West Asia Conflict to Weigh on India's Macro Fundamentals by CareEdge Ratings

India has stepped into FY27 amid an extremely challenging global landscape marked by escalating geopolitical hostilities. The ongoing conflict in West Asia has resulted in a drastic jump in international energy prices, with Brent crude oil and Liquefied Natural Gas (Japan-Korea Marker) having shot up by 55% and 90%, respectively, since the beginning of the conflict. Unlike the early phase of the Russia–Ukraine conflict, the recent hostilities have disrupted trade routes and triggered supply-side constraints, with multiple energy extraction and production facilities going offline.

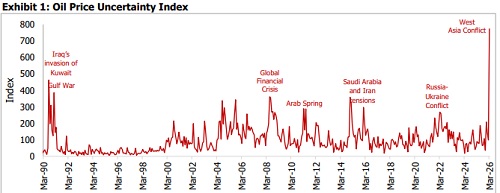

Given the time required to restore these capacities and the threat of further disruptions, energy prices are likely to remain elevated even if the conflict de-escalates early in FY27. The West Asia crisis has created significant uncertainty around global oil prices and availability (Refer Exhibit 1). Given the prolonged nature of the conflict and rising risks of disruptions, our projections for the Indian economy have been revised from our previous assessment following the outbreak of the conflict.

The recent OECD projections of growth and inflation reveal the extent of the conflict's impact. The OECD projects global growth to moderate to 2.9% in 2026 from the estimated 3.3% in 2025. Quarterly projections of global growth throughout 2026 are expected to be lower than the pre-conflict growth path (Refer to Exhibit 2). Inflation in G20 countries is expected to increase to 4% in 2026 from an estimated 3.4% in 2025. Inflationary concerns have led some major central banks to revise their near-to-medium-term inflation outlook upward (Refer to Table 1), thereby implying implications for the future direction of policy rates.

Energy Import Dependence and Economic Vulnerability

The ongoing conflict and potential damage to key energy infrastructure could disrupt supplies and pose significant risks to economies that depend on the region for energy imports. Several Asian economies, such as South Korea, India, Japan, and China, are vulnerable due to their relatively high energy imports from the Middle East (see Exhibit 3). India’s total oil and gas import dependency is estimated to be around 4.2% of its GDP (2024). Of this, reliance on the Middle East is estimated at about 2%.

Implications of the West Asia Conflict on India’s Macro Fundamentals

The global economy is currently experiencing a period of turmoil, with the impact of these developments expected to reach the Indian economy through multiple channels. The conflict has raised concerns not only about increasing global energy prices but also about disruptions to supply chains, which could spill over to growth and inflation. Given the rising risks to growth and inflation, additional fiscal support from the government is likely to weigh on the fiscal position. Furthermore, the ongoing global headwinds also draw attention to India’s external sector vulnerabilities given its high energy import dependence, export and remittance exposure to the West Asia region and moderating capital flows. Amid heightened volatility and sharp fluctuations in global oil prices, we assess key macroeconomic dynamics across multiple oil price scenarios in the following sections. Given the prolonged nature of the conflict and rising risks of disruptions, our projections for the Indian economy have been revised from our earlier assessment following the outbreak of the conflict. Our baseline assumes an average crude oil price of USD 90/bbl for the full fiscal year.

Domestic Growth Projected at 6.7% in FY27 Amid a Volatile Global Environment

The Indian economy is estimated to have held up relatively well in FY26, with the real GDP growth being pegged at 7.6% (Second Advance Estimate). This growth performance was supported by improved consumption and healthy momentum in investments. Policy support from income tax reductions, GST rate cuts, and continued thrust on capex-led growth bolstered the domestic consumption and investment scenario.

While domestic fundamentals remained relatively resilient in FY26, the escalation of conflict in West Asia has weakened the growth outlook, with the Indian economy likely to be affected through multiple channels. As per our baseline scenario for FY27, if the global crude oil prices average at USD 90/bbl for the full year, we estimate India’s GDP growth to moderate to 6.7%. This represents a downward revision from our preconflict growth forecast of 7.2% (assuming crude oil averaging between USD 60-70/bbl). Downside risks to India’s growth outlook persist, given the possibility of a prolonged war situation and higher energy prices. In an extreme case scenario where global crude oil prices average around USD 120/bbl in FY27, we see GDP growth dropping below 6% (Refer to Exhibit 4). Looking ahead, the overall duration of the conflict and the extent of its repercussions on the global supply chains are critical monitorables.

