India `s Alternatives AUM expected to reach USD 276B by 2030 - CareEdge Ratings

Synopsis

Over the past decade, Indian Alternatives Industry’s Asset Under Management (AUM) has more than doubled to USD 152 billion in Dec25. It is expected to achieve strong growth momentum to reach ~USD 276 billion the end of 2030, backed by growing domestic investor base, enabling regulatory framework, portfolio diversification and attractive risk-return proposition for investors.

* India is underpenetrated with Alternatives AUM accounting for ~4% of GDP, as compared to mature global markets with Alternatives AUM at more than 10% of GDP, indicating a strong potential upside.

* With healthy economic growth and increasing financialisation of assets, India’s HNI population is expected to more than double by 2027 as compared to 2022. The rising affluent population and accumulating domestic wealth would support growth in differentiated investment products such as AIFs. Domestic investors capital is gradually diversifying into Alternatives, accounting for ~66% of total amount raised in Dec25.

India’s Alternatives Investment: A Decade of Transformation and Opportunity

Over the past decade, India’s Alternatives industry has emerged as an attractive investment avenue registering strong growth and rising investor preference over traditional assets.

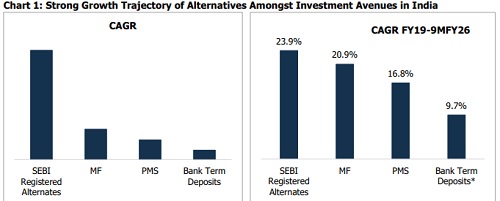

Low Alternatives Penetration in India Indicate Good Growth Potential

India is projected to be the third largest economy globally by the year 2028, making it an attractive opportunity for investors. Despite strong growth, India remains significantly underpenetrated in the Alternatives space. Alternatives AUM currently represents only about 4% of the country’s GDP as compared to over 10% in mature global markets such as the United States, Europe and parts of Asia. This gap highlights the immense potential for alternative assets to scale in India, especially as the wealth base and capital market depth continue to expand.

Alternatives Industry: Gaining Ground in a High-Growth Indian Economy

The Indian alternative industry is expected to reach ~USD 276 bn by the year 2030 from USD 152 bn in Dec25. Between 2025 and 2030, the industry is expected to record a CAGR of ~11% to 14%, where India is expected to outpace the mature market like North America and Europe. The AIF segment in India is growing quickly because of increasing awareness of alternative investments, evolution of regulatory environment, investors looking beyond traditional asset classes for investment option, improving financial literacy and growing high net worth population in the country.

As India's economy and wealth increase, investors are looking for more diverse and higher-yielding options than usual, also these investments are not linked to market fluctuations thereby a preferred choice to diversify, leading to a rise in demand for alternative investments like private credit and real assets. The support from SEBI and positive government policies have made the environment for these funds transparent and well governed. Hence, established players are well placed to take advantage of this growth.

Rising allocations toward private credit in the Indian alternatives market reflect investors’ increasing preference within alternative assets for more predictable cash flows, downside protection, and relatively shorter investment horizons compared to private equity. Private credit investments typically offer structured payouts, priority in the capital structure, and lower sensitivity to valuation cycles, making them attractive during periods of market uncertainty.

In contrast, private equity, also a core segment of alternatives, depends more heavily on exit timing and equity market conditions, which can result in longer lock-in periods and greater return variability. At the same time, strong demand for flexible financing from mid-market Indian companies, tightening bank lending standards, and the need for alternative debt capital have expanded opportunities in private credit. As a result, investors are gradually increasing allocations to private credit within India’s alternatives industry to balance portfolios with stable income generation, improved risk-adjusted returns, and enhanced capital preservation.

