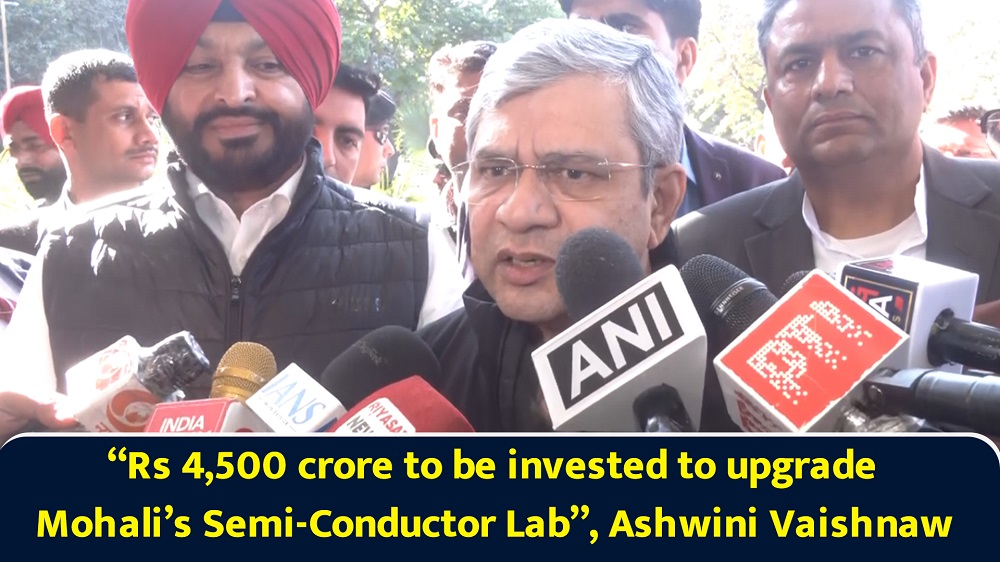

`Rs 4,500 crore to be invested to upgrade Mohali`s S...

Quote on India`s Q2 FY2026 GDP Growth Rate by Rajeev...

.jpg)

Quote on Weekly Market Outlook 28th November 2025 fr...

Watch: Defence Secy analyses India`s need for dedica...

Top News

News Not Found

Tag News

News Not Found

More News

News Not Found