Consumer Discretionary Sector Update : Q1FY27 Preview: Premiumisation Outpaces Margin Pressure by Choice Institutional Equities

Premiumisation Trend Strengthens; Margin on Watch

Karnataka, the largest consumer of AlcoBev products by volume in India, has altered the duty structure to move to Alcohol-in-Beverage mechanism. This has led to reduction of MRPs by 15–23% across price points, largest cuts are seen around the INR 5,000–6,000/bottle range. This will act as a significant tailwind for national players and enhance premiumisation. P&A segments are expected to grow at double digits for the industry. However, margin expansion is likely to take a pause owing to higher packaging cost (glass and PET). Price pass-throughs require state approval, which takes 1–2 quarters; therefore, we do not expect margin relief in Q1. However, ENA and grain cost are likely to offset as prices stay benign. However, if war de-escalation talks succeed, we believe the industry will be back on track and continue to enjoy the dual earnings growth from margin expansion and increase P&A volume

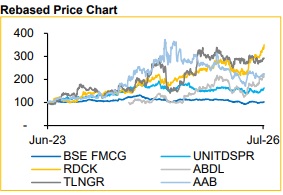

ABDL and RDCK are our High-conviction Investment Ideas RDCK: INR 3,950 (BUY) and ABDL: INR 690 (BUY) are our high-conviction ideas reflecting continued premiumisation momentum and margin expansion visibility into FY29E.

State-level Excise: Divergent Outcome

* Uttar Pradesh (Bullish): FY27E excise target set at INR 712.8 Bn (+13% YoY). E-lottery and composite shops create structural volume tailwind. RDCK is likely to be the primary beneficiary

* Maharashtra (Disruptive): Maharashtra Made Liquor (MML) policy is taxing in-state manufacturers at lower rates, thus suppressing mid-tomass volumes for national players. Maharashtra's excise collections reached INR 480 Bn in FY26 (+18% YoY). Heightened prices have led to an industry-wide contraction of 20%. UNITDSPR has a large revenue contribution from the state

* Andhra Pradesh (Normalising): IMFL prices hiked by INR 10/bottle from Jan’26; bar excise duty reversed, thus balancing retail. ABDL's AP volumes expected to normalise in Q1FY27 as retail channel stabilises

* Karnataka (Near-term Positive): Our channel checks suggest recent MRP revisions across premium spirits, reinforcing pricing power and providing a partial cushion against near-term packaging cost inflation

Input Cost Pressure Persists despite Easing Crude Price

Glass and PET cost (packaging cost), which account for ~20% of spirits revenue, increased sharply during March–May as Brent crude surged to ~USD 112/bbl. Although crude has since corrected, packaging cost typically lags commodity movements by 1–2 months, implying Q1FY27E will still absorb a significant portion of the earlier inflation. Additionally, exdistillery price hikes require state approvals and usually take 1–2 quarters to materialise, delaying pass-through. On the positive side, ENA prices remain benign providing a cushion for players with captive distillation capabilities, such as RDCK and ABDL.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131

More News

Renewable Equipments Sector Update : MNRE extends ALMM List-II exemption till Dec'26 by Prab...