Information Technology Sector Update : FY27 off to a slow start amid uncertain tides by PL Capital

IT companies are expected to see subdued growth in Q1FY27, in an otherwise seasonally strong quarter. Leakages in traditional services and cannibalization of new revenue streams are weighing on overall revenue growth. Q1 impact is broad-based, with direct effects visible in Consumer, Hi-Tech, and Telecom. Slower decision-making and elongated sales cycle are leading to delays in revenue conversion and execution. AI-led deals contribute disproportionately to the pipeline, and come with smaller deal size and tenure, which translate into lower ACV and fragmented deal closures. We expect median revenue growth of 0.8% QoQ in CC terms and 0.4% QoQ in USD terms, implying a cross-currency headwind of ~40bps. EUR and GBP have weakened by 0.3% and 0.6% QoQ, respectively, against USD, while INR depreciated 3.4% QoQ, with the latter supporting margins in Q1.

Within Tier I, we are trimming our growth and margin estimates for most of the names (barring TECHM) for FY27E/FY28E, as operational performance is expected to be discouraging in Q1, attributed to the Middle East crisis and general slowdown due to adverse macros. As a result, we see EPS changes in the range of 0.4 to -2.7%/-0.1 to - 3.2% for FY27E/FY28E in Tier I companies. Tier II companies are likely to outpace Tier I in terms of growth in Q1. However, there are a few exceptions: EPS of LATENTVI and KPIT has been cut by 4.9%/5.0% and 17.7%/14.1% for FY27E/FY28E, respectively. We expect deal TCV to be muted sequentially, since mega deals are missing in Q1. Despite the Q1 softness, we expect INFO and HCLT to maintain their organic revenue guidance band, while HCLT is likely to deliver at the mid-range of the guidance.

Tier I & II operating performance:

We expect muted performance across both Tier I and II companies. Tier I companies are expected to report 0.4% median QoQ CC growth, led by INFO (2.4% QoQ CC growth, aided by integration of Optimum Healthcare), while WPRO and HCLT will be laggards, declining by 1.3% and 1.0% QoQ CC, respectively. Within Tier II companies, COFORGE will report consolidated growth of 22% QoQ CC with 2 months' contribution from the Encora acquisition, while organic growth is expected to be flat. PSYS will continue its growth momentum with 3.5% QoQ CC growth. Among Tier II, we expect KPIT to report weak results with 4.1% QoQ CC decline, due to persistent weakness in the automotive segment

On the margins front, we expect pressure across both Tier I and II companies, despite the INR tailwind, due to weak Q1 performance. We expect sequential margin decline across all coverage companies, except TECHM, which will continue its margin improvement trajectory with 30bps QoQ. Across our coverage universe, we expect margin movement in the band of -440bps to +30bps, with a median margin decline of 100bps QoQ in Tier I companies and 80bps QoQ in Tier II companies

Valuation and View

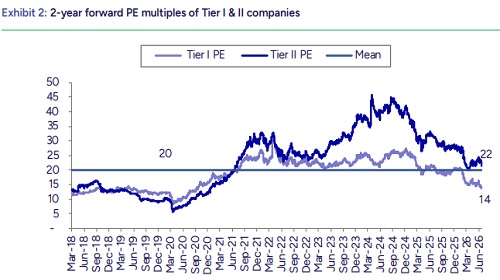

The NIFTY IT Index has been down 11.4% in the Apr-Jun quarter, taking the total drag to 31% in YTD CY26 – a decline driven by AI-led growth deceleration and now further aggravated by the Middle East conflict's impact on global enterprise tech spending. While our coverage companies carry limited direct exposure to the Middle East region, softer start to FY27 and elongated decision-making cycles will continue to weigh on revenue growth and earnings in the near term. Sharp INR depreciation should provide a partial offset, helping arrest margin pressure even as companies continue to invest in AI-led capabilities and absorb productivity pass-back to clients. We believe much of this weakness is now priced in, with 2-year forward PE multiples declining to 14x for Tier I and 22x for Tier II companies and expect a recovery from H2FY27. Despite the sharp correction, we retain our positive stance on the IT sector and continue to prefer mid-caps over large caps, given their relative resilience through recent macro headwinds and AI-led uncertainty. Within midcaps, Persistent, Mphasis and Coforge remain our top picks, trading at attractive FY26-28E PEG ratio of 1.1x each

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...