Oil and Gas Sector Update : Geopolitics Steering Oil Prices by Choice Institutional Equities

Developments over the past week:

* The US President informed at the time of writing this report (March 27, 2026) that he has extended his deadline to attack Iran’s energy infrastructure by 10 days to April 6, 2026.

* Meanwhile, Iran has put forward 5-point proposal to end the war: (i) total halt to attacks (ii) guarantees against future conflict (iii) war damages payment (iv) cessation of hostilities on all regional fronts (v) recognition of Iran’s control over the Strait of Hormuz.

* As per market reports, 40% of Russia’s oil export capacity is offline, factoring port outages, pipeline issues and tanker-related disruptions. The development is on the back of as fresh wave of attacks by Ukraine which knocked out key Baltic export infrastructure.

* As per the press release issued by the Government of Indian on March 26, 2026: (i) India is receiving more crude from across the world than what was previously arriving through the Straits (ii) Every Indian refinery is running at over 100% utilization (iii) Crude oil supplies for next 60 days have already been tied by Indian Oil Companies (iv) There is no LPG shortage as domestic refinery production has been ramped up by 40%, raising daily output to 50 TMT, accounting for >60% of nation’s requirement. Meanwhile, 800 TMT of assured inbound LPG cargoes are already secured and enroute from the US, Russia, Australia and other countries. Approximately, one full month of supply is firmly arranged, with additional procurement being finalised continuously.

* The excise duty on petrol has been reduced from INR13/L to INR3/L by Indian Government. Meanwhile, the excise duty on diesel has been slashed from INR10/L to nil.

In our opinion:

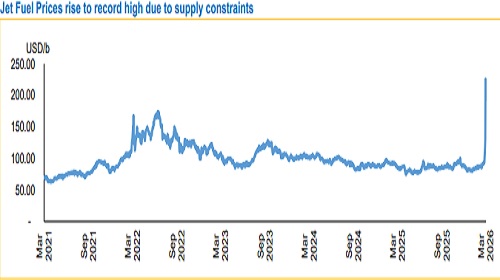

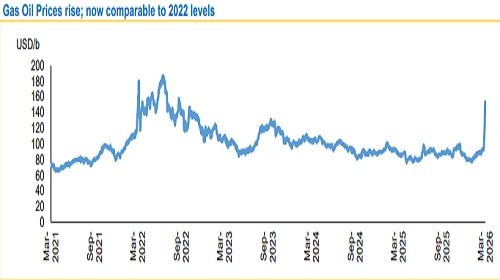

* The current Brent prices are primarily being driven by Geopolitical risk premium which has been building and evaporating, reflecting the ebb and flow in the intensity of the conflict. However, it is not yet reflecting physical deficit that is being observed in the Southeast Asia, as countries are importing grades of crude at a premium which were previously available at discount.

* The Brent prices would sustain at higher levels (USD110b to USD130/b) as the market bakes in the precautionary demand and scarcity premium. If the Hormuz situation remains status quo without progress in US-Israel-Iran negotiations, declining floating inventories and tightening marginal storage could drive a sharp increase in oil prices, leading to sustained higher prices during the month of April. We have built the following scenarios and implications of the same as below:

* Provided there is escalation of conflict over the upcoming weekend and continues through the entire month of April without abating, we expect the Brent price to average at USD130/b for the month of April.

* If negotiations begin but repeatedly fail through April, we expect Brent to average ~USD 110/b for the month, with elevated volatility. Our April forecast assumes the current supply deficit of ~7–11 mb/d persists, which would keep prices supported near USD 110/b. Brent has averaged USD 97.23/b between March 1 to 26.

* If US-Israel intervention leads opening of the Strait of Hormuz, with flows resuming gradually Brent prices could retreat towards ~USD 90/b over the coming weeks. This would largely reflect the unwinding of the precautionary demand premium, although a residual geopolitical risk premium may persist.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131