Metals & Mining Sector Update : Aluminium – Off the peak, not off the table by Emkay Global Financial Services Ltd

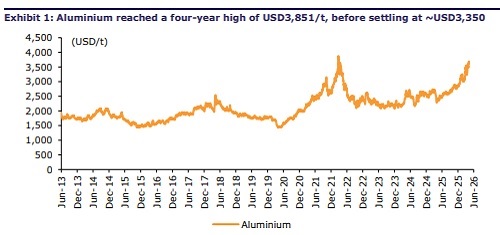

While the de-escalation of the West Asia conflict has eased near-term supply concerns, we remain constructive on aluminium (Al) as structural supply risks persist. During the conflict, nearly 9% of global Al production was exposed to disruption risks, pushing prices to a four-year high of USD3,851/t. Although this geopolitical premium is fading, we expect prices to remain supported by the risk of Chinese production curbs amid energy and emissions inspections and Guinea's proposed bauxite export controls, which could tighten raw material availability for Chinese smelters. We forecast Al to remain in the USD3,200- 3,300/t range through the remaining FY27. Despite the recent correction in Al equities, we believe the earnings outlook remains intact. HNDL remains our preferred pick, supported by resilient prices and an improving outlook for Novelis, while NACL appears fairly valued following its recent ~16% rebound.

Geopolitical premium fades, structural tightness remains

With the West Asia conflict now largely de-escalating and the proposed ceasefire agreement expected to be formalized on 19-Jun, a key overhang on global Al supply is likely to ease. At the peak of the conflict, nearly 9% of global Al production (~74mt) from the Middle East faced disruption risks due to potential blockages in the Strait of Hormuz, contributing to an estimated ~2mt supply deficit in CY26 and driving a sharp rally in prices. While geopolitical risks are receding, we expect supply tightness to persist through FY27, with disrupted smelting capacity likely requiring 6-12M to normalize. Al prices rose ~23% since the onset of the conflict, reaching four-year high of USD3,851/t before moderating to USD3,350/t (up 7.4% since 28-Feb-26). The rally was further supported by concerns over potential Chinese production curbs. We forecast an average price of USD3,325/t for CY26 and expect prices to remain elevated within the USD3,200-3,300/t range through the remaining FY27, supported by lingering supply tightness.

Emerging supply risks reinforce positive Al price outlook

While the resolution of the West Asia conflict has eased near-term supply concerns and Al prices have retreated from their recent highs, we remain constructive on the mediumterm outlook. We believe two key supply-side developments are likely to keep the market structurally tight. First, China faces an increasing risk of production curbs amid stricter energy efficiency and emissions inspections. Chinese smelters have been operating at elevated utilization levels to capitalize on the supply disruptions caused by the Middle East conflict, raising the probability of regulatory intervention. Second, Guinea's proposed bauxite export controls could tighten the upstream raw material market. The government is expected to introduce measures aimed at restricting exports, supporting domestic ore prices, and promoting downstream processing. Given that Guinea accounts for over one-third of global bauxite production and supplies nearly 75% of China's bauxite imports, any sustained restrictions could materially increase feedstock costs for Chinese alumina refiners and aluminium smelters. With China heavily reliant on imported bauxite, tighter ore availability is likely to support alumina costs and, in turn, Al prices.

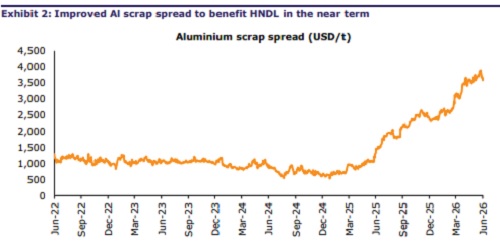

Healthy earnings outlook remains intact

Following the recent correction in aluminium prices, sector valuations have also moderated. However, we continue to believe that the structural drivers supporting aluminium prices remain intact and should sustain healthy earnings over the medium term. Accordingly, HNDL remains our preferred pick, supported by resilient aluminium prices and an improving outlook for Novelis, driven by better scrap spreads and the restart of the Oswego facility. In contrast, NACL appears fairly valued following its ~16% rebound over the past two weeks.

For More Emkay Global Financial Services Ltd Disclaimer http://www.emkayglobal.com/Uploads/disclaimer.pdf & SEBI Registration number is INH000000354

Ltd.jpg)