Hold Tata Elxsi Ltd for the Target Rs. 4,800 By Prabhudas Lilladher Ltd

Growth under pressure, Recovery timeline uncertain

Quick Pointers

* Mixed qtr. with rev. below est. but strong margin expansion

* Expect high single digit revenue growth in Transportation in FY27

The revenue performance (+0.9% QoQ CC) was below our estimates (+1.2% QoQ CC), attributed to delayed deal closures within Healthcare vertical, down 13.7% QoQ. Media and Communications supported the overall growth, while Transportation growth was muted sequentially. The overall OEM mix (~77% of revenue) is improving within Transportation, which should drive a steady state going forward, although it anticipates Transportation to grow high-single digit in FY27E. We believe the underlying spending pattern within M&C and H&L is sporadic and require couple of more quarters to derive predictable growth within these verticals. Near-term M&C performance is largely benefiting from a planned execution of large deal, otherwise the ground reality remains weak due to consolidation and M&A activities within the space. On margin, it exceeded our estimate by 120bps QoQ, attributed to improving utilization (at ~73% in Q3), it aspires to achieve 80% utilization with a combination of deploying automation and AI. Additionally, we believe the decoupling of revenue growth and talent hiring would provide incremental margins levers. We expect CC revenue growth of 6.0%/10.0% YoY (8.4%/11.4% earlier) in FY27E/FY28E. We are assigning 30x PE to FY28 EPS, translating a TP of INR 4,800. Downgrade to HOLD (BUY earlier).

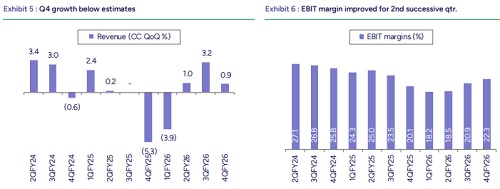

Revenue: TELX reported muted growth of 0.9% QoQ CC in Q4. Growth was subdued as the 5.6% QoQ CC increase in Media & Comms. was offset by flattish performance in Transportation and a sharp 13.1% QoQ CC decline in Healthcare & Life Sciences. Geographically, all regions except the Americas grew sequentially. For FY26, TELX revenue declined by 5.5% YoY CC, driven by weakness across key segments of Transportation (-3.3%), Media & Comms. (-7%), and Healthcare & Life Sciences (-15%).

Operating Margin: Margin improvement continued for the second consecutive quarter, with EBIT margin expanding by 140 bps QoQ, following a 240 bps improvement in Q3. Margins improved despite a ~90 bps headwind from wage hikes (wef from Jan. 1), supported by tailwinds from INR depreciation (~155 bps), operational efficiencies (~65 bps), and improved utilization. For FY26, the company reported an adjusted EBIT margin of ~20%, down 330 bps YoY.

Hiring & Utilization: Net headcount declined by 54 in Q4, marking the fifth consecutive quarter of decline, taking total employee strength to ~11.5k. Utilization improved to ~77% during the quarter (vs. ~73% in Q3), and management expects it to increase further to 80–82%, providing a tailwind to margins in FY27E. For FY26, the company’s net headcount declined by 874.

Please refer disclaimer at Report

SEBI Registration number is INH000000933

600-400.jpg)