Daily Derivatives Report 23rd February 2026 by Axis Securities Ltd

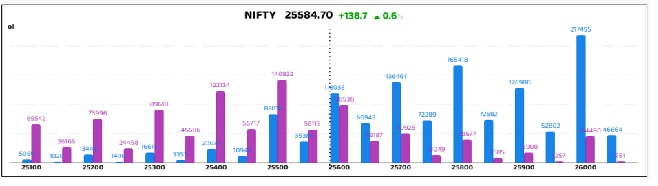

Nifty

The Day That Was:

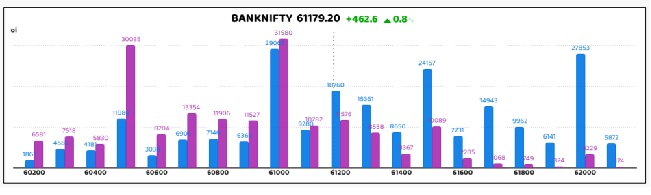

Nifty Futures: 25,584.7 (0.5%), Bank Nifty Futures: 61,179.2 (0.8%).

Nifty Futures climbed 138.7 points as Open Interest (OI) expanded by 2.85 lakh shares to 185.38 lakh, confirming a Long Build-up as the index swung from a discount to a 13-point premium. This bullish momentum was mirrored in Bank Nifty Futures, which surged 462.6 points with an OI addition of 0.32 lakh shares (reaching 18.11 lakh), signalling a structural shift into positive territory as its premium recovered to 7 points from a previous discount of 23. While prices trended toward intraday peaks, late-session profit-shaving moderated the final gains, though the underlying strength was validated by a robust HSBC Composite PMI of 59.3, fuelled by manufacturing resilience at 57.5. Metal, PSU Banking, and FMCG counters spearheaded the recovery through value hunting, contrasting with the turbulence in IT and Media as US interest-rate ambiguity weighed on growth stocks. However, the 6.70% spike in India VIX to 14.36 and the USD-INR pair’s 31-paise jump to 90.99 driven by safe-haven dollar demand underscore a fragile market floor. Consequently, while internal demand remains a potent catalyst, the surge in volatility and currency depreciation suggests that participants should maintain a defensive posture against lingering external shocks.

Global Movers:

Wall Street orchestrated a massive intraday reversal on Friday, as a high-velocity session defined by a paradoxical "judicial relief" rally saw the Supreme Court strike down the administration's sweeping tariff regime, sparking a defiant risk-on rotation that propelled the Dow Jones, gains +231 points (+0.5%), 49,626, the S&P 500, gains +48 points (+0.7%), 6,910, and the tech-heavy Nasdaq, gains +203 points (+0.9%), 22,886 into the green. This regulatory reprieve effectively neutralized a "stagflationary cocktail" of disappointing Q4 GDP growth (1.4%) and a firmer-than-expected Core PCE (0.4% MoM), though it fuelled a yield-curve steepening with the US 10-Year Yield, gains +2 bps (+0.6%), 4.08% rising as traders priced in a more complex Fed path. In the commodities pits, a "safe-haven overdrive" saw Gold, gains +121 points (+2.4%), 5,118 and Silver, gains +6.7 points (+8.6%), 84 explode through key psychological barriers, while Brent Crude, loss -0.2 points (-0.3%), 71 remained trapped in a contango structure, as the demand-side drag of weak GDP offset the geopolitical risk premium of U.S.-Iran frictions.

Stock Futures:

RVNL: Shares surged 5.2% as a strategic alliance with Texmaco and a Rs 1,201 Cr Northern Railway mandate triggered a sharp Short Covering phase. Open interest contracted 5.9%, with 2,825 futures contracts liquidated as the basis improved by 2.45 points. Despite heavy call concentration of 31,591 contracts, a reduction of 6,991 units suggests tactical unwinding. The PCR's ascent to 0.43 reflects a gradual shift in sentiment toward this resilient execution pipeline.