Inflation Seen at 4.5-4.7% in FY27 Amid Risks from Elevated Energy Prices & Supply Disruptions

Global energy prices have jumped drastically, with prices of Brent crude oil and Liquefied Natural Gas (Japan-Korea Marker) having shot up by 55% and 90%, respectively, since the beginning of the conflict. India is dependent on imports to meet about 88% of its total oil requirement and 51% of its gas requirement. In this context, it is important to note that India’s CPI inflation has become more sensitive to retail energy prices under the new series, with the combined weight of diesel, petrol, and LNG rising to 4.8% from 2.4% earlier. Assuming a full pass-through, a USD 10 increase in crude oil prices can lead to an estimated 55–60 bps rise in headline inflation, with around 45 bps stemming from the direct effects and 10–15 bps from the indirect effects. However, in the current scenario, the indirect inflationary pressures could be higher, given the risks of potential supply disruptions.

Overall, assuming global crude oil prices average at USD 90/bbl in FY27, India’s CPI inflation is projected to average between 4.5-4.7%. We have revised our projection upward from the earlier 4.3%, which factored global crude oil prices ranging between USD 60-70/bbl. Our revised inflation projection assumes that a large burden of the higher global crude oil prices will be borne by the government and OMCs. We have based our projection on the expectation that the OMCs may be able to absorb an increase in Brent crude oil prices up to USD 106/bbl. Furthermore, our projection also factors in government support, as reflected in the recent cut in the special additional excise duty on petrol and diesel. In an extreme scenario, if global crude oil prices average USD 120/bbl in FY27, we could also see some demand destruction, which would keep inflation in the 6.4-6.6% range.

West Asia Conflict to Push Up Government’s Fiscal Burden to 0.5% of GDP in FY27

In recent years, the Union government has demonstrated notable commitment to its fiscal consolidation targets. However, the current volatility in global economic conditions and their repercussions on the domestic economy would warrant greater fiscal support, challenging the fiscal consolidation path for FY27. Amid high global crude oil prices, the government has already announced cuts to the special additional excise duty on petrol and diesel to shield domestic consumers from higher prices. It has also imposed an export duty on diesel and Aviation Turbine Fuel (ATF) to maintain sufficient domestic availability. We estimate the net revenue foregone from the cut in excise duty, adjusted for export duty revenue, to be around Rs 1.1 trillion.

Another pressure point for government finances is expected to be the additional fertiliser subsidy outgo amid challenges to fertiliser imports and higher LNG prices. India sources over a quarter of its fertiliser imports from West Asian countries. Moreover, around one-third of the global seaborne fertiliser trade (about 16 million tonnes) passes through the Strait, raising concerns about access to fertiliser. Also, more than 60% of India’s urea production relies on imported LNG as a feedstock. Given this background, we estimate the government’s subsidy outgo on fertilisers to rise by about Rs 38,000 crore over the budgeted Rs 1.7 trillion.

The repercussions of the West Asia conflict on the Indian economy are expected to be through multiple channels and across several sectors. This, in turn, is expected to weigh on India’s overall growth momentum, potentially translating into lower tax collections for the government. Our preliminary analysis suggests that the government’s tax collections in FY27 could be lower by about Rs 40,000 crore. The ultimate impact of the West Asia conflict on not just India’s tax collections but also its broader fiscal health will depend on how long the conflict persists and the scale of disruptions. Overall, we estimate the fiscal burden from the excise duty cut on petroleum products, along with the possibility of an increase in fertiliser and fuel subsidy burden and lower tax revenue collections, to be around 0.5% of GDP in FY27. However, the government’s Economic Stabilisation Fund should provide some buffer to address rising fiscal pressures.

10Y G-Sec Yields Projected between 6.8-6.9% Amid Heightened Uncertainties & Fiscal Pressures Elevated oil and gas prices are stoking fears of increased fiscal and inflationary pressures, thereby pushing up Gsec yields across tenors. Beyond the war's repercussions, higher-than-expected state government borrowing is also contributing to the rise in yields. As a result, the 10Y G-sec yield has risen 37 bps in March, crossing 7%, a level last seen in July 2024. Looking ahead, G-sec yields are expected to face upward pressure due to heightened global uncertainties, inflationary pressures, and rising fiscal challenges. We estimate the fiscal burden from the excise duty cut on petroleum products, along with the possibility of an increase in subsidy burden and lower tax revenue collections, to be around 0.5% of GDP in FY27. As per our baseline scenario, we expect G-sec yields to average 6.8 – 6.9% over the year, assuming early resolution of the conflict. However, should oil average USD 120/bbl through the year, rising fiscal pressures would push yields above 7.4%.

