Neutral IEX Ltd For Target Rs.137 Motilal Oswal Financial services Ltd

Evaluating the coal exchange opportunity

* IEX's Board had granted in-principle approval in Mar'26 to explore a coal exchange, tapping into a nascent opportunity backed by the Ministry of Coal's Draft Coal Exchange Rules (published in Dec'25). Other competitors, such as NSE, have also proposed setting up a coal exchange. Assuming final rules are issued shortly, we believe the award could take place in 12–15 months, pushing the setup of the coal exchange well into FY28.

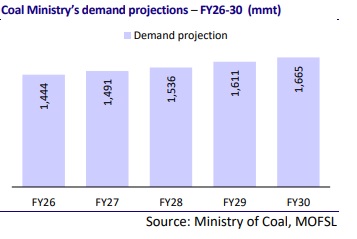

* We estimate India's coal demand at ~1.6BnT in FY28, with 10% spot market penetration. Of this, we estimate 5% of spot volumes might flow through an exchange. Assigning a 50x PE to FY28 PAT we arrive at an equity valuation of ~INR8.2b (i.e., INR6.8b when discounted back by two years at 10%) for the coal exchange opportunity.

* Currently, IEX, MCX, and BSE are trading at one-year forward P/E of 22.2x, 39.6x, and 39.8x, respectively.

* We reiterate our Neutral rating on IEX with a TP of INR137.

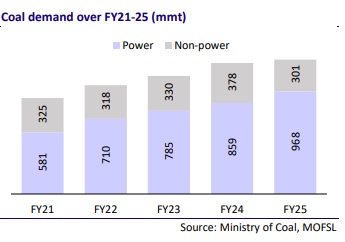

Coal demand surges 40% in five years; power utilities lead the charge

* The total coal demand in India has shown an upward trajectory over FY21- 25, rising from 0.9 BnT in FY21 to 1.3BnT in FY25, reflecting a cumulative growth of ~40% (~9% CAGR). Power utilities have largely driven this growth, as they accounted for 60-70% of the aggregate demand over the years.

* Coal imports are essential to meet ~20-25% of India’s total coal demand, especially for high-quality coking coal and high GCV coal that are domestically scarce.

* Coal India Limited (CIL) and Singareni Collieries Company Limited (SCCL) are the major producers of coal in the country.

Coal exchange: A market in the making, but miles to go

* The Ministry of Coal issued the Draft Coal Exchange Rules, 2025, on 19th Dec’25. The rules apply only to delivery-based contracts.

* As coal output rises, the market is expected to move from a supplyconstrained and deficit-coal regime towards one with a potential surplus beyond long?term fuel?supply agreements and project?linked allocations. * To manage this surplus, the sales model is expected to shift from opaque and bilateral allocations toward a more transparent and market?oriented system anchored on a national coal exchange.

* The coal exchange will aim to bring in standardized contracts defined by grade, quality, and delivery terms – enabling centralized order matching and liquid trading across multiple sellers and buyers. This will create transparent, real?time price discovery and reduce information asymmetry.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412