Neutral Vedant Fashions Ltd for the Target Rs. 420 by Motilal Oswal Financial Services Ltd

Valuations turning attractive, but consistent growth remains key

We recently interacted with Mr. Vedant Modi, Chief Revenue Officer of Vedant Fashions (VFL). Below are the key takeaways:

* VFL is navigating a prolonged slowdown; the management largely attributes it to macro factors (slowdown in hiring by IT companies, weak discretionary demand in the mid-premium category, etc.) and, to a lesser extent, to higher organized competition in the ethnic wear space.

* Management indicated that organized ethnic wear stores increased from 500 to 2,500 in the past few years, with part of it driven by VFL’s high profitability. However, the bulk of the new entrants are loss-making, and, of late, the store openings have ebbed.

* VFL is targeting ~8% SSSG on a steady-state basis, driven by interventions to boost footfalls, improve conversions, and ~3-4% annual ASP increases, while it continues to focus on improving the quality of its retail network.

We build in a modest ~5-6% revenue, EBITDA, and EPS CAGR over FY26-28E, primarily led by mid-single-digit SSSG, as net retail area addition could remain modest.

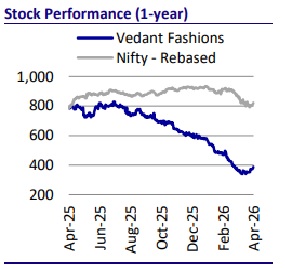

* Following a 45% correction over the last 12 months, VFL trades at 28x 1-yr FY27E EPS, undemanding for a business expected to generate ~INR6b FCF over FY26-28 with ~17-18% RoE. However, we await signs of a sustained demand recovery before turning constructive. Reiterate Neutral with an unchanged TP of INR420, premised on 25x FY28E EPS.

Macro slowdown hurting growth; competitive intensity stabilizing

* Management believes that the growth in mid-premium categories has been hurt primarily by macro factors (~65% of the impact) such as a slowdown in IT hirings, weak wage growth, and slower migration from low- to mid-income households, while higher competitive intensity has had a lesser impact.

* Over the past few years, the organized ethnic wear EBO count had increased significantly from ~500 to 2,500 as more players got attracted by the profit margins on Manyavar.

* However, compared to consistent 25%+ profit margins for Manyavar, most ethnic retailers are struggling with either low single-digit profitability or are currently loss-making.

* Lack of profitability, along with macro slowdown in the mid-premium category, has driven some industry consolidation with significant store closures (albeit offset by store openings by some larger retailers, who are currently in the build-out phase), leading to a stable competitive environment.

* A data-led inventory model (~95%+ full-price sell-through vs. ~60% for peers) drives VFL’s strong profitability and operating strength (vs. peers) and remains the core structural moat in an industry where dead stock is a key challenge.

Multi-pronged approach to boost SSSG and improve retail network health

* VFL is targeting a mid-to-high single-digit (~8%) steady-state SSSG, while improving the quality of its retail network through disciplined store openings and consolidating low-productivity and unprofitable stores.

* The company is taking initiatives on all the variables, such as footfalls, conversions, ASP, and ABV, to deliver ~8% SSSG on a steady-state basis.

* Marketing is becoming more ROI-driven with better use of digital and AI, alongside store-level interventions (such as improved layouts and localized activation) aimed at improving footfalls and boosting conversions. Further, the company is also working on improving repeat purchases by leveraging the existing customer data and introducing certain loyalty programs.

* Management believes that the company did not take adequate price hikes in the last few years, and going forward, it would target ~3-4% annual price hikes while improving the product’s perceived quality. However, it would not use ASP hikes as a lever to protect or increase margins.

* Improvement in retail network quality is another key driver for VFL to deliver sustained double-digit growth. Management indicated that out of ~1.8m sqft retail network, ~0.1-0.2m sqft is currently low in productivity due to a variety of reasons and would likely undergo consolidation. The revenue impact from such closures would be limited, and the company would continue to open stores, albeit maintaining a strict discipline on the store-level economics and return metrics.

Manyavar remains the key anchor, with Twamev witnessing strong traction

* Manyavar, the core brand, continues to anchor the portfolio, driving the bulk of revenue and footfalls with a strong full-price sell-through.

* Twamev, a premium brand, is scaling with a throughput-led model of fewer stores and higher productivity. The brand already contributes ~35% of sales in top-performing stores, aided by digital-first marketing and sharper positioning in metro markets.

* Mohey is pivoting towards the non-bridal category, with a focus primarily on colocated stores with Manyavar, rather than standalone stores, to drive higher footfalls, cross-selling, and boosting conversions.

* Divas, an online-led, entry-price brand

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412