ICICI Bank Q2 FY26 results

Performance Review: Quarter ended September 30, 2025

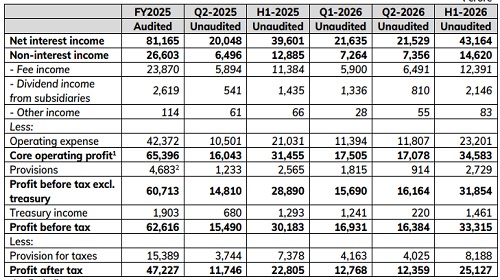

* Profit before tax excluding treasury grew by 9.1% year-on-year to Rs.16,164 crore (US$ 1.8 billion) in the quarter ended September 30, 2025 (Q2-2026)

* Core operating profit grew by 6.5% year-on-year to Rs.17,078 crore (US$ 1.9 billion) in Q2-2026

* Profit after tax grew by 5.2% year-on-year to Rs.12,359 crore (US$ 1.4 billion) in Q2-2026

* Average deposits grew by 9.1% year-on-year to Rs.15,57,449 crore (US$ 175.4 billion) in Q2-2026

* Average current account and savings account (CASA) ratio was 39.2% in Q2- 2026

* Total period-end deposits grew by 7.7% year-on-year to Rs.16,12,825 crore (US$ 181.6 billion) at September 30, 2025

* Domestic loan portfolio grew by 10.6% year-on-year to Rs.13,75,260 crore (US$ 154.9 billion) at September 30, 2025

* Net NPA ratio was 0.39% at September 30, 2025

* Including profits for the six months ended September 30, 2025 (H1-2026), total capital adequacy ratio was 17.00% and CET-1 ratio was 16.35%, on a standalone basis, at September 30, 2025

The Board of Directors of ICICI Bank Limited (NSE: ICICIBANK, BSE: 532174, NYSE: IBN) at its meeting held at Mumbai today, approved the standalone and consolidated accounts of the Bank for the quarter ended September 30, 2025 (Q2-2026). The statutory auditors have conducted a limited review and have issued an unmodified report on the standalone and consolidated financial statements for the quarter ended September 30, 2025

Profit & loss account

* Profit before tax excluding treasury grew by 9.1% year-on-year to Rs.16,164 crore (US$ 1.8 billion) in Q2-2026 from Rs.14,810 crore (US$ 1.7 billion) in the quarter ended September 30, 2024 (Q2-2025)

* Core operating profit grew by 6.5% year-on-year to Rs.17,078 crore (US$ 1.9 billion) in Q2-2026 from Rs.16,043 crore (US$ 1.8 billion) in Q2-2025

* Net interest income (NII) increased by 7.4% year-on-year to Rs.21,529 crore (US$ 2.4 billion) in Q2-2026 from Rs.20,048 crore (US$ 2.3 billion) in Q2-2025. Net interest margin was 4.30% in Q2-2026

* Non-interest income, excluding treasury, increased by 13.2% year-on-year to Rs.7,356 crore (US$ 828 million) in Q2-2026 from Rs.6,496 crore (US$ 732 million) in Q2-2025

* Fee income grew by 10.1% year-on-year to Rs.6,491 crore (US$ 731 million) in Q2- 2026 from Rs.5,894 crore (US$ 664 million) in Q2-2025. Fees from retail, rural and business banking customers constituted about 78% of total fees in Q2-2026

* Treasury income was Rs.220 crore (US$ 25 million) in Q2-2026 as compared to Rs.680 crore (US$ 77 million) in Q2-2025

* Provisions (excluding provision for tax) were Rs.914 crore (US$ 103 million) in Q2-2026 compared to Rs.1,233 crore (US$ 139 million) in Q2-2025 and Rs.1,815 crore (US$ 204 million) in Q1-2026 • Profit before tax grew by 5.8% year-on-year to Rs.16,384 crore (US$ 1.8 billion) in Q2- 2026 from Rs.15,490 crore (US$ 1.7 billion) in Q2-2025

* Profit after tax grew by 5.2% year-on-year to Rs.12,359 crore (US$ 1.4 billion) in Q2- 2026 from Rs.11,746 crore (US$ 1.3 billion) in Q2-2025

