Neutral Oil India Ltd for the Target Rs 475 by Motilal Oswal Financial Services Ltd

Elevated other expenses dent 4Q performance

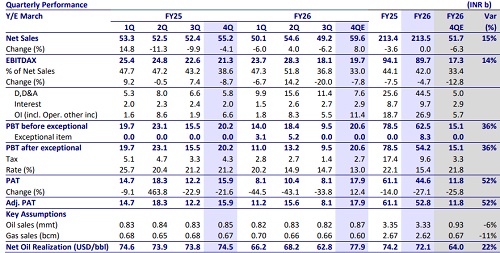

* Oil India’s (OINL) 4QFY26 revenue came in line with our estimate at INR59.6b. Oil sales came in 3% above our estimate, while gas sales were 12% below our estimate at 0.87mmt/0.6bcm. Oil production increased 6% YoY to 0.891mmt. Gas production declined 6% YoY at 0.754bcm. Oil realization was USD77.9/bbl (our estimate of USD78.4/bbl). EBITDA was 14% below our estimate at INR18.2b (-8% YoY). The miss was primarily due to a significant foreign exchange loss at INR4.9b and elevated contract costs at INR9.1b.

Exploration cost write-offs stood at INR1.5b. EBITDA adjusted for forex loss stood at INR23.1b, up 16%/76% YoY/QoQ. Reported PAT was 18% above our estimate at INR17.9b. ? Things we liked about the result:

1) Well drilling intensity remains high with 74 new wells dug in FY26 (23 wells in 4QFY26). The company aims to drill 100 wells in FY27.

2) NRL: CDU and VDU are slated to start in Jul’26. Further, 1.5mmscmd new well gas has been allocated to NRL.

* Key investor concerns:

1) Contract cost (including survey cost) rose significantly to INR9.1b (INR8.9b in 3QFY26, INR6.1b in 4QFY25). Elevated other expenses over the last three quarters have dented OINL's performance.

2) Exploration cost write-off/provisions/impairments for the year stood at INR21b (INR6.5b in FY25). With increased exploration intensity, we build in an exploration cost write-off at INR14b for FY27/28.

3) Production volumes continue to remain soft as oil/gas production was down 0.2%/2% YoY at 3.5mmt/3.2bcm in FY26. Gas production was down 6% YoY in 4QFY26. The management indicated that 0.1mmt crude oil and 0.3bcm gas production were hit by the economic blockade of 10-15 days in their areas of operations. However, the management has guided that strong production growth is expected going forward, with total volumes reaching 4mmt/ 3.35bcm crude oil/gas in FY27. Further, management expects 5bcm gas production in 18 months.

* Valuation : We reiterate our Neutral rating on the stock and arrive at our SoTP-based TP of INR475 as we model a CAGR of 3.2%/5% in oil/gas production volume over FY26-28.

Valuation and view

* In the past few quarters, OINL has struggled to raise production/sales with limited production/sales growth YoY. Further, while we like the increased exploration intensity (which is key to building a robust development pipeline), we believe this will likely be accompanied by higher dry well write-offs, which will weigh on earnings. Further, the benefits of increased new well gas proportion for OINL will be mostly offset by subdued gas realization, amid a weaker crude oil price outlook.

* The company aims to drill 100 wells by FY27. These will be the highest number of wells drilled annually in the history of OINL. The NRL refinery segment is expected to achieve 50% capacity utilization by the end of FY27, which shall gradually ramp up to 100% by the end of 2QFY28.

* We revise our SoTP-based TP to INR475 as we model a 3.2%/5% production volume growth CAGR for oil and gas production over FY26-28.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412