UPI Eyes 240 bn Domestic Transactions in FY26 & Continues Expanding Globally by CareEdge Ratings

Synopsis

* India’s payments ecosystem has undergone a structural transformation from cash-led to digitally dominant, with digital modes accounting for 99.8% of the total transaction volume and 93% of value. This shift has been enabled by strong policy support, interoperable infrastructure (UPI-led) and rapid fintech adoption alongside rising financial inclusion and merchant digitisation

* The global payments landscape is rapidly shifting towards real-time, interoperable systems, with Unified Payments Interface emerging as a powerful solution, positioning India at the forefront of digital public infrastructure and shaping the future of cross-border payment ecosystems.

* This transformation is further catalysed through strong network effects and ecosystem depth, increasing participation from banks, fintechs, and merchants, creating a self-sustaining digital payment ecosystem that continues to drive higher adoption, innovation and efficiency across the value chain.

Overview of Retail Payments System in India

India’s retail payments ecosystem is one of the world’s most advanced and interoperable digital payments market. Anchored by regulatory oversight from the RBI and powered technologically by the NPCI, India, today operates a payment landscape that seamlessly integrates traditional instruments such as cheques and cards with modern digital platforms including UPI, IMPS, ABPS and PPIs.

This integrated framework has not only ensured operational efficiency but has also accelerated financial inclusion and digital penetration across the country.

The Indian Digital Payments Ecosystem: Structural Catalysts at Play

The Indian government and the RBI are promoting digital adoption nationwide, particularly in Tier-2 and Tier-3 cities, supported by initiatives such as the PIDF, which aims to accelerate digital payments in underserved regions.

Digital payments, led by UPI, AePS, IMPS and others, dominate retail transactions, accounting for 93% of payment value and 99.8% of transaction volume as of 9MFY26. Cards and prepaid instruments are stable or in decline as UPI substitutes for low-value transactions. While UPI leads, other systems, such as NEFT, IMPS, and NACH, remain important, especially for high-value and bulk payments. NEFT remains crucial for mid-to-high-value transactions, with an average ticket size of approximately Rs 48,289 as of January 2026, which is significantly higher than that of UPI whose average ticket size is of Rs 1,298 as of same date. IMPS continues to experience steady growth but is lagging behind UPI, which offers a similar instant payment experience with broader merchant acceptance. NACH transactions remain important for bulk disbursements such as salaries, subsidies and dividends.

UPI is not merely a tool of convenience, but an instrument of empowerment. Across India, UPI is enabling individuals and small businesses to increasingly participate in the formal financial ecosystem with greater convenience. From urban micro-entrepreneurs to rural households, people can securely receive and transfer money instantly. The digital ecosystem has also enabled the government to deliver benefits directly into beneficiaries’ bank accounts, ensuring greater transparency, efficiency and reduced reliance on intermediaries. For the Indian Government, this happens to be a matter of pride. More than 89% of adults in India now have bank accounts, many enabled by Aadhaar and Jan Dhan Yojana, and UPI has become the bridge connecting them to the digital economy.

UPI Expected to Account for Major Chunk of All Retail Digital Transactions in India

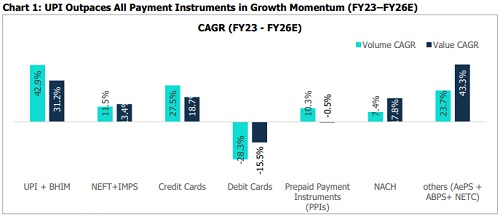

While credit cards are still widely used for e-commerce and high-value purchases, debit cards and Prepaid Payment Instruments (PPIs) are losing ground to UPI for smaller transactions.

NEFT and IMPS still dominate with a majority share, but their share has declined gradually compared to FY23. UPI (including BHIM) has emerged as a key driver of structural growth, increasing its value share. The ecosystem is rapidly converging toward a UPI-led payments architecture, with continued headroom for share expansion.

UPI has become the default rail for retail payment volumes, rising from 73.6% (FY23) to 86% (FY26E), with other modes now marginal. Its dominance is driven by wide QR acceptance, seamless real-time experience, almost zerocost structure, and strong fit for everyday transactions. UPI is not just gaining share, it is entrenching itself as the core payments infrastructure, with sustainable drivers supporting further scale and limited disruption risk.

Recent Innovation Accelerating UPI Growth

The BHIM app has introduced biometric authentication (fingerprint/face ID) for UPI payments, allowing users to transact up to Rs 5,000 without entering a UPI PIN. This enhances convenience, especially for users who forget their PIN, while maintaining security through device-level verification. The feature supports multiple payment modes (QR, UPI ID, mobile number) and reflects a broader push to make Unified Payments Interface more frictionless and accessible, further driving adoption.