Credit growth

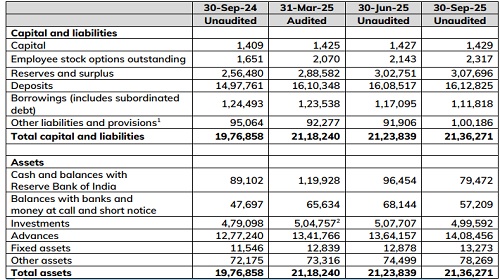

The net domestic advances grew by 10.6% year-on-year and 3.3% sequentially at September 30, 2025. The retail loan portfolio grew by 6.6% year-on-year and 2.6% sequentially, and comprised 52.1% of the total loan portfolio at September 30, 2025. Including non-fund outstanding, the retail portfolio was 42.9% of the total portfolio at September 30, 2025. The business banking portfolio grew by 24.8% year-on-year and 6.5% sequentially at September 30, 2025. The rural portfolio declined by 1.3% year-onyear and grew by 0.8% sequentially at September 30, 2025. The domestic corporate portfolio grew by 3.5% year-on-year and 1.0% sequentially at September 30, 2025. Total advances increased by 10.3% year-on-year and 3.2% sequentially to Rs.14,08,456 crore (US$ 158.6 billion) at September 30, 2025.

Deposit growth

Average deposits increased by 9.1% year-on-year and 1.6% sequentially to Rs.15,57,449 crore (US$ 175.4 billion) in Q2-2026. Average current account deposits increased by 12.6% year-on-year and 1.6% sequentially in Q2-2026. Average savings account deposits increased by 8.5% year-on-year and 3.2% sequentially in Q2-2026. Total periodend deposits increased by 7.7% year-on-year to Rs.16,12,825 crore (US$ 181.6 billion) at September 30, 2025 (Rs.16,08,517 crore (US$ 181.2 billion) at June 30, 2025).

With the addition of 263 branches during H1-2026, the Bank had a network of 7,246 branches and 10,610 ATMs & cash recycling machines at September 30, 2025.

Asset quality

The gross NPA ratio was 1.58% at September 30, 2025 compared to 1.67% at June 30, 2025 and 1.97% at September 30, 2024. The net NPA ratio was 0.39% at September 30, 2025 compared to 0.41% at June 30, 2025 and 0.42% at September 30, 2024. The gross NPA additions were Rs.5,034 crore (US$ 567 million) in Q2-2026 compared to Rs.6,245 crore (US$ 703 million) in Q1-2026 and Rs. 5,073 crore (US$ 571 million) in Q2-2025. Recoveries and upgrades of NPAs, excluding write-offs and sale, were Rs.3,648 crore (US$ 411 million) in Q2-2026 compared to Rs.3,211 crore (US$ 362 million) in Q1-2026 and ? 3,319 crore (US$ 374 million) in Q2-2025. The net additions to gross NPAs, excluding write-offs and sale, were Rs.1,386 crore (US$ 156 million) in Q2-2026 compared to Rs.3,034 crore (US$ 342 million) in Q1-2026 and Rs.1,754 crore (US$ 198 million) in Q2-2025. The Bank has written-off gross NPAs amounting to Rs.2,263 crore (US$ 255 million) in Q2- 2026. The provisioning coverage ratio on non-performing loans was 75.0% at September 30, 2025

Excluding NPAs, the total fund based outstanding to all borrowers under resolution as per the various extant regulations/guidelines declined to Rs.1,624 crore (US$ 183 million) or about 0.1% of total advances at September 30, 2025 compared to Rs.1,788 crore (US$ 201 million) at June 30, 2025 and Rs.2,546 crore (US$ 287 million) at September 30, 2024.

The loan and non-fund based outstanding to performing corporate borrowers rated BB and below was Rs.3,661 crore (US$ 412 million) at September 30, 2025 compared to Rs.2,995 crore (US$ 337 million) at June 30, 2025 and Rs.3,386 crore (US$ 381 million) at September 30, 2024. The increase during the quarter was due to upgrade of certain borrowers having non-fund outstanding from non-performing to performing status.

