Indian Real Estate`s financial discipline spurs credit upgrades and equity market surge; ~INR 400 Bn raised via IPOs since 2021- Colliers India

India’s real estate sector has continued to exhibit marked improvement in terms of financial health in the post-pandemic era, outperforming other major industries in the economy in terms of critical credit and financial metrics. The last decade has been eventful for Indian real estate, resulting in structural changes. Events such as the Real Estate (Regulation and Development) Act (RERA), Goods and Services Tax (GST) implementation, demonetization, Non-Banking Financial Companies (NBFC) crisis and the COVID-19 pandemic have only made the sector more resilient, transparent and competitive. Particularly post the pandemic, the real estate sector has demonstrated a strong ‘V-shaped’ recovery. Overall, the financial prudence of Indian real estate is reflected in improving credit rating of companies driven by better operating & profitability margins, leverage ratios etc. In this context, we have assessed the aggregate financials of the top 50 listed real estate companies in India in terms of profitability, gearing & market performance.

Credit deployment in Indian real estate on the rise

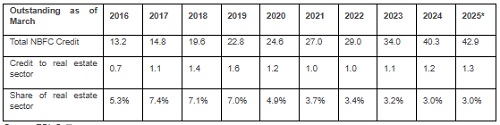

The sector’s access to credit has improved significantly in absolute terms, though with evolving dynamics amongst banks and NBFCs. While the share of banks in overall credit exposure to Indian realty has increased notably and NBFCs have become relatively averse to real estate exposure post the 2018 crisis, the outstanding loan book for both banks and NBFCs has grown significantly in the last decade.

Gross bank credit in India has grown significantly, from INR 109.5 lakh crore in FY 2021 to INR 182.4 lakh crore in FY 2025. Bank credit in the real estate sector has impressively doubled in the same period, from INR 17.8 lakh crore to INR 35.4 lakh crore. Importantly, real estate now accounts for close to one-fifth of the bank credit deployment in the country, signaling growing lender confidence in the sector.

Trends in gross bank loan book in India (in INR lakh crore)-

Trends in NBFC loan book in India (in INR lakh crore) -

In addition to increased lending to the real estate sector, the quality of loans has also improved significantly. The proportion of Gross Non-Performing Assets (GNPA) in the construction industry loan book of banks has significantly reduced from 23.5% in March 2021 to 3.1% in March 2025.

“Indian real estate sector continues to demonstrate resilience and financial prudence even in the wake of external volatilities. In fact, the strong financial health of the sector is demonstrated by significantly higher proportion of credit rating upgrades during FY 2025 as compared to upward revisions in other economic sectors. The relatively higher credit quality of real estate loans is well supported by underlying strong demand-supply dynamics across multiple asset classes such as residential, commercial, industrial & warehousing, retail, hospitality etc. Looking ahead, the overall outlook for Indian real estate remains positive in the near-mid-term amidst sustained global as well as domestic investor confidence,” said Badal Yagnik, Chief Executive Officer, Colliers India.

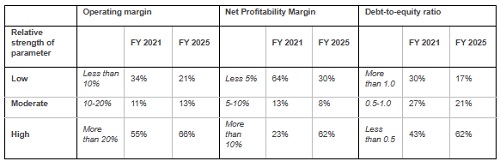

Profitability and leverage ratios improve for most of the larger real estate players

Increasing appetite for real estate lending by financial institutions has primarily stemmed from the financial prudence displayed by the sector. In fact, the top 50 listed real estate companies have shown impressive improvements in terms of profitability, cash flow realization, and balance sheet performance over the last five years. One of the most significant trends is the improvement in profitability metrics – 62% of the top 50 listed real estate companies had higher profitability margins at the end of FY 2025 as compared to the 23% share in FY 2021. Consistent strong demand, higher revenue realization, and better operating efficiencies can be attributed to the increasing profitability of real estate companies.