ABB: Investors disregarded profit compression to drive a 4.9% price gain, fueled by a 52% YoY order book expansion. This Long Addition saw open interest swell by 19.7% with 3,470 new contracts, flipping the basis from a discount to a 36.5-point premium. While 7,454 call options were added, nearly identical put writing of 7,575 contracts lifted the PCR to 0.79. The magnitude of new positioning confirms institutional conviction in ABB’s long-term electrification trajectory.

BDL: The Rafale co-production tailwind catalyzed a 3.2% rally, prompting Short Covering as open interest shed 14.5% (2,978 contracts). The futures discount widened slightly to 17.3 points, yet a subtle 650-contract addition in puts versus a 184-contract drop in calls nudged the PCR higher to 0.50. This interplay suggests that while the basis remains soft, the velocity of short liquidation indicates a structural neutralization of previous bearish pressure in the defence segment.

KEI: A high-voltage breakout propelled KEI 4% higher to record peaks, driven by a Rs 25,000 Cr data-centre opportunity. Short Covering dominated the flow as open interest contracted 8.5%, while the futures discount deepened significantly by 40.8 points to 56.3. Options activity remained skewed toward protection, with 423 puts added against 272 calls, maintaining a robust PCR of 1.35. The price-to-basis divergence highlights an aggressive scramble for liquidity amidst an accelerating supply-demand imbalance.

Put-Call Ratio Snapshot:

The Nifty put-call ratio (PCR) rose to 0.98 from 0.7 points, while the Bank Nifty PCR rose from 0.98 to 1.09 points.

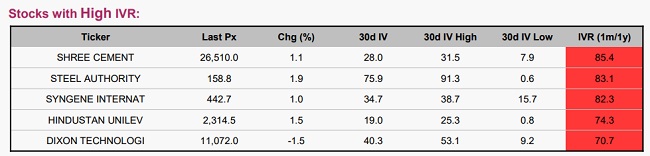

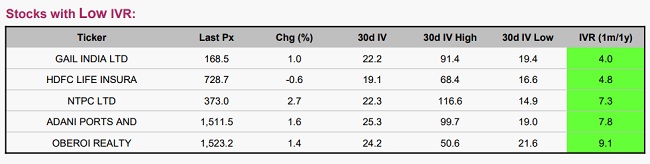

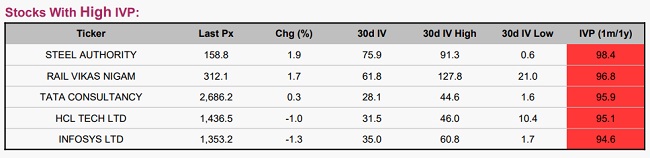

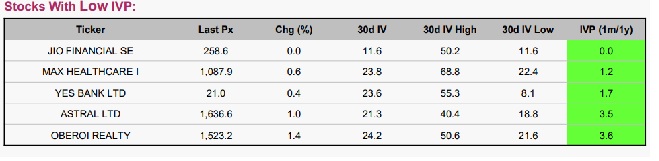

Implied Volatility (IV):

SHREE CEMENT (26,510.00, +1.1%) and STEEL AUTHORITY (158.8, +1.9%) have pushed their Implied Volatility Ranks to 85.4 and 83.1 respectively; this peak pricing creates a structural advantage for premium sellers as the market prepares for a shift from wide-range turbulence to sideways stability. In contrast, the energy and insurance segments, represented by GAIL INDIA LTD (168.5, +1%) and HDFC LIFE INSURA (728.7, -0.6%), are operating at the floor of their annual volatility cycles with IVRs of 4 and 4.8. These low-rank environments suggest that despite minor daily price fluctuations, the "volatility engine" is dormant, favouring a disciplined wait-and-watch approach as both tickers remain locked in narrow consolidation.