At September 30, 2025, the Bank holds total provisions, other than specific provisions on fund-based outstanding to borrowers classified as non-performing, amounting to Rs.22,620 crore (US$ 2.5 billion) or 1.6% of loans. These provisions include the contingency provisions of Rs.13,100 crore (US$ 1.5 billion) as well as general provision on standard assets, provisions held for non-fund based outstanding to borrowers classified as nonperforming, loan and non-fund based outstanding to standard borrowers under resolution and the BB and below portfolio.

Capital adequacy

Including profits for the six months ended September 30, 2025 (H1-2026), the Bank’s total capital adequacy ratio at September 30, 2025 was 17.00% and CET-1 ratio was 16.35% compared to the minimum regulatory requirements of 11.70% and 8.20% respectively.

Consolidated results

The consolidated profit after tax increased by 3.2% year-on-year to Rs.13,357 crore (US$ 1.5 billion) in Q2-2026 from Rs.12,948 crore (US$ 1.5 billion) in Q2-2025.

Consolidated assets grew by 6.8% year-on-year to Rs.26,86,485 crore (US$ 302.6 billion) at September 30, 2025 from Rs.25,16,512 crore (US$ 283.4 billion) at September 30, 2024

Key subsidiaries

The annualised premium equivalent of ICICI Prudential Life Insurance (ICICI Life) was Rs.4,286 crore (US$ 483 million) in H1-2026 compared to Rs.4,467 crore (US$ 503 million) in H1-2025. Value of New Business (VNB) of ICICI Life was Rs.1,049 crore (US$ 118 million) in H1-2026 compared to Rs.1,058 crore (US$ 119 million) in H1-2025. The VNB margin was 24.5% in H1-2026 compared to 22.8% in FY2025 and 23.7% in H1-2025. The profit after tax increased to Rs.299 crore (US$ 34 million) in Q2-2026 from Rs.252 crore (US$ 28 million) in Q2-2025.

The Gross Direct Premium Income (GDPI) of ICICI Lombard General Insurance Company (ICICI General) was Rs.6,596 crore (US$ 743 million) in Q2-2026 compared to Rs.6,721 crore (US$ 757 million) in Q2-2025. The combined ratio stood at 105.1% in Q2-2026 compared to 104.5% in Q2-2025. Excluding the impact of CAT losses of Rs.73 crore (US$ 8 million) in Q2-2026 and Rs.94 crore (US$ 11 million) in Q2-2025, the combined ratio was 103.8% and 102.6% respectively. The profit after tax of ICICI General grew by 18.1% to Rs.820 crore (US$ 92 million) in Q2-2026 compared to Rs.694 crore (US$ 78 million) in Q2-2025. With effect from October 1, 2024, long-term products are accounted on 1/n basis, as mandated by IRDAI, hence Q2-2026 numbers are not fully comparable with prior periods.

The profit after tax of ICICI Prudential Asset Management Company, as per Ind AS, was Rs.835 crore (US$ 94 million) in Q2-2026 compared to Rs.694 crore (US$ 78 million) in Q2- 2025.

The profit after tax of ICICI Securities, on a consolidated basis, as per Ind AS, was Rs.425 crore (US$ 48 million) in Q2-2026 compared to Rs.529 crore (US$ 60 million) in Q2-2025

The profit after tax of ICICI Home Finance, as per Ind AS, was Rs.203 crore (US$ 23 million) in Q2-2026 compared to Rs.183 crore (US$ 21 million) in Q2-2025

Summary Profit and Loss Statement (as per standalone Indian GAAP accounts)

1. Excluding treasury

2. The Bank, on a prudent basis, continues to hold provision against the security receipts guaranteed by the Government, which will be reversed on actual receipt of recoveries or approval of claims, if any.

3. Prior period numbers have been re-arranged wherever necessary

Summary balance sheet

1. The Bank continues to hold contingency provision of Rs.13,100 crore (US$ 1.5 billion) at September 30, 2025

2. Pursuant to the Scheme of Arrangement amongst ICICI Bank Limited and ICICI Securities Limited and their respective shareholders, ICICI Securities Limited has been delisted from stock exchanges on March 24, 2025 and became a wholly-owned subsidiary of the Bank.

3. Prior period figures have been re-grouped/re-arranged wherever necessary

Above views are of the author and not of the website kindly read disclaimer

.jpg)