Buy Titan Company Ltd For Target Rs.5,250 by Motilal Oswal Financial Services Ltd

Growth compounder; eyeing all-round excellence

* Titan Company (TTAN) held an analyst meet to discuss industry trends and its growth and margin outlook. Despite the current turbulent times for the jewelry industry, the company aspires a substantial scale-up of its businesses over FY26- 30. At a consolidated level, TTAN is targeting a 2.0x revenue and EBIT growth each by FY30, which translates into an implied ~20% CAGR over FY26-30. Within the domestic portfolio, the jewelry business (including Tanishq, Mia, and Zoya) is expected to achieve 2.0x revenue and 1.9x EBIT. CaratLane has a more aggressive target of 2.3x revenue and 2.5x EBIT (~25% CAGR), reflecting continued premiumization and operating leverage. The watches division is expected to deliver 2.1x revenue (~20% CAGR) and 2.2x EBIT, while EyeCare is guided to achieve 2.2x revenue and 2.5x EBIT. On the international front, the company expects the overseas Tanishq and Mia businesses to scale to 2.5x revenue and 5.5x EBIT. For Damas, management has outlined a 2.0x revenue ambition, with high single-digit margins. TTAN’s emerging businesses portfolio carries the most ambitious revenue aspiration domestically, targeting 3.4x revenue by FY30, with profitability expected to reach mid-single-digit margins.

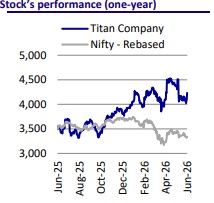

* In our recent note, we highlighted the impact of regulatory headwinds and volatile gold prices on the near-term performance (link). However, we believe TTAN is well-positioned to navigate these issues through continued diversification of gold sourcing avenues (temple jewelry, exchange, etc). The company’s superior balance sheet should also help mitigate the impact of regulatory tightening. Given TTAN’s long-term growth prospects and the historically positive stock performance following a year of regulatory announcements (outperforming the NIFTY-50 as well), we maintain a positive outlook. We model sales, EBITDA, and APAT CAGR of 16%/20%/23% over FY26-28E, and reiterate our BUY rating on the stock with a TP of INR5,250 at 60x Mar’28E EPS.

Jewelry business – Market share gains and expansion drive growth

TTAN’s jewelry business has delivered strong growth, with revenue, studded jewelry sales, and buyers posting a CAGR of 24%, 18%, and 7%, respectively, over the last three years. The company’s market share has nearly doubled to ~8.5% in FY26 from ~4.5% in FY19, and is targeted to reach ~11% by FY30. It plans to expand its jewelry network from 850 stores (ex CaratLane) to 1,400 stores by FY30. The company plans to add ~40 Tanishq stores and 60 Mia stores annually, while renovating ~60 existing Tanishq stores each year. Mia and Zoya have scaled significantly, reaching over INR20b and INR5b in revenue, respectively. Amid elevated gold prices, old-gold exchange contribution has increased to 50% of sales (+750bp in FY26) and is expected to rise further to 60– 65% over time. Management targets a 20% revenue CAGR through FY30, implying 2x revenue growth and 1.8x EBIT growth. The increasing share of gold coins is expected to exert pressure on margins in the near term; however, over the medium term, this should partly be offset through a better product mix and profitability improvements across other segments. Moreover, the permissible tenure of gold on lease has been extended from 180 days to 270 days, improving working capital flexibility.

International jewelry business – Expanding the global footprint

TTAN’s international jewelry business (Tanishq, Mia, and Zoya) crossed INR30b in revenue (UCP basis) and achieved PBT profitability in FY26. The company currently operates 10 stores in North America and 20 stores across the UAE, Oman, Qatar, Singapore, and Kuwait. To further strengthen its international presence, TTAN acquired Damas, which currently operates 123 stores across the GCC, including 60 in the UAE, 36 in Saudi Arabia, 10 in Kuwait, 9 in Qatar, and 4 each in Oman and Bahrain. Damas exited CY25 with revenue of AED740m (~INR19b). Going forward, management plans selective store additions in the UAE while positioning Saudi Arabia as the key growth market for the brand. TTAN aims to more than double the size of the Damas business by FY30 while achieving a high single-digit EBIT margin profile.

Valuation and view

* TTAN, with its superior competitive positioning (in sourcing, studded ratio, youth-centric focus, and reinvestment strategy), continues to outperform other branded players. Its brand recall and business moat are not easily replicable; therefore, Tanishq’s competitive edge will remain strong in the category.

* The jewelry store count reached 1,349 as of Mar’26, and the expansion story remains intact. The non-jewelry business is also scaling up well and will contribute to growth in the medium term.

* In our recent note, we highlighted the impact of regulatory headwinds and volatile gold prices on the near term performance (link). However, we believe TTAN is well-positioned to navigate these issues through continued diversification of gold sourcing avenues (temple jewelry, exchange, etc). The company’s superior balance sheet should also help mitigate the impact of regulatory tightening. Given TTAN’s long-term growth prospects and the historically positive stock performance following a year of regulatory announcement (outperforming the NIFTY-50 as well), we maintain a positive outlook. We model sales, EBITDA, and APAT CAGR of 16%/20%/23% over FY26- 28E and reiterate a BUY rating on the stock with a TP of INR5,250 at 60x Mar’28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412