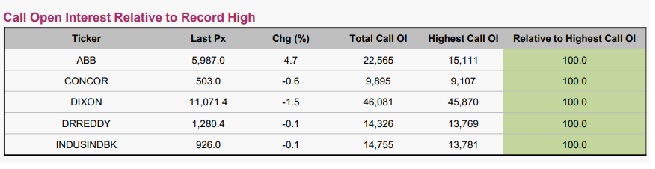

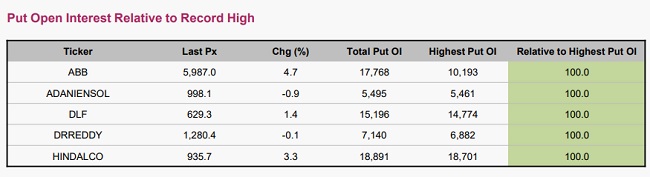

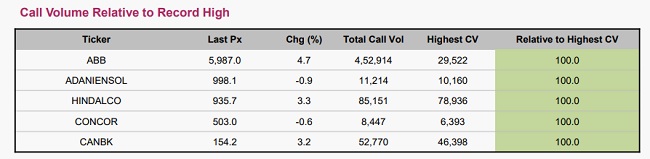

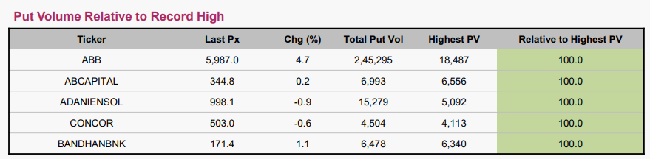

Options volume and Open Interest highlights:

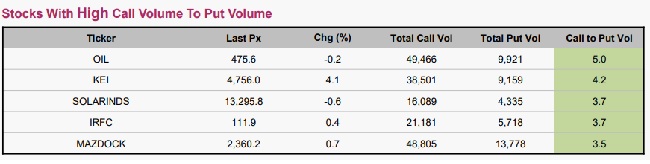

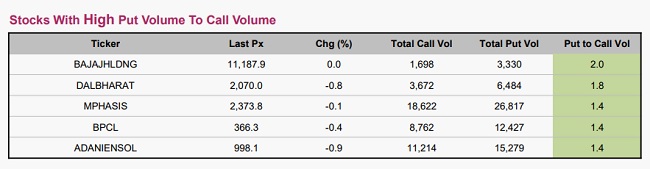

Oil India Limited and Mazagon Dock Shipbuilders Limited continue to display strong upward price momentum, supported by heavily skewed call-to-put ratios of roughly 5:1 and 4:1. Such extreme positioning reflects crowded bullish bets in the derivatives market and materially elevates the risk of near-term profit-taking or a positioning-led pullback. By contrast, Mphasis Limited and Adani Energy Solutions Limited remain constrained by subdued to negative sentiment. However, emerging signs of seller fatigue suggest that downside momentum may be waning, creating conditions conducive to a tactical mean-reversion bounce. At the broader market level, volatility appears poised to rise as overstretched derivatives positions begin to unwind. This dynamic is underscored by concentrated call accumulation in IndusInd Bank Limited and Dixon Technologies (India) Limited, sizeable two-way build-ups in ABB India Limited, and elevated put positioning in DLF Limited and Hindalco Industries Limited nearing annual highs. Collectively, these signals point to a market entering a more reactive and potentially turbulent phase. (This data covers only stock options with at least 500 contracts traded on the day for both calls and puts).

Participant-wise Open Interest Net Activity:

Index Futures witnessed a sharp exodus by retail clients, who liquidated 13,693 contracts, effectively offsetting a broad-based accumulation by institutional and professional desks. Foreign Institutional Investors (FIIs) spearheaded this bullish rotation by adding 4,208 contracts, supported by Domestic Institutional Investors (DIIs) and Proprietary traders, who bolstered positions by 1,935 and 7,550 contracts, respectively. In Stock Futures, the sentiment divergence intensified amid a high-volume turnover of 76,671 contracts. While clients and Proprietary desks aggressively offloaded 38,911 and 37,760 contracts, FIIs absorbed the bulk of the selling pressure with a massive 70,761 contract addition. This massive institutional absorption, complemented by 5,910 new DII contracts, underscores a sophisticated shift from retail skepticism to aggressive institutional accumulation across the derivatives complex.

BankNifty

For More Axis Securities Disclaimer https://simplehai.axisdirect.in/disclaimer-home

SEBI Registration number is INZ000161633