Neutral Westlife Foodworld Ltd for the Target Rs. 535 by Motilal Oswal Financial Services Ltd

Slightly better print; near-term pressure on margins

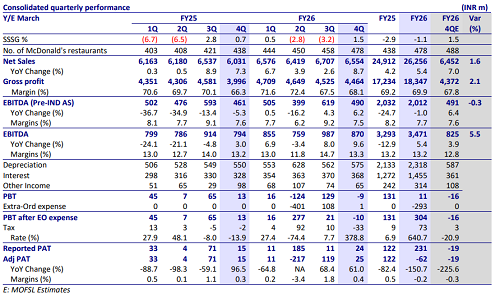

* Westlife Foodworld (WESTLIFE) reported a revenue growth of 9% YoY to INR6.6b in 4QFY26 (est. INR6.4b). The same-store sales growth (SSSG) stood at 1.5% YoY (in line). On-premise sales grew 9% YoY, driven by positive footfall growth across all three months of the quarter. Off-premise sales increased 6% YoY. The West region continued to witness healthy growth momentum, while recovery trends have started in the South market (positive footfalls, flat SSSG). Footfalls grew in mid-single digits, supported by value meal offerings (INR99 platform) and brand-building initiatives, with the momentum sustaining into April as well.

* The company added 20 net new stores in 4Q (40 in FY26), taking the store count to 478. The company plans to open more than 60 restaurants annually going forward (vs. the earlier guidance of 45–50 stores) and aims to grow its network to 580-630 restaurants by 2027.

* GM expanded 190bp YoY to 68.1% (est. 67.8%), led by supply-chain efficiencies, internal cost optimization initiatives, and favorable annual procurement contracts. EBITDA margin was flat YoY at 13.3%. (est. 12.8%). EBITDA margin (pre-IND AS) was slightly down by 20bp YoY to 7.5%. Management guided ~67% gross margin in FY27 amid the ongoing inflationary environment. The company will take calibrated price hikes of 2–4% to offset input cost pressures, while no major price increase has been implemented over the last 4–5 months.

* We believe regional demand will see a gradual improvement, and, therefore, we expect a gradual ADS recovery in the near future. We reiterate our Neutral rating with a TP of INR535, based on 28x Mar’28E EV/EBITDA (pre-IND AS).

SSSG up 1.5%; margin trajectory improves

* Same store revenue up 1.5%: Sales grew 9% YoY to INR6.6b (est. INR6.4b), led by a store addition of 9% YoY and healthy guest count momentum. The West continued to deliver a healthy performance while the South has started recovering. SSSG was 1.5% YoY in 4QFY26 (est. 1.5%, -3% in 3QFY26, +0.7% in 4QFY25). The company opened 20 net stores (opened 21 stores, and closed one store), taking the count to 478 in 78 cities. Average sales per store declined 6% YoY to INR60m (annual) in 4QFY26.

* EBITDA (pre-IND AS) up 6% YoY: GM expanded 190bp YoY to 68.1% (est. 67.8%). The reported GM reflects a one-off optical impact of 200bp in 4QFY26 due to the reclassification of processing charges from opex to COGS. EBITDA grew 10% YoY to INR870m (est. INR825m). EBITDA margin was flat YoY at 13.3%. (est. 12.8%). EBITDA margin (pre-IND AS) was down marginally by 20bp YoY to 7.5%, EBITDA (pre-IND AS) rose 6% YoY. Restaurant Operating Margin (ROM) post-IND AS rose 70bp YoY to 19.8% (est. 19.1%). ROM pre IND AS was up 50bp YoY to 14% (est. 13.9%).

* In FY26, net sales/EBITDA rose 5% each. EBITDA Pre-Ind AS was down 1%.

Key takeaways from the management commentary

* The underlying guest count growth was in the mid-single digits during the quarter. The momentum has continued into April as well.

* Management guided that gross margins may normalize at 67% going forward, considering inflationary pressures, although cost optimization initiatives are expected to partially offset these headwinds. ? The company will take 2–4% annual price hikes in a calibrated manner to offset inflation. WESTLIFE has not taken major price hikes over the last 4–5 months.

* WESTLIFE plans to open more than 60 restaurants annually going forward, compared to the earlier guidance of 45–50 stores.

Valuation and view

* We cut our EBITDA estimate by 4% for FY27 and largely maintain our estimate for FY28.

* Management guided ~67% gross margin in FY27 amid the ongoing inflationary environment. The demand trajectory improved in 4Q, with positive footfalls across months. WESTLIFE has become more aggressive in store additions (60 per year vs. 45-50 per year earlier).

* We believe regional demand will gradually improve, and, therefore, we expect a gradual ADS recovery in the near future. We reiterate our Neutral rating with a TP of INR535, based on 28x Mar’28E EV/EBITDA (pre-IND AS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412