Capital Goods Sector Update : Demand recovers QoQ, but lags YoY due to the base effect by Motilal Oswal Financial Services Ltd

Demand recovers QoQ, but lags YoY due to the base effect

Genset channel checks

Our channel checks with genset players indicate that demand has begun to improve after reaching lows during 3QFY25. On-the-ground activity levels have improved during 4QFY25, although they remain lower than last year. The previous year had a high volume base fueled by pre-buying activities. Competition remains intense, particularly in the low kVA segment, where market share has shifted among players due to pricing. Higher kVA ranges are still witnessing normal demand. Prices, as expected, have corrected 2-3% QoQ but are still much higher on a YoY basis. Most of the channel partners believe that this transitional phase will persist until 1QFY26, following which demand is likely to normalize. Overall revenue growth for 4QFY25 is anticipated to be driven by a 25-30% YoY increase in prices alongside a 15-20% YoY decline in volumes. Export markets have already bottomed out and will keep improving sequentially in the coming quarters. We maintain our positive stance on genset players and believe that, following this transitory phase, companies with a strong product portfolio and an extensive distribution network will stand ahead of the competition in the medium to long run. We marginally revise our estimates for KKC and maintain BUY on both KKC (TP: INR4,100) and KOEL (TP: INR1,150).

Key highlights from our interaction with genset channel partners

Genset demand is improving sequentially across ranges and user base

The following are the key highlights from our channel check with genset dealers and distributors:

* Demand improved sequentially: Demand recovered on a sequential basis, with Jan and Mar’25 being better months, while Feb’25 was hit by weaker spending across segments. Demand continued to be healthy from critical segments, including hospitals, hotels, retail, select government projects, and manufacturing units. However, real estate demand continues to be selective across regions. Volumes have improved in low kVA ranges, and participation has also increased from a broader array of players, while the mid-kVA range is experiencing growth project-wise. This, in our opinion, is expected to result in 10-15% volume growth on a QoQ basis. However, volumes are still lower on a YoY basis, as expected, since the industry benefited last year (especially in 4QFY24) due to pre-buying activities. Hence, volumes can still be lower by 15- 20% YoY for the genset industry.

* Sequential impact on volumes: Overall industry volumes reached nearly 32,000 units in 3QFY25. Industry experts anticipate that volumes can grow to 35,000- 37,000 units in 4QFY25, indicating a 10-15% QoQ improvement. However, industry volumes are still likely to dip on a YoY basis, as the impact of pre-buying in 4QFY24 led to higher volumes exceeding 40,000-42,000 units.

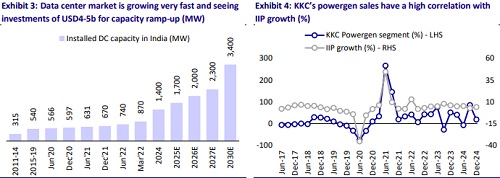

* HHP demand remains strong: Data centers remain a key growth driver for HHP genset, which continued to grow at a faster rate than low-to-mid-range gensets. KKC is a leader in the HHP segment and continues to gain from the healthy demand in this sub-segment. KOEL is making efforts to increase its share in the HHP market.

FY25 to broadly end at ~25-30% higher prices for CPCB 4+ products

Following the norm change, prices for CPCB 4+ were higher by 20-40% across various nodes. During 3QFY25, price cuts of 6-7% were taken across ranges due to weak demand in low-to-mid-kVA ranges. A few nodes up to 200kVA, can experience a further price moderation of 3-4%. Broadly, beyond that, higher prices for CPCB 4+ would be absorbed in the market, and the industry may settle at an average price increase of 25-30% for CPCB 4+ products in 4QFY25. Value-wise growth for the quarter is projected to be ~15-20%, as the impact of higher pricing will be offset by lower volumes YoY due to the high base of last year. Pricing discounts among competitors continue to remain consistent with previous trends.

Genset market segmentation among players

The genset market continued to remain dominated by three players – KOEL, Cummins, and Mahindra Powerol. They control nearly 65-70% of the market share. Within these players, there has been a shift in market share, as KOEL is strategically not participating in low-kVA ranges while Cummins is active in that range too. For the low-to-mid kVA range, we observe the presence of several domestic players, including KOEL, Cummins, Mahindra Powerol, Ashok Leyland, and Greaves Cotton. Recently, the Tata Group has also entered this segment. In the higher kVA range, multinational corporations (MNCs) remain the dominant players, with Cummins leading the market in high HHP gensets. Other active competitors in this space include Perkins, Baudouin, Caterpillar, and MTU. KOEL aims to strengthen its position in the HHP market, focusing on both product development and project execution, and is actively pursuing this goal. Within these sub-segments, the following preferences are observed: 1) for low kVA, the overall cost is the primary consideration when selecting a provider; 2) for mid-kVA, factors such as product availability, pricing, after-sales service, and distribution network are prioritized; and 3) for high kVA, emphasis is placed on quality and after-sales support.

Engineering exports have been improving

India’s engineering exports have been on the rise since Jul’24 (Exhibit 9). Companies are currently assessing strategies to boost exports in light of the potential tariff-like situations in certain countries, particularly from the US. KKC’s export revenue appears to have bottomed out in 3QFY24 and has been growing sequentially since then. KOEL is still at a nascent stage as far as export markets are concerned and is currently focusing on the Middle East and the US markets.

Key monitorables in the coming months

We believe that the high base impact of volumes due to pre-buying will continue to play until 1QFY26, and following that it will be a like-to-like comparison. In the forthcoming quarters, we will continue to monitor 1) further demand improvement from current levels, 2) the product mix of various players across kVA ranges, 3) the stability of price points, 4) the continuity of HHP demand from the data center market, and 5) the recovery in the export markets.

Valuation and recommendation

KKC is currently trading at 30.0x P/E, and KOEL is trading at 17.6x P/E on Mar’27E EPS. We value KKC at 41x P/E on two-year forward estimates and KOEL at 25x P/E on two-year forward estimates for core business. Both stocks had corrected in the recent past due to uncertainty seen in the powergen market as well as on the export front. Things are improving sequentially on demand, and we expect powergen market stability to come from FY26. We maintain BUY on both KKC (TP: INR4,100) and KOEL (TP: INR1,150) as they are ready to tide over the emission norm transition.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

More News

Infrastructure Sector Update : NHAI awarding picks up in 4Q, ends below target in FY25 by Mo...