In order to support small scale merchants in adopting digital payment systems including UPI, various initiatives have been taken up by the Government, the RBI and NPCI from time to time. These inter alia, include incentive scheme for promotion of low value BHIM-UPI transactions, and the PIDF which provides grant support to the banks and fintech’s for deployment of digital payment infrastructure (such as POS Terminals and QR codes) in Tier-3 to 6 centres. UPI has played a pivotal role in promoting financial inclusion and accelerating the nation’s shift towards a cashless economy. Its remarkable growth, both in terms of transaction volumes and geographical reach, highlights its transformative impact on the financial landscape. UPI has not only revolutionised the way India conducts financial transactions but has also positioned the country as a global leader in digital payments.

The Global Context: India at the Forefront of Real-Time Payments India’s digital payments journey has attracted global recognition for its scale, interoperability and inclusivity. The IMF recognised UPI as the world’s largest retail fast-payment system by transaction volume. It is estimated that UPI accounts for approximately 49% of global real-time payment transaction volumes. UPI has cemented India’s position as the global leader in real-time payments, distinguished by its scale, interoperability, and system-wide integration. This leadership signals a paradigm shift, with India not just leading in volumes but actively defining the global blueprint for digital payment ecosystems.

UPI Goes Global: Expanding India’s Payments Footprint

India has extended UPI’s reach to eight countries - Bhutan, France, Mauritius, Nepal, Qatar, Singapore, Sri Lanka, and the UAE. The international expansion is being driven by NPCI International Payments Limited (NIPL), which has onboarded more than two million international merchants.

Outlook

UPI’s trajectory reflects more than transaction growth; it signals the maturation of India’s digital public infrastructure. With rising internet tele-density, expanding financial inclusion, increasing merchant digitisation, and sustained regulatory support, UPI is positioned for continued structural growth. As India accounts for nearly half of global realtime payment volumes, the continued internationalisation of UPI and RuPay reinforces the country’s role in shaping the future architecture of interoperable and inclusive digital finance.

India is poised to extend its leadership in digital payments to the global stage, leveraging the success of Unified Payments Interface to shape cross-border payment frameworks within BRICS. The focus is shifting toward interoperable systems and CBDCs to enable seamless, real-time, and cost-efficient international transactions. This positions India to play a pivotal role in redefining global payment architecture, while enhancing efficiency in trade, remittances, and financial integration across emerging economies.

India’s Unified Payments Interface has become the backbone of the digital payment ecosystem, driving scale, efficiency, and financial inclusion. Its interoperable, low-cost model has transformed everyday transactions and positioned India as a global leader in real-time payments.

Going forward, continued innovation and global expansion are set to further strengthen as highlighted in Payments Vision 2028 by the RBI. It outlines a strategic roadmap to strengthen and future-proof India’s digital payments ecosystem, focusing on resilience, inclusivity, security, and innovation. It emphasizes enhancing cross-border payment efficiency, interoperability (including TReDS), and customer protection frameworks, while promoting ease of doing business through streamlined regulations and new initiatives like Payments Switching Service and support for small payment providers. The vision also prioritizes cybersecurity, research capacity, data accessibility, and innovation in areas such as cards and electronic cheques, ensuring India’s payment infrastructure remains robust, scalable, and globally aligned.

CareEdge Advisory’s View

“With 694 banks live on UPI and monthly volumes exceeding 20 billion transactions, amounting to over Rs 26 lakh crores in February 2026, India’s UPI ecosystem has achieved remarkable scale and depth. This strong growth reflects increasing adoption, expanding reach, and the robustness of India’s digital payments infrastructure, positioning UPI for continued expansion and deeper integration across use cases,” says Kalpesh Mantri, Assistant Director at CareEdge Advisory.

India's payments system is undergoing a structural shift towards a hybrid model, where digital and cash channels coexist, serving distinct yet complementary roles. Supported by a conducive regulatory environment and innovations that enhance interoperability, UPI is well-positioned to consolidate its role as the backbone of India’s payments landscape, driving both transactional efficiency and broader economic participation.

“UPI has emerged as a global leader, accounting for nearly 49% of global real-time payment volumes, and powers the world’s largest real-time payment system in India. UPI has transformed domestic payments and is now expanding internationally with presence across multiple countries and over 2 million international merchants, setting the benchmark for digital payment systems worldwide,” says Tanvi Shah, Senior Director at CareEdge Advisory.

Above views are of the author and not of the website kindly read disclaimer