Markets Navigate Global Headwinds; Long-Term Outlook Remains Steady – Motilal Oswal Mutual Fund

* Nifty 50 fell by 11.31% in March 2026

* Nifty Next 50 declined by 13.43%

* Nifty Midcap 150 fell by 11.06%

* Nifty Smallcap 250 declined by 10.03%

* Nifty Microcap 250 fell by 11.29%

* Nifty 500 declined by 11.39%

According to Motilal Oswal Mutual Fund’s Global Market snapshot report, Indian equity markets witnessed broad-based selling pressure in March 2026, with all major indices ending deep in the red amid risk-off sentiment and global growth concerns.

The Nifty 50 declined 11.31% over the last one month. The index fell 14.54% over three months, 9.26% over six months, and 5.05% on a one-year basis. The Nifty Next 50 posted a monthly loss of 13.43%. The index recorded returns of -13.00% over three months, -11.05% over six months, and -4.27% over one year.

The Nifty Microcap 250 fell 11.29% over the last one month and delivered returns of -16.20% over three months, -17.45% over six months, and -8.67% over one year. The Nifty 500 recorded a monthly decline of 11.39%, while posting a fall of 14.01% over the last three months. Over a longer horizon, the index delivered returns of -9.70% over the past six months and -3.80% over the past one year.

Large caps remained weak during the month, with the Nifty 50 and Nifty Next 50 falling by 11.31% and 13.43%, respectively. Broader markets also came under pressure, as midcaps and smallcaps declined by 11.06% and 10.03%.

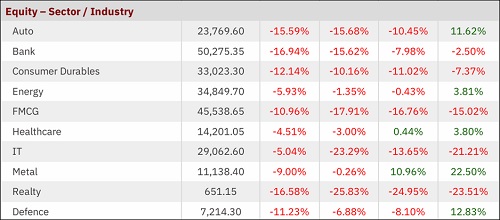

Sectorally, IT was relatively resilient with a fall of 5.04%, however over the year it has seen a 21.21% fall. Auto, Bank and Realty were the worst hit in the Month of March, declining by 15.59%, 16.94% and 16.58%, respectively. On a longer-term basis, Metals remain the standout outperformer, delivering strong gains of 22.50% over one year, supported by the global commodity cycle, while Defence and Auto also continue to show strength with returns of 12.83% & 11.62% respectively. Risk-off sentiment and global growth concerns weighed on rate-sensitive and consumption linked sectors.

Factor indices also remained under pressure. Quality fell by 8.11%, while Low Volatility, Momentum and Enhanced Value declined by 10.82%, 12.17% and 16.90%, respectively.

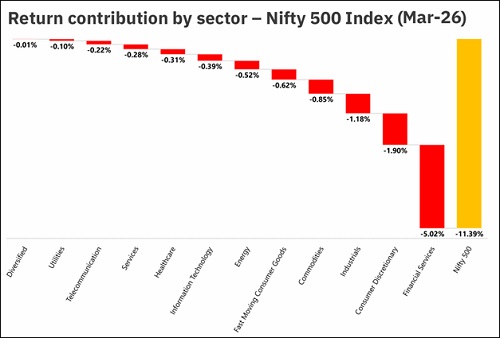

Nifty 500 declined by 11.39% in March, dragged largely by Financial Services, Consumer Discretionary and Industrials.

Nasdaq 100 and S&P 500 fell by 7.78% and 8.04%, respectively. The Dow Jones Industrial Average fell the least compared to the other major US indices.

In emerging markets, China and Brazil were the least affected. While, South Africa and Korea fell sharply by 21.09% and 20.99%, respectively.

Meanwhile, developed markets also declined, with Germany falling by 13.26%, while the UK was the least affected, declining by 8.64%. Among developed markets, the US, Japan, and European indices also remained under pressure.

Crude oil gained sharply by 53.51%, while the US dollar appreciated by 4.26%. Gold and silver, however, declined due to weaker demand expectations and heightened volatility.

Crypto markets remained relatively stable, with Bitcoin and Ethereum rising by 0.70% and 3.45%, respectively.

Quick Take

* CPI inflation edged up from 2.75% to 3.21%, indicating a modest rise in price pressures during the month.

* FII sentiment turned sharply weaker, with outflows widening to ?1,25,736 crore from inflows of ?37,804 crore earlier, while DII flows also remained in outflow territory.

* GST collections rose to ?2,00,064 crore, pointing to continued resilience in economic activity.

Above views are of the author and not of the website kindly read disclaimer