India’s Current Account Deficit Projected at 2.1% of GDP in FY27

India’s current account deficit is expected to face challenges amid the ongoing global turmoil, given its high energy dependence. India is dependent on imports to meet about 88% of its total oil requirement and 51% of its gas requirement. Over the past five years, India has expanded its supply from the US and Russia. However, West Asia still accounts for a large 51% of India’s total crude oil imports. India imports 5.5–6 million barrels of crude oil per day. A USD 10 increase in crude prices could raise India’s import bill by around USD 20 billion. Given that India also exports a significant share of refined petroleum products, a USD 10 rise in crude prices could increase the current account deficit (CAD) by 30–40 basis points. Apart from crude oil's impact, there are two additional risks stemming from the exposure of exports and remittances to West Asian economies. India’s merchandise exports to West Asia were USD 64 billion (14.7% of total exports) in FY25. Furthermore, India’s remittances remain vulnerable to shocks from the West Asia conflict, as the Gulf Cooperation Council (GCC) countries account for nearly 38% of India’s total inward remittances, amounting to more than USD 130 billion. Overall, factoring in global crude oil prices averaging at USD 90/bbl for the full year, along with some pressure on exports and remittances, we estimate India’s CAD to widen to 2.1% of GDP (Vs our pre-conflict projection of ~1%).

At a time when India’s current account is facing renewed pressure, driven by its high dependence on energy imports and challenges to exports, it is important to note that India’s capital flows have also come under pressure amid volatile FPI flows and moderating net FDI. India’s FPI outflows further intensified following the West Asia conflict, reaching USD 13.6 billion in March, the highest monthly outflow in the last six years. With this, FPI outflows for FY26 were recorded at USD 16.6 billion, as against inflows of USD 2.7 billion in FY25. Looking ahead, persistent global uncertainties, elevated crude oil prices, and rupee weakness are likely to keep investor sentiment cautious, weighing on the FPI flows. Furthermore, net FDI inflows (Gross inflows – Repatriation – FDI by India) have consistently been negative over the past six months. Higher repatriations and FDI outflows have been weighing on India’s net FDI inflows. During 10M FY26, India’s net FDI inflows were weak at USD 1.7 billion following a poor USD 1 billion in FY25.

Rupee to Average Between 92-93 in FY27

Over the period of these hostilities, most major currencies have depreciated against the US dollar, while the dollar itself has strengthened by around 2.8% during the same period (Refer to Exhibit 11). Weakness in foreign investment flows, pressures on the current account deficit and global risk-off sentiment have kept the rupee under pressure. The rupee has depreciated by 4.3% (30th Mar-26) against the dollar since the beginning of the conflict in West Asia. However, the rupee remains significantly undervalued as at the end of February 2026 in REER terms (Refer to Exhibit 12). This suggests that when global conditions improve, the rupee has scope to appreciate, supported by favourable domestic fundamentals and bolstered by the recently concluded trade agreements.

The RBI has recently announced measures to curb volatility in the rupee arising from speculation. It directed banks to limit their net open exposure to the currency in the forex market to USD 100 million by the end of each day beginning April 10th to help ease currency volatility. It further reinforced these directions by barring banks from offering rupee non-deliverable forwards (NDFs) to resident and non-resident clients. The Central Bank may introduce further measures to contain currency volatility, depending on evolving conditions.

If the conflict ends soon and crude oil averages USD 90/bbl in FY27, we project the rupee to average around 92-93. If the conflict intensifies, leading to oil prices averaging a high of USD 120/bbl in FY27, we project the rupee to average close to 98 over the year.

Looking Ahead

The current global economic uncertainty comes at a time when the domestic economy was gaining traction, supported by improving consumption and signs of revival in private investment. The global headwinds have risen dramatically with the intensification of the West Asia conflict. Any further escalation in the conflict poses material risks to the fundamentals of the global and domestic economies. There are heightened concerns not just about the global energy price trajectory but also about risks from global supply chain disruptions, which could have severe repercussions across many industries. Looking ahead, the duration of the conflict, along with its impact on the global energy prices and supply chains, will be the key factors to monitor.

Above views are of the author and not of the website kindly read disclaimer