Credit Offtake Remains Firm in February 2026 by CareEdge Ratings

Synopsis

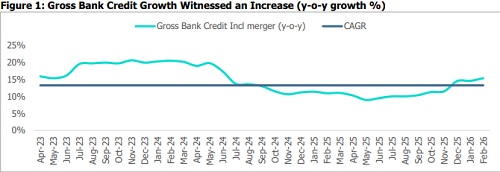

* Credit offtake improved in February 2026, with non-food bank credit growth rising to 14.3% year-on-year (yo-y), compared to 11.1% in February 2025, and remaining broadly in line with the trend observed over the preceding two months.

* The growth was broad-based, supported by strong traction in personal loans, particularly vehicle financing, alongside steady expansion in services and industrial credit, where NBFCs and MSMEs continued to act as key growth drivers. Gold loans remained a standout, registering a significant 127.9% y-o-y growth. In addition, part of the overall acceleration is attributed to changes in the fortnightly reporting framework introduced under the Banking Laws (Amendment) Act, 2025.

In February 2026, non-food bank credit grew by 14.3% y-o-y, broadly in line with the trend seen over the preceding two months. The growth was driven by personal loans, particularly vehicle financing, while MSME lending continued to grow steadily at double digits. Credit to the services sector, including trade and NBFCs, remained robust, aided by a gradual revival in corporate borrowing activity. Gold loans continued to surge by 127.9% amid elevated gold prices. On a sequential basis, credit growth maintained strong momentum across segments. However, part of this uptick reflects changes in fortnightly reporting norms introduced under the Banking Laws (Amendment) Act, 2025.

In February 2026, industrial credit growth improved to 13.5% y-o-y, up from 7.1% a year earlier. The acceleration was broad-based, supported by stronger credit offtake across multiple industries, including mining and quarrying, food processing, beverages and tobacco, textiles, leather and leather products, petroleum and coal products, engineering goods, chemicals, automotive components and transport equipment, cement, construction, infrastructure, gems and jewellery and basic metals, reflecting working capital demand. However, momentum remained uneven, as credit growth moderated in segments such as wood and wood products, paper and paper products, rubber and plastics, and glass and glassware, indicating mixed sectoral performance.

Additionally, heightened geopolitical tensions in West Asia, which escalated toward the end of February 2026, are expected to pose emerging risks for export-oriented MSMEs, particularly in sectors such as gems and jewellery, textiles, and ceramics. These segments could face pressure from potential demand disruptions and rising input costs, given their limited pricing power. In response to ongoing logistical challenges, the Reserve Bank of India has extended the enhanced export credit period of up to 450 days for pre- and post-shipment finance until June 30, 2026. While this provides near-term relief, persistent supply chain disruptions and elevated input costs may increase working capital requirements, potentially driving higher reliance on short-term borrowings in the coming months for some entities and creating funding challenges for others.

MSME credit continued to grow faster than lending to large industries, resulting in a gradual shift in the composition of industrial credit. The share of large industries moderated to 67.1% in February 2026 from 70.7% a year earlier, while micro and small enterprises increased their share from 20.2% to 23.2% over the same period. This rebalancing has been further supported by policy measures, including the Union Budget 2025–26 enhancements to MSME investment and turnover thresholds, along with the increase in guaranteed coverage limits from Rs 5 crore to Rs 10 crore. These initiatives, coupled with relatively better yields and a favourable product mix, are reinforcing the growing contribution of MSMEs to overall credit expansion.

Infrastructure credit, which constitutes around one-third of total industrial lending, registered a 7.9% y-o-y growth in February 2026. The expansion was primarily driven by the power sector, accounting for 56.2% of infrastructure credit, with growth accelerating to 21.4% from 2.6% a year ago. Ports also exhibited robust growth at 55.2%, indicating improving investment activity. However, the overall momentum remained uneven across segments. Credit growth to the road sector declined by 2.3% compared with the previous year's 3.3%, while lending to railways, airports, and telecommunications contracted, partly offsetting gains in other infrastructure segments.

In February 2026, credit to the services sector increased by 16.3% y-o-y, accelerating from 11.7% a year earlier. The rise was led by stronger lending to retail trade, tourism, hotels and restaurants, shipping, aviation, computer software and NBFCs. However, the overall expansion was partly offset by a decline in credit to segments such as transport operators and professional services.

Bank lending to NBFCs witnessed a strong traction in February 2026, with outstanding credit rising to Rs 19.4 lakh crore, accounting for 9.4% of total bank credit. Growth accelerated significantly to 20.9% y-o-y, nearly three times the 8.1% rate recorded a year ago. This strong momentum reflects NBFCs’ shift from relatively expensive market borrowings to bank funding. The uptick also reflects renewed corporate borrowing activity and the impact of a high base. In parallel, credit to the trade segment remained resilient, reaching Rs 13.2 lakh crore and registering a 14.4% y-o-y growth, marginally lower than 14.7% recorded in the previous year. Commercial real estate credit, which accounts for around 3% of total bank credit, saw steady acceleration, rising 17.4% y-o-y, up from 13.7% the previous year. Overall steady expansion indicates continued strength in commercial activity and sustained demand for working capital financing.

Personal loans, which account for nearly one-third of total bank credit, grew 15.2% y-o-y in February 2026, up from 11.7% in the corresponding period last year, reflecting continued strength in retail demand. This acceleration was primarily driven by a surge in gold loans, which grew 127.9%, surpassing the 103.5% growth seen a year ago. However, adjusting for the impact of gold-backed lending, the underlying growth in personal loans moderates to 11.5% y-o-y.

Conclusion

At the end of February 2026, overall credit growth showed broad-based improvement, reflecting strengthening demand across key segments. Although part of the uptick is attributable to changes in the reporting fortnight under the Banking Laws (Amendment) Act, 2025. Within retail, vehicle loans regained traction, supported by improved affordability post GST rate cuts, particularly in the PV segment, while corporate lending to large industries saw a marginal uptick. MSMEs continued to play a meaningful role in incremental credit growth, alongside rising bank exposure to NBFCs. Overall, banks are maintaining a balanced approach, supporting growth while preserving margins.

Additionally, the ongoing West Asia crisis is contributing to structural tightening in India’s personal loan market by sustaining inflationary pressures, delaying monetary easing, and increasing funding costs, thereby reinforcing a higher-for-longer interest rate environment. Elevated crude prices and supply disruptions have accelerated repricing in unsecured credit, particularly personal loans, faster than in secured segments, with NBFCs and fintech lenders facing greater pressure due to their reliance on wholesale funding. In tandem, rising living costs are compressing household disposable incomes, shifting borrowing toward liquidity support and debt consolidation rather than discretionary spending, while asset-quality risks are rising in subprime segments. In response, lenders are tightening underwriting standards, moderating ticket sizes, and adopting intensifying risk-based pricing, leading to selective credit flow and increasing divergence between prime and non-prime borrowers over the next 12–18 months.

Above views are of the author and not of the website kindly read disclaimer