Neutral TCI Express Ltd For Target Rs. 520 by Motilal Oswal Financial Services Ltd

Steady 4Q; volume recovery to be gradual

* TCI Express’s (TCIEXP) 4QFY26 revenue grew 6% YoY to INR3.2b (in line). EBITDA stood at INR331m (+26% YoY), 3% above our estimate. EBITDA margin came in at 10.1% in 4QFY26 vs. our estimate of 10%. APAT rose ~7% YoY to INR208m vs our estimate of INR220m.

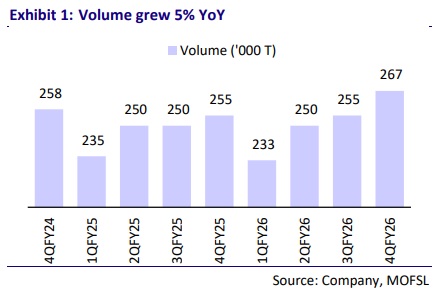

* In 4QFY26, volumes grew 5% YoY to 0.267m tons, impacted by the West Asia crisis, which led to subdued logistics activity during the quarter.

* In FY26, Revenue/EBITDA/APAT grew 2%/6%/5%.

* While 4QFY26 volumes have been muted, management expects growth to improve going ahead, driven by improvement in SME demand along with the scale-up of e-commerce shipment volumes and multimodal segments. Management is targeting volume growth of 10% in FY27, supported by demand recovery aided by an expected improvement in SME demand. We broadly retain our FY27 and FY28 estimates and expect TCIEXP to deliver a 6%/7%/11% volume/revenue/EBITDA CAGR over FY26-28. We reiterate our Neutral rating with a TP of INR520, based on 18x FY28 EPS.

Key highlights from the management commentary

* TCIE’s volumes in 4QFY26 stood at 0.267m tons (+5% YoY). Capacity utilization during 4QFY26 remained steady at 83.5%.

* The operating environment during the quarter was challenging due to geopolitical tensions and the conflict in West Asia, resulting in elevated airline fuel prices and higher logistics costs. Additionally, rising labor costs and temporary disruptions impacted business operations across select markets.

* The rise in fuel prices is unlikely to impact margins, as majority of the costs are pass-through in nature.

* The increase in labor cost has impacted margins by 100bp.

* For FY27, management has guided for 10-11% volume growth, with revenue growth of 12-15% YoY.

* Management expects a 150bp improvement in EBITDA margin in FY27, driven by cost optimization, higher automation benefits, and price hikes.

Valuation and view

* TCIEXP’s 4Q was broadly in line. We believe volume growth will gradually improve, supported by recovery in demand from the SME segment, the rising contribution of the multimodal logistics segment, and ecommerce shipment volumes.

* We largely maintain our estimates for FY27 and FY28. We expect TCIEXP to clock a 6%/7%/11% volume/revenue/EBITDA CAGR over FY26-28. We reiterate our Neutral rating with a revised TP of INR520 (based on 18x FY28 EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412