Additionally, the debt-to-equity ratio, a critical indicator of financial discipline, has shown consistent improvement over the past five years. More than 60% of the leading real estate companies in India have comfortable debt levels, which is reflected in the debt-to-equity ratio of less than 0.5 in FY 2025. This is particularly noteworthy considering that 43% of the leading real estate companies were low-leverage companies in FY 2021. Financial prudence at the Special Purpose Vehicle (SPV) level has in a way culminated into comfortable debt levels at the consolidated level. Moreover, it highlights a deliberate strategy amongst large developers to deleverage and enhance capital as well as operational efficiency.

Comparison of key financial ratios for the top 50 listed real estate players in India (FY 2025 vs FY 2021)

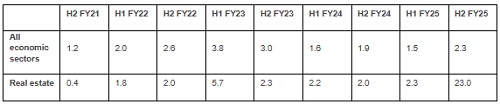

Creditworthiness of the real estate sector reflected in a significantly higher number of rating upgrades

Most economic sectors in India have rebounded strongly post-pandemic. However, the pace and extent of recovery in the real estate sector has been comparatively more pronounced than in other industries. This is reiterated by a higher proportion of credit rating upgrades in Indian real estate in recent years. In fact, the real estate sector has outperformed the broader industry on credit quality metrics, with a leading Credit Rating Agency (CRA) reporting 23% of upgrades in its rated real estate portfolio versus a mere 1% of downgrades during the second half of FY 2025. The percentage of rating upgrades and downgrades across industries from the same CRA meanwhile stood at 14% and 6% respectively in the same period.

While the extremely high number of upgrades vis-à-vis downgrades in H2 of FY 2025 in Indian real estate may rationalize over the next few years, it is still expected to outperform most economic sectors, driven by its inherent fundamentals. Rising revenues, improving operating and profitability margins, and steady debt deleveraging underscore the adoption of more sustainable and disciplined financial practices in Indian real estate, reinforcing its position as one of the promising sectors across the corporate landscape.

Credit ratio (rating upgrades/rating downgrades) trend in Indian real estate

Real estate companies increasingly access equity markets to fuel expansion

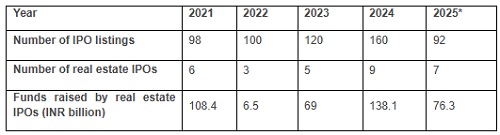

Real estate players are increasingly turning to public markets to raise capital, as reflected in the surge of Initial Public Offerings (IPO) in recent years. In 2024 alone, India witnessed close to 160 fresh public issuances across sectors, comfortably outpacing issuances in 2023. Remarkably, the real estate sector saw 9 IPOs in 2024, raising nearly INR 138 billion - almost double the amount raised in the previous year. Since 2021, 30 IPOs have collectively raised close to INR 400 billion into India’s real estate sector. Heightened activity in the equity markets has continued into 2025 as well. The year has already seen 92 IPOs, including 7 real estate IPOs till date. Interestingly, real estate IPOs are expanding into newer categories such as flex spaces, with leading operators scaling their portfolios across cities and fast-tracking their public listing plans. Moreover, the introduction of REIT and SM-REIT offerings is democratizing real estate ownership for the retail investor. In the near to mid-term, several real estate companies, including Real Estate Investment Trusts (REITs), Small & Medium (SM)-REITs, hospitality players, residential developers, flex space operators etc. are lining up for their IPOs with the regulator.

IPO trends: Heightened activity in recent years

“Real estate players are increasingly tapping public markets to fuel their expansion and strengthen balance sheets, signaling growing investor confidence in the sector. The strong momentum seen in 2024 has carried into 2025, with seven real estate IPOs, raising more than INR 76 billion till July. Moreover, the diverse listings across segments such as flex spaces, hospitality, office, residential, etc., and the anticipated upswing in SM REIT and REIT activity is promising for the entire real estate sector. Indian real estate continues to draw strength from long-term stability and growing investor confidence, making it less vulnerable to global uncertainties,” said Vimal Nadar, National Director and Head of Research, Colliers India.

Looking ahead, the outlook remains particularly positive for residential and commercial real estate, led by strong end-user demand, favorable demographics, rising disposable income, and relatively lower interest rates.

However, real estate developers and investors must remain cautious of potential risks, including interest rate fluctuations, urban land acquisition bottlenecks, and global economic headwinds that could moderate real estate growth.

Above views are of the author and not of the website kindly read disclaimer