Buy Tech Mahindra Ltd for the Target Rs. 1,750 by Motilal Oswal Financial Services Ltd

On a firm footing

FY27 margins on track

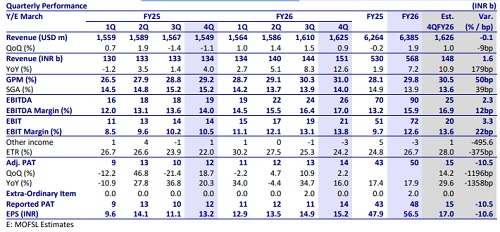

* Tech Mahindra (TECHM) reported 4QFY26 revenue of USD1.6b, up 0.6% QoQ in CC, in line with our estimate of 0.5% CC growth. BFSI/Technology rose 8.0%/2.5% QoQ, whereas Retail declined 5.3% QoQ (in USD terms). EBIT margin was up 70bp QoQ at 13.8%, beating our estimate of 13.6%.

* Adj. PAT stood at INR14b (up 2.2% QoQ/16% YoY), below our estimate of INR15b. NN deal TCV of USD1,073m was down 2.1% QoQ/up 34.5% YoY.

* In INR terms, revenue/EBIT/adj. PAT grew 7.2%/39.2%/17.9% YoY in FY26. In 1QFY27, we expect revenue/EBIT/adj. PAT to grow by 14.9%/48.6%/51.9% YoY. Free cash flow stood at 115% of net profit in FY26. FY26 RoE came in at 17.6% (vs. 15.7%/13.3%/18.5% in FY25/FY24/FY23). We reiterate BUY on TECHM with a TP of INR1,750 (implying 20% upside), based on 20x FY28E EPS.

Our view: Large deal wins provide growth visibility

* Telecom stable despite potential client-specific issues: Telecom growth has held up better than expected, up ~5.6% YoY/1.8% QoQ in 4Q and ~2.6% YoY in FY26, supported by Comviva and improving stability in the largest client. TechM’s telecom portfolio is more diversified and mature across IT, BPS, network services and products, working with 100+ operators globally, which reduces dependence on any single client or service line. We believe the Communications vertical is likely to stay resilient vs. prior quarters, supported by a large Europe deal won in 3QFY26.

* Margin story intact: EBIT margin improved to 13.8% in 4Q (+70bp QoQ) and 12.6% in FY26 (+290bp YoY). Management reiterated its FY27 margin target of ~15% and indicated that expansion is ‘not too dependent on growth’. Most of the improvement is expected from gross margin, delivery efficiencies and pricing. Fixed-price contracts carry ~8% higher margins than T&M and remain a key lever.

* With most cost actions in place, we expect TechM to move closer to ~15% margins, though we keep some buffer given the uncertain demand environment. We build in 14.8% EBIT margin for FY27.

* Risks from client budget cuts loom, but higher-than-peers FY27 growth looks achievable: Management indicated higher confidence in better YoY growth in FY27, with part of the revenue already locked in from strong deal wins (USD3.79b TCV in FY26, +42% YoY). The company closed two large deals in consecutive quarters, including a USD500mn+ telecom deal and a fiveyear global partnership with Orange Business.

* That said, some budget cuts and client-specific uncertainties persist across verticals. With industry growth seen at ~2-5%, TechM aims to outperform. We believe FY27 growth of ~4.5% YoY cc is achievable, though deal conversion and client budget stability remain key monitorables.

* Vertical mix improving gradually: BFSI showed strong traction (+8% QoQ in 4Q) with continued client additions, though ramp-ups were gradual. Manufacturing remained steady, led by aerospace and industrials, while auto is stabilizing. Retail continued to perform well, supported by logistics and e-commerce deals. Hi-tech and healthcare remained soft, though both saw some stabilization in 2H. Overall, growth drivers are becoming more broad-based, but the shift will take time.

* Management reiterated FY27 growth and margin targets: Management reiterated its FY27 targets of above-peer growth and ~15% EBIT margin. The setup is supported by healthy deal wins, stable telecom and margin visibility. While margin delivery looks largely in control, growth recovery will depend on execution in an uncertain environment, especially deal ramp-ups.

Valuation and change in estimates

* We keep our estimates unchanged, reflecting steady directional progress. We estimate FY27 EBIT margins at 14.8%, which would result in a 25% CAGR in INR PAT over FY26-28. Early signs of a turnaround in Communications vertical, supported by a large Europe deal, improve confidence in the medium-term growth outlook.

* The ongoing restructuring under the new leadership is tracking well and this quarter was another step in the right direction. We continue to like TECHM’s bottom-up turnaround story. We value TECHM at 20x FY28E EPS with a TP of INR1,750 (20% upside). We reiterate our BUY rating on the stock.

Revenue in line with our estimate and beat on margins; healthy deal TCV growth

* Revenue stood at USD1.6b, up 0.6% QoQ CC (up 0.9% QoQ in USD terms), in line with our estimate of 0.5% QoQ CC growth. For FY26, revenue stood at USD6.4b, up 0.6% YoY CC.

* IT service/BPO were up 1%/0.5% QoQ. The Americas declined 0.8%, whereas Europe grew 2.7% QoQ.

* BFSI/Technology rose 8.0%/2.5% QoQ. Retail declined 5.3% QoQ (in USD terms). ? EBIT margin was up 70bp QoQ at 13.8%, beating our estimate of 13.6%. For full year, margins stood at 12.6%, up 330bp YoY.

* Net employee reduction of 2,713 (down 1.8% QoQ). Utilization (ex. trainees) was down 50bp QoQ at 86.1%. LTM attrition was down by 20bp at 12.1%.

* New deal TCV was USD1073m, down 2.1% QoQ/up 34.5% YoY.

* Adj. PAT stood at INR14b (up 2.2% QoQ/16% YoY), below our estimate of INR15b. For full year, adj. PAT stood at INR50b, up 2% YoY.

* FCF conversion to PAT stood at 68% vs. 131% in 3QFY26. ? The board of directors approved the final dividend of INR36/share.

Key highlights from the management commentary

* Geopolitical backdrop remains challenging but management is encouraged by how client trust and engagement have deepened over the past two years.

* Closed two mega deals in consecutive quarters: 3Q – European telco deal (USD500m+ TCV over five years); 4Q – global partnership with Orange Business (five-year collaboration) focused on AI, automation, cloud, cybersecurity, and digital platforms.

* USD50m+ clients increased by four YoY to 29; USD20m+ clients expanded by seven YoY to 66 in Europe.

* FY27 is expected to show more visible contribution from seeds already planted across BFS, manufacturing, healthcare, retail/CPG, and energy and utilities.

* Management plans to unveil a new three-year FY30 vision once FY27 targets are met. Commitment is that the new plan will be ‘attractive and credible’ in equal measure.

* BFSI has longer buying and ramp-up cycles. Strategy is to deepen relationships in the Americas and APJ by winning new clients and scaling them over time.

Valuation and view

We remain positive about the restructuring at TECHM under the new leadership. But we expect the impact from these steps to be visible gradually. With the continued strength in BFSI, early signs of a turnaround in the communications and improving operational efficiency, we see room for continued margin improvement ahead. We value TECHM at 20x FY28E EPS with a TP of INR1,750 (20% upside). We reiterate our BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412