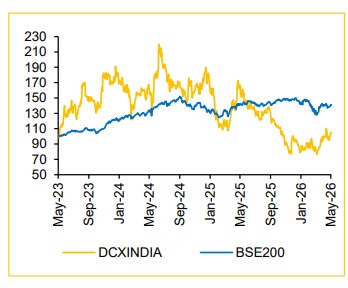

Sell DCX Systems Ltd for the Target Rs.150 by Choice Institutional Equities

Execution Concerns Deepen; Visibility Remains Absent

DCX Systems reported another weak quarter, with continued pressure across revenue, margin and profitability, extending the trajectory of underperformance seen in the past several quarters. The lack of improvement in execution raises concerns around the company’s ability to translate its order book into sustainable earnings. More importantly, the continued absence of engaging with the mgmt. and forwardlooking disclosures for multiple quarters, significantly limits visibility. While the order book remains healthy at INR 29,840 Mn (4.0x of FY26 revenue), backlog strength alone provides limited comfort without consistent execution and margin recovery. A sustained trajectory of revenue degrowth in the past two years, along with repeated quarterly misses, indicates that the challenges may be more structural than cyclical. With no guidance from the management, assessing earnings trajectory or recovery timelines remains difficult, thereby weakening confidence in operating leverage assumptions. The only positives continue to be external, including favourable geopolitical dynamics and potential outsourcing opportunities in defence electronics manufacturing. However, this remains to be a long-term optionality and is yet to reflect in execution or financial performance. Given the continued weakness in earnings delivery and limited visibility, we downgrade DCX Systems to SELL (from Reduce) with a revised target price of INR 150 (30x FY28E EPS), implying a considerable downside from the current level. We would turn constructive only upon clear evidence of execution improvement and margin stabilisation.

Another Disappointing Quarter

* Revenue for Q4FY26 was down by 62.3% YoY and up by 71.2% QoQ at INR 2,073 Mn (vs CIE estimate of INR 6,050 Mn)

? EBITDA for Q4FY26 stood at INR -2.8 Mn (vs CIE estimate of INR 128 Mn). EBITDA margin stood at -0.1%, contracting by 200 bps YoY (vs CIE estimate of 2.1%)

* PAT stood at INR -2.5 Mn (vs CIE estimate of INR 262 Mn). PATM contracted by 389 bps YoY, reaching -0.1% (vs estimate of 4.3%)

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131