Sell Relaxo Footwears Ltd for the Target Rs. 280 by Motilal Oswal Financial Services Ltd

Demand recovers on GST tailwinds; price hikes could slow momentum

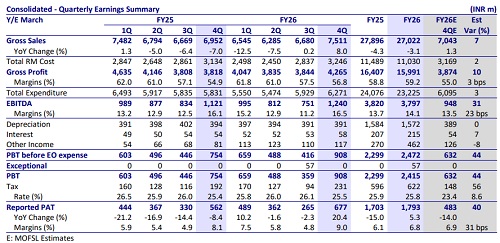

* Relaxo Footwears (RLXF) ended FY26 on a strong note, delivering its first positive volume growth in eight quarters (+10% YoY; 7% beat), driven by GST rationalization and GT recovery. Underlying retail growth remained healthy at ~5–6%, while a 180bp GM expansion drove EBITDA growth of 11% YoY to INR1.2b (31% beat).

* FY26 revenue declined 3% YoY on weak volumes. Better gross margins and tight cost control kept pre-Ind AS EBITDA broadly flat at INR3.7b.

* While demand recovery has improved, management remains cautious amid inflationary and geopolitical uncertainties. Further, the recent 15–18% price hikes taken to offset input cost inflation could partially reverse GST-led competitiveness vs unorganized players and moderate volume recovery.

* We raise FY27E EBITDA/PAT by ~5% and retain FY28E estimates, implying FY26–28E CAGR of 7%/13%/11% in revenue/EBITDA/PAT.

* Despite the recent correction, valuations remain demanding at ~41x FY27E P/E. We reiterate Sell with a revised TP of INR280, based on 30x FY28E EPS.

Volume-led recovery drives a sharp 4Q beat

* Revenue grew ~8% YoY to INR7.5b (7% ahead), marking the first meaningful recovery after eight quarters of flat-to-negative growth.

* Volume growth remained strong at ~10% YoY to 50m pairs, while ASP declined 2% YoY to INR150, indicating a volume-led recovery.

* Gross profit grew ~12% YoY to INR4.3b (10% ahead), with GM expanding 185bp YoY to 56.8% (~180bp beat), aided by a favorable base as 4QFY25 margins were impacted by inventory reduction-led clearance.

* Employee and other expenses grew 8%/11% YoY, respectively, reflecting normalization in operating spends amid improving demand.

* EBITDA grew ~11% YoY to INR1.24b (31% beat).

* EBITDA margins expanded by a modest 40bp YoY to 16.5%, as strong GM recovery was partly offset by higher operating costs.

* Other income increased 44% YoY to INR117m, while finance costs rose 8% YoY.

* PBT grew ~21% YoY to INR908m (44% beat).

* Reported PAT grew ~20% YoY to INR677m (40% beat), with PAT margins expanding ~90bp YoY to 9.0%.

FY26 performance summary

* FY26 revenue declined 3% YoY to INR27b amid weak demand conditions during 1HFY26.

* Volumes declined ~2% YoY to 174m pairs, while ASP declined ~2% YoY to INR151.

* Gross profit declined ~3% YoY to INR16b, though GM expanded marginally by ~40bp YoY to 59.2%, supported by better cost efficiencies.

* Tighter cost control aided profitability, with employee costs rising only 2% YoY, while other expenses declined 5% YoY.

* EBITDA remained broadly flat YoY at INR3.8b, with margins expanding ~35bp YoY to 14.1%.

* Pre-Ind AS EBITDA stood at ~INR3b (down 4% YoY), with margins broadly stable at ~11.2%.

* Reported PAT grew 5% YoY to INR1.8b, aided by higher other income (+71% YoY) and stable depreciation despite flattish EBITDA growth.

* Inventory and receivable days remained stable at 75/40 days, respectively, while payable days increased to 35 days (vs. 26 days YoY). Core working capital improved to 80 days (vs. 88 days in FY25), with absolute CWC declining 12% YoY to INR5.9b, largely driven by higher payables.

* OCF (post-lease payments) declined 18% YoY to INR2.8b, primarily due to lower working capital release.

* Capex increased ~18% YoY to INR1.4b.

* FCF generation declined to INR1.4b (vs. INR2.3b in FY25), largely reflecting lower working capital benefits and higher capex.

Key highlights from the management commentary

* Demand recovery gained traction in 4QFY26, supported by GST rationalization and improving GT demand, with management indicating underlying retail growth of ~5–6%. While momentum remains encouraging, the company remains watchful of the impact of inflation, geopolitical uncertainty, and recent price hikes on consumer demand.

* Pricing actions have largely offset cost inflation, with ~15–18% price increases implemented to mitigate higher raw material and labor costs. As commodity inflation begins to ease, management expects gross margins to expand and is targeting >100bp expansion in operating margins versus FY26 levels.

* Growth strategy is centered on premiumization and channel expansion, including a broader athleisure portfolio, higher ASP offerings, deeper distributor penetration, e-commerce scaling, and increased focus on women and kids categories. Management continues to target sustainable volume growth of ~4– 5% over the medium term.

* FY27 capex of INR1.8–2.0b will support retail expansion and operational upgrades, including the addition of 100 EBOs. Early results from the new store format are encouraging, with better product mix, higher footfalls, and stronger profitability, leading management to expect retail expansion to be both growthaccretive and margin supportive.

Valuation and view

* RLXF delivered its first positive volume growth in eight quarters, driven by GST rationalization and improving GT demand. However, the recovery remains at an early stage, and management remains cautious amid inflationary pressures, geopolitical uncertainties, and the impact of recent price hikes on consumer demand.

* GST reduction has structurally improved the competitiveness of organized players vs the unorganized sector, supporting demand recovery. In parallel, the company's focus on premiumization, channel expansion, and cost efficiencies should aid gradual margin expansion.

* While recent volume recovery is encouraging, sustaining it remains key. The company has implemented 15–18% price hikes to offset input cost inflation, which could partially reverse the pricing advantage created by GST rationalization and temper volume growth going forward.

* We raise FY27E EBITDA/PAT by ~5% and retain FY28E estimates, implying FY26– 28E CAGR of 7%/13%/11% in revenue/EBITDA/PAT. However, recent price hikes could pose downside risks to volume recovery.

* Despite the recent correction, valuations remain demanding at ~41x FY27E P/E. We reiterate Sell with a revised TP of INR280, based on 30x FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412