Reduce BHEL Ltd For Target Rs.368 by Prabhudas Liladhar Capital Ltd

Strong Q1; further execution ramp-up on cards

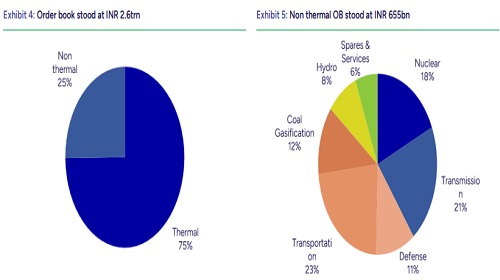

We revise our FY27E/FY28E EPS estimate by +5.4%/+5.8% accounting for improvement in execution and normalization in provision. BHEL delivered a strong Q1FY27 performance, with revenue growing 40% YoY and EBITDA margin expanding to 6.5%, supported by lower other expenses. The Power segment (~52% YoY) remained the key growth driver, backed by execution of a healthy order book of ~INR1.9trn. Recent order wins, including the INR210bn EPC award for the 3×800MW Meja thermal power project and BHEL's largest-ever export order (~INR22.5bn) for generator packages for the Dangote refinery, have taken the Power segment order book to ~Rs2.1trn. Along with the current pipeline, opportunities in nuclear, coal gasification and green hydrogen are expected to provide new growth avenues. The Industrial segment reported ~12% YoY revenue growth, with order inflows of ~INR17.7bn driven by transmission, O&G and transportation, while opportunities across HVDC & Green Energy Corridors, defence and rail mobility are expected to drive incremental order inflows and strengthen diversification across end markets. BHEL offers strong multiyear revenue visibility, with robust execution momentum and sustained investments in India's power and infrastructure sectors expected to support future growth. The stock is currently trading at P/E of 44.2x/29.6x on FY27E/FY28E. We maintain our ‘Reduce’ rating on the stock given recent rally in the stock price, with a TP of Rs368 (Rs321 earlier) valuing the stock at a PE of 25x Mar’28E (23x Sep’28E earlier) owing to better execution.

Long term view: We believe

1) large thermal power order pipeline,

2) diversification into railways, defense, green hydrogen, coal gasification, etc

3) growing exports business augurs well for BHEL. However, execution pace and balance sheet health continues to be key monitorable

Power execution drove revenue growth, while lower expenses aided profitability:

Standalone revenue grew by 40% YoY to INR77bn (PLe: Rs64.4bn) led by growth in Power segments (+51.8% YoY to INR59.2bn) and Industry segments (+12% YoY to INR17.8bn). Gross margin expanded by 202bps YoY to 31.2% (PLe: 29.2%) likely due to favourable product mix. EBITDA came in at INR5bn vs loss of INR5.3bn in Q1FY26 (PLe: loss of Rs1.2bn) with EBITDA margins expanded to 6.5% vs -9.8% in Q1FY26 (Ple: -1.8%) aided by lower other expenses (-42% YoY to Rs3.9bn) and employee expenses (-709bps YoY as % of sales). Adj. PAT came in at INR3.8bn vs a loss of INR4.5bn in Q1FY26 (Ple: loss of INR1.2bn) driven by increase in other income (+24.5% YoY to INR2.3bn) while effective tax rate remained flattish at 25.5% (vs 25.1% in Q1FY26).

Long term view: We believe

1) large thermal power order pipeline,

2) diversification into railways, defense, green hydrogen, coal gasification, etc

3) growing exports business augurs well for BHEL. However, execution pace and balance sheet health continues to be key monitorable

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271