Domestic Investors Rising Participation in AIFs in India

The share of domestic investors in India’s alternatives ecosystem has increased steadily from 59.1% in Mar24 to 62.1% in Dec24, and further to 66.2% in Dec25, highlighting the growing role of local capital in the market. Correspondingly, the share of foreign capital declined from 40.9% in Mar24 to 37.9% in Dec24 and to 33.8% in Dec25. However, despite this decline in proportion, the absolute value of foreign investor inflows continued to grow, increasing by 20% Year-on-Year, and recording a further 14.6% Year-on-Year growth between Dec24 and Dec25. This indicates sustained foreign investor interest in India, even as domestic participation expands at a faster pace.

India’s high-net-worth (HNI) and ultra-high-net-worth (UHNI) population has been expanding rapidly, fuelled by economic liberalisation, startup wealth creation and intergenerational transfers. The HNI base, expected to more than double between 2022 and 2027, is increasingly seeking sophisticated investment options that go beyond traditional instruments like mutual funds or fixed deposits. Alternatives investments are fulfilling this need by offering diversified exposure, tailored strategies, and access to high-growth sectors.

Exponential Growth in AIFs in India

Over the past decade, Indian Alternatives industry has registered growth of more than 50 times in terms of funds raised on account of various factors - evolution of regulatory framework, increasing participation from family offices, insurance companies, sovereign funds, foreign funds inflow, growing wealth of HNIs and UHNIs, investors’ preference for diversification beyond traditional asset classes, sectoral diversification and innovative investment solutions.

AIF Investment Trends – Key Sectors

Based on the category of AIFs, the funds deploy different strategies such as funding growth stage companies, start-ups, equity investments in listed and unlisted companies, debt solutions, hedging strategies, etc. Further, key growth sectors attracting AIF capital include Fintech, Healthtech, Renewable Energy, Financial Services, Real Estate, and IT/ITeS. Investment trends show a healthy mix of legacy sectors like Real Estate and BFSI, alongside future-facing bets in IT, pharmaceutical, and renewable energy.

Global Headwinds and Near-Term Uncertainty for India’s Alternatives Industry

Some of the global private credit funds have recently imposed redemption limits amid rising withdrawal requests, highlighting liquidity risks in semi-liquid structures. While such developments raise concerns, the spillover to India is likely to be limited, as most Indian private credit vehicles operate as closed-ended Category II AIFs with lockedin capital, reducing redemption pressure. However, indirect effects could emerge through cautious global investor sentiment and tighter fundraising conditions, underscoring the importance of credit discipline, transparency, and prudent portfolio construction in India’s growing private credit market.

The West Asia conflict may create short-term uncertainty for India’s alternatives industry by slowing foreign capital inflows and impacting valuations through oil price volatility, inflation, and interest rate movements. However, rising domestic participation and new opportunities in infrastructure, renewables, and domestic manufacturing could offset these pressures, supporting the industry’s medium-term growth

Conclusion

India’s Alternative Investment Fund ecosystem is entering a more mature and structurally resilient phase, supported by strong domestic participation, growing investor sophistication, and disciplined capital deployment. The evolution from rapid expansion to selective allocation reflects a healthier investment environment where performance, governance, and sector expertise are becoming central to capital flows. This shift is strengthening the foundation of the alternatives industry and enhancing its role in supporting innovation, enterprise growth, and long-term value creation within the Indian economy.

With low penetration relative to global markets, expanding investor awareness, and increasing sectoral opportunities, AIFs are well positioned to remain a key component of India’s evolving investment landscape. The combination of scale, agility across fund sizes, and rising thematic strategies suggests that alternatives will continue to gain prominence as investors seek diversification and superior risk-adjusted returns. Overall, the trajectory indicates sustained momentum, reinforcing the role of AIFs as an important channel for channelling capital into high-growth sectors of the economy.

“India’s alternatives industry is poised for a transformative decade, with Alternates AUM expected to nearly double by 2030 to ~USD 276 billion,” says Tanvi Shah, Senior Director at CareEdge Advisory & Research, highlighting the strong long-term growth outlook for the segment.

Above views are of the author and not of the website kindly read disclaimer

More News

Economy : Financing Fragility Over Real Fixes by Choice Institutional Equities Ltd